Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 73

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::printArticle() - APP/Controller/ArtileDetailController.php, line 73

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 88

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 74

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::printArticle() - APP/Controller/ArtileDetailController.php, line 74

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 88

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Warning (512): Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853 [CORE/src/Http/ResponseEmitter.php, line 48]

if (Configure::read('debug')) {

trigger_error($message, E_USER_WARNING);

} else {

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html PUBLIC "-//W3C//DTD XHTML 1.0 Transitional//EN"

"http://www.w3.org/TR/xhtml1/DTD/xhtml1-transitional.dtd">

<html xmlns="http://www.w3.org/1999/xhtml">

<head>

<link rel="canonical" href="https://im4change.in/<pre class="cake-error"><a href="javascript:void(0);" onclick="document.getElementById('cakeErr67fa95c3f2e7c-trace').style.display = (document.getElementById('cakeErr67fa95c3f2e7c-trace').style.display == 'none' ? '' : 'none');"><b>Notice</b> (8)</a>: Undefined variable: urlPrefix [<b>APP/Template/Layout/printlayout.ctp</b>, line <b>8</b>]<div id="cakeErr67fa95c3f2e7c-trace" class="cake-stack-trace" style="display: none;"><a href="javascript:void(0);" onclick="document.getElementById('cakeErr67fa95c3f2e7c-code').style.display = (document.getElementById('cakeErr67fa95c3f2e7c-code').style.display == 'none' ? '' : 'none')">Code</a> <a href="javascript:void(0);" onclick="document.getElementById('cakeErr67fa95c3f2e7c-context').style.display = (document.getElementById('cakeErr67fa95c3f2e7c-context').style.display == 'none' ? '' : 'none')">Context</a><pre id="cakeErr67fa95c3f2e7c-code" class="cake-code-dump" style="display: none;"><code><span style="color: #000000"><span style="color: #0000BB"></span><span style="color: #007700"><</span><span style="color: #0000BB">head</span><span style="color: #007700">>

</span></span></code>

<span class="code-highlight"><code><span style="color: #000000"> <link rel="canonical" href="<span style="color: #0000BB"><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">Configure</span><span style="color: #007700">::</span><span style="color: #0000BB">read</span><span style="color: #007700">(</span><span style="color: #DD0000">'SITE_URL'</span><span style="color: #007700">); </span><span style="color: #0000BB">?><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$urlPrefix</span><span style="color: #007700">;</span><span style="color: #0000BB">?><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$article_current</span><span style="color: #007700">-></span><span style="color: #0000BB">category</span><span style="color: #007700">-></span><span style="color: #0000BB">slug</span><span style="color: #007700">; </span><span style="color: #0000BB">?></span>/<span style="color: #0000BB"><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$article_current</span><span style="color: #007700">-></span><span style="color: #0000BB">seo_url</span><span style="color: #007700">; </span><span style="color: #0000BB">?></span>.html"/>

</span></code></span>

<code><span style="color: #000000"><span style="color: #0000BB"> </span><span style="color: #007700"><</span><span style="color: #0000BB">meta http</span><span style="color: #007700">-</span><span style="color: #0000BB">equiv</span><span style="color: #007700">=</span><span style="color: #DD0000">"Content-Type" </span><span style="color: #0000BB">content</span><span style="color: #007700">=</span><span style="color: #DD0000">"text/html; charset=utf-8"</span><span style="color: #007700">/>

</span></span></code></pre><pre id="cakeErr67fa95c3f2e7c-context" class="cake-context" style="display: none;">$viewFile = '/home/brlfuser/public_html/src/Template/Layout/printlayout.ctp'

$dataForView = [

'article_current' => object(App\Model\Entity\Article) {

'id' => (int) 25809,

'title' => 'Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi &amp; Surabhi Agarwal',

'subheading' => '',

'description' => '<div align="justify">

-The Business Standard

</div>

<p align="justify">

<em>Against NDA's 75 million target, UPA added 61 million in 2013-14</em>

</p>

<p align="justify">

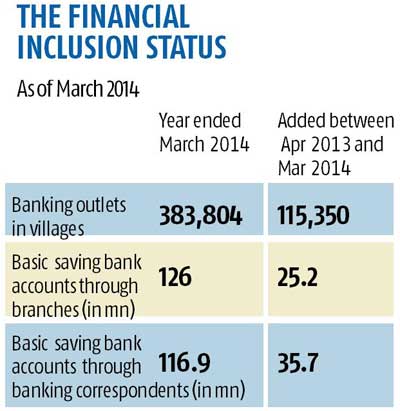

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank accounts under the scheme by Thursday and looked ahead to the target of achieving 75 million accounts by January 2015.

</p>

<p align="justify">

<img src="tinymce/uploaded/Financial Inclusion.jpg" alt="Financial Inclusion" width="400" height="411" />

</p>

<p align="justify">

In fact, given that the UPA government added an additional 60.9 million accounts in 2013-14, the target is an easy one. The real challenge is of keeping the accounts alive, funding the overdraft mechanism and ensuring confusion over the insurance cover is resolved.

</p>

<p align="justify">

A meeting on Monday in the finance ministry could resolve some of the make-or-break problems of the grand scheme. The finance ministry will try to resolve the confusion created over the account-linked accident insurance the government has already announced. Other components of the Jan Dhan scheme too are yet to be fleshed out. Each of the new bank accounts is to come with a RuPay debit card, a Rs 5,000 overdraft facility, a Rs 1 lakh accident insurance and Rs 30,000 life insurance. Keeping these accounts running, the insurance-claim system functional, funnelling money through cash transfer mechanisms and making the overdraft facilities financially viable will imply costs for different financial sector actors. Or, more likely, for these costs to be subsidised by the government.

</p>

<p align="justify">

&quot;We know the costs involved from work done earlier for the direct benefit transfer and financial inclusion schemes. But this is really several schemes rolled into one over phases and we will have to sort the fine details,&quot; said a senior official in the government.

</p>

<p align="justify">

The immediate challenge for the government will be to figure out the financial viability of maintaining the accounts and the linked insurance schemes. The RBI-promoted National Payments Corporation of India (NPCI) which offers the RuPay card, had already given the contract for accident insurance to HDFC Ergo for a period of three years. But this insurance was linked to the transaction history of the accountholder. The industry was led to believe there would be an insurance top-up by the government on this of Rs 1 lakh, costing NPCI Rs 1 per customer every year.

</p>

<p align="justify">

NPCI plans the insurance cost from the income generated out of transaction on the RuPay platform.

</p>

<p align="justify">

For every ATM transaction the issuing bank pays NPCI 40 paise. For every point of sale or ecommerce transaction NPCI gets 60 paise from the issuing bank and 30 paise from the accepting bank. All existing RuPay debit card holders would be able to avail of this facility, sources told Business Standard but not those holding saving accounts without the RuPay card. The card itself will cost about Rs 50 each roughly, though the scale could bring down costs marginally, sources said.

</p>

<p align="justify">

A former banker also noted that the financial viability of running these millions of accounts would depend on the minimum balances maintained and the number of transactions carried out in a year. A source in the government said earlier assessments suggested that out of the 180 million bank accounts opened under the financial inclusion scheme so far, a vast majority sat dormant or unused once they were opened. The RBI also noted that even as the volume of accounts had increased substantially keeping the transactions flowing remained a challenge. In other words, the banking inclusion system generated empty accounts to meet set targets.

</p>

<p align="justify">

Back-of-the envelope calculations suggest that for public sector banks an average monthly balance of Rs 50,000 is essential to meet the costs of operating an account. But another expert who has worked on the banking correspondent model economics said a much lower average balance of Rs 15,000-12,000 could help banks meet costs. But for millions of poor who could finally have an account number, this is likely to be only a dream.

</p>

<p align="justify">

The overdraft facility that the Jan Dhan scheme commits could be valuable for the poor but clarity has still not emerged on where the funds would be diverted from to finance it. Some news reports suggest that the overdraft facility will be guaranteed by an Rs 1,000 crore fund from NABARD. But this may not be sufficient if the overdraft facility really takes off. Assuming one account each for 75 million households, an overdraft facility of Rs 5,000 each amounts to Rs 37,500 crore. Even if one is to assume a risk proportion of 20-25 per cent, it would imply a minimum of Rs 7,000 crore loss to the banking sector.

</p>

<p align="justify">

A more fundamental question that the scheme has not yet resolved is the last-mile connectivity essential for financial inclusion. The government says it would be based on banking correspondents, which are not brick and mortar banks but private companies. It's cheaper than running branches but still requiring a substantial flow of money to and from the accounts to generate commission for the agents involved. The last government was unable to ensure that flow in the absence of the fertiliser, food and kerosene subsidy being turned into cash-based ones. The previous government had assessed in its internal discussions that a robust and competitive banking correspondent model required at least 200,000 working sub-agents. If one was to expect these individuals to earn even Rs 1,000 a month from acting as the last-mile connector, the previous government had assessed it would require moving the entire social sector subsidy bill through the banking correspondent funnel, including MNREGA, food, fertiliser and kerosene subsidies. This has not happened and while India already has 248,000 sub-agents most of them do not really work. Hiring an additional 50,000 sub-agents that get paid Rs 5,000 a month is bound to not be productive either.

</p>

<p align="justify">

The costs of running this banking correspondent model will be tested even more as the financial inclusion scheme reaches deeper into rural India, sources admit. &quot;If one wants these accounts to be functional and not remain dormant then the density of banking correspondent has to be increased. But that also increases the cost of delivery,&quot; explained an official who had worked on this scheme in the previous government.

</p>

<p align="justify">

Additionally, the economics of the cash transfer schemes for the banks would be dependent on what kind of float period is allowed by the government and not just the volume of funds involved.

</p>

<p align="justify">

--

</p>

<p align="justify">

<strong>PROBLEM AREAS</strong>

</p>

<p align="justify">

<strong> </strong>Accident insurance cover Meeting on Monday to resolve confusion<br />

Funding the banking correspondent model finance unclear. 248,000 correspondent agents in country<br />

Cost of overdraft facility No clarity on who shall bear the cost<br />

Existing saving accounts without RuPay card not to get other benefits<br />

Creating new accounts not a challenge, increasing transaction per account is

</p>',

'credit_writer' => 'The Business Standard, 30 August, 2014, http://wap.business-standard.com/article/economy-policy/jan-dhan-yojana-many-questions-remain-114083000024_1.html',

'article_img' => '',

'article_img_thumb' => '',

'status' => (int) 1,

'show_on_home' => (int) 1,

'lang' => 'EN',

'category_id' => (int) 16,

'tag_keyword' => '',

'seo_url' => 'jan-dhan-yojana-many-questions-remain-ishan-bakshi-nitin-sethi-surabhi-agarwal-4673846',

'meta_title' => null,

'meta_keywords' => null,

'meta_description' => null,

'noindex' => (int) 0,

'publish_date' => object(Cake\I18n\FrozenDate) {},

'most_visit_section_id' => null,

'article_big_img' => null,

'liveid' => (int) 4673846,

'created' => object(Cake\I18n\FrozenTime) {},

'modified' => object(Cake\I18n\FrozenTime) {},

'edate' => '',

'tags' => [

[maximum depth reached]

],

'category' => object(App\Model\Entity\Category) {},

'[new]' => false,

'[accessible]' => [

[maximum depth reached]

],

'[dirty]' => [[maximum depth reached]],

'[original]' => [[maximum depth reached]],

'[virtual]' => [[maximum depth reached]],

'[hasErrors]' => false,

'[errors]' => [[maximum depth reached]],

'[invalid]' => [[maximum depth reached]],

'[repository]' => 'Articles'

},

'articleid' => (int) 25809,

'metaTitle' => 'LATEST NEWS UPDATES | Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi &amp; Surabhi Agarwal',

'metaKeywords' => 'Below Poverty Line,Jan Dhan Yojana,Financial Inclusion,banking,Poverty',

'metaDesc' => '

-The Business Standard

Against NDA's 75 million target, UPA added 61 million in 2013-14

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank...',

'disp' => '<div align="justify">-The Business Standard</div><p align="justify"><em>Against NDA's 75 million target, UPA added 61 million in 2013-14</em></p><p align="justify">The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank accounts under the scheme by Thursday and looked ahead to the target of achieving 75 million accounts by January 2015.</p><p align="justify"><img src="https://im4change.in/siteadmin/tinymce/uploaded/Financial Inclusion.jpg" alt="Financial Inclusion" width="400" height="411" /></p><p align="justify">In fact, given that the UPA government added an additional 60.9 million accounts in 2013-14, the target is an easy one. The real challenge is of keeping the accounts alive, funding the overdraft mechanism and ensuring confusion over the insurance cover is resolved.</p><p align="justify">A meeting on Monday in the finance ministry could resolve some of the make-or-break problems of the grand scheme. The finance ministry will try to resolve the confusion created over the account-linked accident insurance the government has already announced. Other components of the Jan Dhan scheme too are yet to be fleshed out. Each of the new bank accounts is to come with a RuPay debit card, a Rs 5,000 overdraft facility, a Rs 1 lakh accident insurance and Rs 30,000 life insurance. Keeping these accounts running, the insurance-claim system functional, funnelling money through cash transfer mechanisms and making the overdraft facilities financially viable will imply costs for different financial sector actors. Or, more likely, for these costs to be subsidised by the government.</p><p align="justify">&quot;We know the costs involved from work done earlier for the direct benefit transfer and financial inclusion schemes. But this is really several schemes rolled into one over phases and we will have to sort the fine details,&quot; said a senior official in the government.</p><p align="justify">The immediate challenge for the government will be to figure out the financial viability of maintaining the accounts and the linked insurance schemes. The RBI-promoted National Payments Corporation of India (NPCI) which offers the RuPay card, had already given the contract for accident insurance to HDFC Ergo for a period of three years. But this insurance was linked to the transaction history of the accountholder. The industry was led to believe there would be an insurance top-up by the government on this of Rs 1 lakh, costing NPCI Rs 1 per customer every year.</p><p align="justify">NPCI plans the insurance cost from the income generated out of transaction on the RuPay platform.</p><p align="justify">For every ATM transaction the issuing bank pays NPCI 40 paise. For every point of sale or ecommerce transaction NPCI gets 60 paise from the issuing bank and 30 paise from the accepting bank. All existing RuPay debit card holders would be able to avail of this facility, sources told Business Standard but not those holding saving accounts without the RuPay card. The card itself will cost about Rs 50 each roughly, though the scale could bring down costs marginally, sources said.</p><p align="justify">A former banker also noted that the financial viability of running these millions of accounts would depend on the minimum balances maintained and the number of transactions carried out in a year. A source in the government said earlier assessments suggested that out of the 180 million bank accounts opened under the financial inclusion scheme so far, a vast majority sat dormant or unused once they were opened. The RBI also noted that even as the volume of accounts had increased substantially keeping the transactions flowing remained a challenge. In other words, the banking inclusion system generated empty accounts to meet set targets.</p><p align="justify">Back-of-the envelope calculations suggest that for public sector banks an average monthly balance of Rs 50,000 is essential to meet the costs of operating an account. But another expert who has worked on the banking correspondent model economics said a much lower average balance of Rs 15,000-12,000 could help banks meet costs. But for millions of poor who could finally have an account number, this is likely to be only a dream.</p><p align="justify">The overdraft facility that the Jan Dhan scheme commits could be valuable for the poor but clarity has still not emerged on where the funds would be diverted from to finance it. Some news reports suggest that the overdraft facility will be guaranteed by an Rs 1,000 crore fund from NABARD. But this may not be sufficient if the overdraft facility really takes off. Assuming one account each for 75 million households, an overdraft facility of Rs 5,000 each amounts to Rs 37,500 crore. Even if one is to assume a risk proportion of 20-25 per cent, it would imply a minimum of Rs 7,000 crore loss to the banking sector.</p><p align="justify">A more fundamental question that the scheme has not yet resolved is the last-mile connectivity essential for financial inclusion. The government says it would be based on banking correspondents, which are not brick and mortar banks but private companies. It's cheaper than running branches but still requiring a substantial flow of money to and from the accounts to generate commission for the agents involved. The last government was unable to ensure that flow in the absence of the fertiliser, food and kerosene subsidy being turned into cash-based ones. The previous government had assessed in its internal discussions that a robust and competitive banking correspondent model required at least 200,000 working sub-agents. If one was to expect these individuals to earn even Rs 1,000 a month from acting as the last-mile connector, the previous government had assessed it would require moving the entire social sector subsidy bill through the banking correspondent funnel, including MNREGA, food, fertiliser and kerosene subsidies. This has not happened and while India already has 248,000 sub-agents most of them do not really work. Hiring an additional 50,000 sub-agents that get paid Rs 5,000 a month is bound to not be productive either.</p><p align="justify">The costs of running this banking correspondent model will be tested even more as the financial inclusion scheme reaches deeper into rural India, sources admit. &quot;If one wants these accounts to be functional and not remain dormant then the density of banking correspondent has to be increased. But that also increases the cost of delivery,&quot; explained an official who had worked on this scheme in the previous government.</p><p align="justify">Additionally, the economics of the cash transfer schemes for the banks would be dependent on what kind of float period is allowed by the government and not just the volume of funds involved.</p><p align="justify">--</p><p align="justify"><strong>PROBLEM AREAS</strong></p><p align="justify"><strong> </strong>Accident insurance cover Meeting on Monday to resolve confusion<br /> Funding the banking correspondent model finance unclear. 248,000 correspondent agents in country<br /> Cost of overdraft facility No clarity on who shall bear the cost<br /> Existing saving accounts without RuPay card not to get other benefits<br /> Creating new accounts not a challenge, increasing transaction per account is</p>',

'lang' => 'English',

'SITE_URL' => 'https://im4change.in/',

'site_title' => 'im4change',

'adminprix' => 'admin'

]

$article_current = object(App\Model\Entity\Article) {

'id' => (int) 25809,

'title' => 'Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi &amp; Surabhi Agarwal',

'subheading' => '',

'description' => '<div align="justify">

-The Business Standard

</div>

<p align="justify">

<em>Against NDA's 75 million target, UPA added 61 million in 2013-14</em>

</p>

<p align="justify">

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank accounts under the scheme by Thursday and looked ahead to the target of achieving 75 million accounts by January 2015.

</p>

<p align="justify">

<img src="tinymce/uploaded/Financial Inclusion.jpg" alt="Financial Inclusion" width="400" height="411" />

</p>

<p align="justify">

In fact, given that the UPA government added an additional 60.9 million accounts in 2013-14, the target is an easy one. The real challenge is of keeping the accounts alive, funding the overdraft mechanism and ensuring confusion over the insurance cover is resolved.

</p>

<p align="justify">

A meeting on Monday in the finance ministry could resolve some of the make-or-break problems of the grand scheme. The finance ministry will try to resolve the confusion created over the account-linked accident insurance the government has already announced. Other components of the Jan Dhan scheme too are yet to be fleshed out. Each of the new bank accounts is to come with a RuPay debit card, a Rs 5,000 overdraft facility, a Rs 1 lakh accident insurance and Rs 30,000 life insurance. Keeping these accounts running, the insurance-claim system functional, funnelling money through cash transfer mechanisms and making the overdraft facilities financially viable will imply costs for different financial sector actors. Or, more likely, for these costs to be subsidised by the government.

</p>

<p align="justify">

&quot;We know the costs involved from work done earlier for the direct benefit transfer and financial inclusion schemes. But this is really several schemes rolled into one over phases and we will have to sort the fine details,&quot; said a senior official in the government.

</p>

<p align="justify">

The immediate challenge for the government will be to figure out the financial viability of maintaining the accounts and the linked insurance schemes. The RBI-promoted National Payments Corporation of India (NPCI) which offers the RuPay card, had already given the contract for accident insurance to HDFC Ergo for a period of three years. But this insurance was linked to the transaction history of the accountholder. The industry was led to believe there would be an insurance top-up by the government on this of Rs 1 lakh, costing NPCI Rs 1 per customer every year.

</p>

<p align="justify">

NPCI plans the insurance cost from the income generated out of transaction on the RuPay platform.

</p>

<p align="justify">

For every ATM transaction the issuing bank pays NPCI 40 paise. For every point of sale or ecommerce transaction NPCI gets 60 paise from the issuing bank and 30 paise from the accepting bank. All existing RuPay debit card holders would be able to avail of this facility, sources told Business Standard but not those holding saving accounts without the RuPay card. The card itself will cost about Rs 50 each roughly, though the scale could bring down costs marginally, sources said.

</p>

<p align="justify">

A former banker also noted that the financial viability of running these millions of accounts would depend on the minimum balances maintained and the number of transactions carried out in a year. A source in the government said earlier assessments suggested that out of the 180 million bank accounts opened under the financial inclusion scheme so far, a vast majority sat dormant or unused once they were opened. The RBI also noted that even as the volume of accounts had increased substantially keeping the transactions flowing remained a challenge. In other words, the banking inclusion system generated empty accounts to meet set targets.

</p>

<p align="justify">

Back-of-the envelope calculations suggest that for public sector banks an average monthly balance of Rs 50,000 is essential to meet the costs of operating an account. But another expert who has worked on the banking correspondent model economics said a much lower average balance of Rs 15,000-12,000 could help banks meet costs. But for millions of poor who could finally have an account number, this is likely to be only a dream.

</p>

<p align="justify">

The overdraft facility that the Jan Dhan scheme commits could be valuable for the poor but clarity has still not emerged on where the funds would be diverted from to finance it. Some news reports suggest that the overdraft facility will be guaranteed by an Rs 1,000 crore fund from NABARD. But this may not be sufficient if the overdraft facility really takes off. Assuming one account each for 75 million households, an overdraft facility of Rs 5,000 each amounts to Rs 37,500 crore. Even if one is to assume a risk proportion of 20-25 per cent, it would imply a minimum of Rs 7,000 crore loss to the banking sector.

</p>

<p align="justify">

A more fundamental question that the scheme has not yet resolved is the last-mile connectivity essential for financial inclusion. The government says it would be based on banking correspondents, which are not brick and mortar banks but private companies. It's cheaper than running branches but still requiring a substantial flow of money to and from the accounts to generate commission for the agents involved. The last government was unable to ensure that flow in the absence of the fertiliser, food and kerosene subsidy being turned into cash-based ones. The previous government had assessed in its internal discussions that a robust and competitive banking correspondent model required at least 200,000 working sub-agents. If one was to expect these individuals to earn even Rs 1,000 a month from acting as the last-mile connector, the previous government had assessed it would require moving the entire social sector subsidy bill through the banking correspondent funnel, including MNREGA, food, fertiliser and kerosene subsidies. This has not happened and while India already has 248,000 sub-agents most of them do not really work. Hiring an additional 50,000 sub-agents that get paid Rs 5,000 a month is bound to not be productive either.

</p>

<p align="justify">

The costs of running this banking correspondent model will be tested even more as the financial inclusion scheme reaches deeper into rural India, sources admit. &quot;If one wants these accounts to be functional and not remain dormant then the density of banking correspondent has to be increased. But that also increases the cost of delivery,&quot; explained an official who had worked on this scheme in the previous government.

</p>

<p align="justify">

Additionally, the economics of the cash transfer schemes for the banks would be dependent on what kind of float period is allowed by the government and not just the volume of funds involved.

</p>

<p align="justify">

--

</p>

<p align="justify">

<strong>PROBLEM AREAS</strong>

</p>

<p align="justify">

<strong> </strong>Accident insurance cover Meeting on Monday to resolve confusion<br />

Funding the banking correspondent model finance unclear. 248,000 correspondent agents in country<br />

Cost of overdraft facility No clarity on who shall bear the cost<br />

Existing saving accounts without RuPay card not to get other benefits<br />

Creating new accounts not a challenge, increasing transaction per account is

</p>',

'credit_writer' => 'The Business Standard, 30 August, 2014, http://wap.business-standard.com/article/economy-policy/jan-dhan-yojana-many-questions-remain-114083000024_1.html',

'article_img' => '',

'article_img_thumb' => '',

'status' => (int) 1,

'show_on_home' => (int) 1,

'lang' => 'EN',

'category_id' => (int) 16,

'tag_keyword' => '',

'seo_url' => 'jan-dhan-yojana-many-questions-remain-ishan-bakshi-nitin-sethi-surabhi-agarwal-4673846',

'meta_title' => null,

'meta_keywords' => null,

'meta_description' => null,

'noindex' => (int) 0,

'publish_date' => object(Cake\I18n\FrozenDate) {},

'most_visit_section_id' => null,

'article_big_img' => null,

'liveid' => (int) 4673846,

'created' => object(Cake\I18n\FrozenTime) {},

'modified' => object(Cake\I18n\FrozenTime) {},

'edate' => '',

'tags' => [

(int) 0 => object(Cake\ORM\Entity) {},

(int) 1 => object(Cake\ORM\Entity) {},

(int) 2 => object(Cake\ORM\Entity) {},

(int) 3 => object(Cake\ORM\Entity) {},

(int) 4 => object(Cake\ORM\Entity) {}

],

'category' => object(App\Model\Entity\Category) {},

'[new]' => false,

'[accessible]' => [

'*' => true,

'id' => false

],

'[dirty]' => [],

'[original]' => [],

'[virtual]' => [],

'[hasErrors]' => false,

'[errors]' => [],

'[invalid]' => [],

'[repository]' => 'Articles'

}

$articleid = (int) 25809

$metaTitle = 'LATEST NEWS UPDATES | Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi &amp; Surabhi Agarwal'

$metaKeywords = 'Below Poverty Line,Jan Dhan Yojana,Financial Inclusion,banking,Poverty'

$metaDesc = '

-The Business Standard

Against NDA's 75 million target, UPA added 61 million in 2013-14

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank...'

$disp = '<div align="justify">-The Business Standard</div><p align="justify"><em>Against NDA's 75 million target, UPA added 61 million in 2013-14</em></p><p align="justify">The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank accounts under the scheme by Thursday and looked ahead to the target of achieving 75 million accounts by January 2015.</p><p align="justify"><img src="https://im4change.in/siteadmin/tinymce/uploaded/Financial Inclusion.jpg" alt="Financial Inclusion" width="400" height="411" /></p><p align="justify">In fact, given that the UPA government added an additional 60.9 million accounts in 2013-14, the target is an easy one. The real challenge is of keeping the accounts alive, funding the overdraft mechanism and ensuring confusion over the insurance cover is resolved.</p><p align="justify">A meeting on Monday in the finance ministry could resolve some of the make-or-break problems of the grand scheme. The finance ministry will try to resolve the confusion created over the account-linked accident insurance the government has already announced. Other components of the Jan Dhan scheme too are yet to be fleshed out. Each of the new bank accounts is to come with a RuPay debit card, a Rs 5,000 overdraft facility, a Rs 1 lakh accident insurance and Rs 30,000 life insurance. Keeping these accounts running, the insurance-claim system functional, funnelling money through cash transfer mechanisms and making the overdraft facilities financially viable will imply costs for different financial sector actors. Or, more likely, for these costs to be subsidised by the government.</p><p align="justify">&quot;We know the costs involved from work done earlier for the direct benefit transfer and financial inclusion schemes. But this is really several schemes rolled into one over phases and we will have to sort the fine details,&quot; said a senior official in the government.</p><p align="justify">The immediate challenge for the government will be to figure out the financial viability of maintaining the accounts and the linked insurance schemes. The RBI-promoted National Payments Corporation of India (NPCI) which offers the RuPay card, had already given the contract for accident insurance to HDFC Ergo for a period of three years. But this insurance was linked to the transaction history of the accountholder. The industry was led to believe there would be an insurance top-up by the government on this of Rs 1 lakh, costing NPCI Rs 1 per customer every year.</p><p align="justify">NPCI plans the insurance cost from the income generated out of transaction on the RuPay platform.</p><p align="justify">For every ATM transaction the issuing bank pays NPCI 40 paise. For every point of sale or ecommerce transaction NPCI gets 60 paise from the issuing bank and 30 paise from the accepting bank. All existing RuPay debit card holders would be able to avail of this facility, sources told Business Standard but not those holding saving accounts without the RuPay card. The card itself will cost about Rs 50 each roughly, though the scale could bring down costs marginally, sources said.</p><p align="justify">A former banker also noted that the financial viability of running these millions of accounts would depend on the minimum balances maintained and the number of transactions carried out in a year. A source in the government said earlier assessments suggested that out of the 180 million bank accounts opened under the financial inclusion scheme so far, a vast majority sat dormant or unused once they were opened. The RBI also noted that even as the volume of accounts had increased substantially keeping the transactions flowing remained a challenge. In other words, the banking inclusion system generated empty accounts to meet set targets.</p><p align="justify">Back-of-the envelope calculations suggest that for public sector banks an average monthly balance of Rs 50,000 is essential to meet the costs of operating an account. But another expert who has worked on the banking correspondent model economics said a much lower average balance of Rs 15,000-12,000 could help banks meet costs. But for millions of poor who could finally have an account number, this is likely to be only a dream.</p><p align="justify">The overdraft facility that the Jan Dhan scheme commits could be valuable for the poor but clarity has still not emerged on where the funds would be diverted from to finance it. Some news reports suggest that the overdraft facility will be guaranteed by an Rs 1,000 crore fund from NABARD. But this may not be sufficient if the overdraft facility really takes off. Assuming one account each for 75 million households, an overdraft facility of Rs 5,000 each amounts to Rs 37,500 crore. Even if one is to assume a risk proportion of 20-25 per cent, it would imply a minimum of Rs 7,000 crore loss to the banking sector.</p><p align="justify">A more fundamental question that the scheme has not yet resolved is the last-mile connectivity essential for financial inclusion. The government says it would be based on banking correspondents, which are not brick and mortar banks but private companies. It's cheaper than running branches but still requiring a substantial flow of money to and from the accounts to generate commission for the agents involved. The last government was unable to ensure that flow in the absence of the fertiliser, food and kerosene subsidy being turned into cash-based ones. The previous government had assessed in its internal discussions that a robust and competitive banking correspondent model required at least 200,000 working sub-agents. If one was to expect these individuals to earn even Rs 1,000 a month from acting as the last-mile connector, the previous government had assessed it would require moving the entire social sector subsidy bill through the banking correspondent funnel, including MNREGA, food, fertiliser and kerosene subsidies. This has not happened and while India already has 248,000 sub-agents most of them do not really work. Hiring an additional 50,000 sub-agents that get paid Rs 5,000 a month is bound to not be productive either.</p><p align="justify">The costs of running this banking correspondent model will be tested even more as the financial inclusion scheme reaches deeper into rural India, sources admit. &quot;If one wants these accounts to be functional and not remain dormant then the density of banking correspondent has to be increased. But that also increases the cost of delivery,&quot; explained an official who had worked on this scheme in the previous government.</p><p align="justify">Additionally, the economics of the cash transfer schemes for the banks would be dependent on what kind of float period is allowed by the government and not just the volume of funds involved.</p><p align="justify">--</p><p align="justify"><strong>PROBLEM AREAS</strong></p><p align="justify"><strong> </strong>Accident insurance cover Meeting on Monday to resolve confusion<br /> Funding the banking correspondent model finance unclear. 248,000 correspondent agents in country<br /> Cost of overdraft facility No clarity on who shall bear the cost<br /> Existing saving accounts without RuPay card not to get other benefits<br /> Creating new accounts not a challenge, increasing transaction per account is</p>'

$lang = 'English'

$SITE_URL = 'https://im4change.in/'

$site_title = 'im4change'

$adminprix = 'admin'</pre><pre class="stack-trace">include - APP/Template/Layout/printlayout.ctp, line 8

Cake\View\View::_evaluate() - CORE/src/View/View.php, line 1413

Cake\View\View::_render() - CORE/src/View/View.php, line 1374

Cake\View\View::renderLayout() - CORE/src/View/View.php, line 927

Cake\View\View::render() - CORE/src/View/View.php, line 885

Cake\Controller\Controller::render() - CORE/src/Controller/Controller.php, line 791

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 126

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 88

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51</pre></div></pre>latest-news-updates/jan-dhan-yojana-many-questions-remain-ishan-bakshi-nitin-sethi-surabhi-agarwal-4673846.html"/>

<meta http-equiv="Content-Type" content="text/html; charset=utf-8"/>

<link href="https://im4change.in/css/control.css" rel="stylesheet" type="text/css"

media="all"/>

<title>LATEST NEWS UPDATES | Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi & Surabhi Agarwal | Im4change.org</title>

<meta name="description" content="

-The Business Standard

Against NDA's 75 million target, UPA added 61 million in 2013-14

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank..."/>

<script src="https://im4change.in/js/jquery-1.10.2.js"></script>

<script type="text/javascript" src="https://im4change.in/js/jquery-migrate.min.js"></script>

<script language="javascript" type="text/javascript">

$(document).ready(function () {

var img = $("img")[0]; // Get my img elem

var pic_real_width, pic_real_height;

$("<img/>") // Make in memory copy of image to avoid css issues

.attr("src", $(img).attr("src"))

.load(function () {

pic_real_width = this.width; // Note: $(this).width() will not

pic_real_height = this.height; // work for in memory images.

});

});

</script>

<style type="text/css">

@media screen {

div.divFooter {

display: block;

}

}

@media print {

.printbutton {

display: none !important;

}

}

</style>

</head>

<body>

<table cellpadding="0" cellspacing="0" border="0" width="98%" align="center">

<tr>

<td class="top_bg">

<div class="divFooter">

<img src="https://im4change.in/images/logo1.jpg" height="59" border="0"

alt="Resource centre on India's rural distress" style="padding-top:14px;"/>

</div>

</td>

</tr>

<tr>

<td id="topspace"> </td>

</tr>

<tr id="topspace">

<td> </td>

</tr>

<tr>

<td height="50" style="border-bottom:1px solid #000; padding-top:10px;" class="printbutton">

<form><input type="button" value=" Print this page "

onclick="window.print();return false;"/></form>

</td>

</tr>

<tr>

<td width="100%">

<h1 class="news_headlines" style="font-style:normal">

<strong>Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi & Surabhi Agarwal</strong></h1>

</td>

</tr>

<tr>

<td width="100%" style="font-family:Arial, 'Segoe Script', 'Segoe UI', sans-serif, serif"><font size="3">

<div align="justify">-The Business Standard</div><p align="justify"><em>Against NDA's 75 million target, UPA added 61 million in 2013-14</em></p><p align="justify">The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank accounts under the scheme by Thursday and looked ahead to the target of achieving 75 million accounts by January 2015.</p><p align="justify"><img src="https://im4change.in/siteadmin/tinymce/uploaded/Financial Inclusion.jpg" alt="Financial Inclusion" width="400" height="411" /></p><p align="justify">In fact, given that the UPA government added an additional 60.9 million accounts in 2013-14, the target is an easy one. The real challenge is of keeping the accounts alive, funding the overdraft mechanism and ensuring confusion over the insurance cover is resolved.</p><p align="justify">A meeting on Monday in the finance ministry could resolve some of the make-or-break problems of the grand scheme. The finance ministry will try to resolve the confusion created over the account-linked accident insurance the government has already announced. Other components of the Jan Dhan scheme too are yet to be fleshed out. Each of the new bank accounts is to come with a RuPay debit card, a Rs 5,000 overdraft facility, a Rs 1 lakh accident insurance and Rs 30,000 life insurance. Keeping these accounts running, the insurance-claim system functional, funnelling money through cash transfer mechanisms and making the overdraft facilities financially viable will imply costs for different financial sector actors. Or, more likely, for these costs to be subsidised by the government.</p><p align="justify">"We know the costs involved from work done earlier for the direct benefit transfer and financial inclusion schemes. But this is really several schemes rolled into one over phases and we will have to sort the fine details," said a senior official in the government.</p><p align="justify">The immediate challenge for the government will be to figure out the financial viability of maintaining the accounts and the linked insurance schemes. The RBI-promoted National Payments Corporation of India (NPCI) which offers the RuPay card, had already given the contract for accident insurance to HDFC Ergo for a period of three years. But this insurance was linked to the transaction history of the accountholder. The industry was led to believe there would be an insurance top-up by the government on this of Rs 1 lakh, costing NPCI Rs 1 per customer every year.</p><p align="justify">NPCI plans the insurance cost from the income generated out of transaction on the RuPay platform.</p><p align="justify">For every ATM transaction the issuing bank pays NPCI 40 paise. For every point of sale or ecommerce transaction NPCI gets 60 paise from the issuing bank and 30 paise from the accepting bank. All existing RuPay debit card holders would be able to avail of this facility, sources told Business Standard but not those holding saving accounts without the RuPay card. The card itself will cost about Rs 50 each roughly, though the scale could bring down costs marginally, sources said.</p><p align="justify">A former banker also noted that the financial viability of running these millions of accounts would depend on the minimum balances maintained and the number of transactions carried out in a year. A source in the government said earlier assessments suggested that out of the 180 million bank accounts opened under the financial inclusion scheme so far, a vast majority sat dormant or unused once they were opened. The RBI also noted that even as the volume of accounts had increased substantially keeping the transactions flowing remained a challenge. In other words, the banking inclusion system generated empty accounts to meet set targets.</p><p align="justify">Back-of-the envelope calculations suggest that for public sector banks an average monthly balance of Rs 50,000 is essential to meet the costs of operating an account. But another expert who has worked on the banking correspondent model economics said a much lower average balance of Rs 15,000-12,000 could help banks meet costs. But for millions of poor who could finally have an account number, this is likely to be only a dream.</p><p align="justify">The overdraft facility that the Jan Dhan scheme commits could be valuable for the poor but clarity has still not emerged on where the funds would be diverted from to finance it. Some news reports suggest that the overdraft facility will be guaranteed by an Rs 1,000 crore fund from NABARD. But this may not be sufficient if the overdraft facility really takes off. Assuming one account each for 75 million households, an overdraft facility of Rs 5,000 each amounts to Rs 37,500 crore. Even if one is to assume a risk proportion of 20-25 per cent, it would imply a minimum of Rs 7,000 crore loss to the banking sector.</p><p align="justify">A more fundamental question that the scheme has not yet resolved is the last-mile connectivity essential for financial inclusion. The government says it would be based on banking correspondents, which are not brick and mortar banks but private companies. It's cheaper than running branches but still requiring a substantial flow of money to and from the accounts to generate commission for the agents involved. The last government was unable to ensure that flow in the absence of the fertiliser, food and kerosene subsidy being turned into cash-based ones. The previous government had assessed in its internal discussions that a robust and competitive banking correspondent model required at least 200,000 working sub-agents. If one was to expect these individuals to earn even Rs 1,000 a month from acting as the last-mile connector, the previous government had assessed it would require moving the entire social sector subsidy bill through the banking correspondent funnel, including MNREGA, food, fertiliser and kerosene subsidies. This has not happened and while India already has 248,000 sub-agents most of them do not really work. Hiring an additional 50,000 sub-agents that get paid Rs 5,000 a month is bound to not be productive either.</p><p align="justify">The costs of running this banking correspondent model will be tested even more as the financial inclusion scheme reaches deeper into rural India, sources admit. "If one wants these accounts to be functional and not remain dormant then the density of banking correspondent has to be increased. But that also increases the cost of delivery," explained an official who had worked on this scheme in the previous government.</p><p align="justify">Additionally, the economics of the cash transfer schemes for the banks would be dependent on what kind of float period is allowed by the government and not just the volume of funds involved.</p><p align="justify">--</p><p align="justify"><strong>PROBLEM AREAS</strong></p><p align="justify"><strong> </strong>Accident insurance cover Meeting on Monday to resolve confusion<br /> Funding the banking correspondent model finance unclear. 248,000 correspondent agents in country<br /> Cost of overdraft facility No clarity on who shall bear the cost<br /> Existing saving accounts without RuPay card not to get other benefits<br /> Creating new accounts not a challenge, increasing transaction per account is</p> </font>

</td>

</tr>

<tr>

<td> </td>

</tr>

<tr>

<td height="50" style="border-top:1px solid #000; border-bottom:1px solid #000;padding-top:10px;">

<form><input type="button" value=" Print this page "

onclick="window.print();return false;"/></form>

</td>

</tr>

</table></body>

</html>'

}

$maxBufferLength = (int) 8192

$file = '/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php'

$line = (int) 853

$message = 'Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853'

Cake\Http\ResponseEmitter::emit() - CORE/src/Http/ResponseEmitter.php, line 48

Cake\Http\Server::emit() - CORE/src/Http/Server.php, line 141

[main] - ROOT/webroot/index.php, line 39

Warning (2): Cannot modify header information - headers already sent by (output started at /home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php:853) [CORE/src/Http/ResponseEmitter.php, line 148]

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html PUBLIC "-//W3C//DTD XHTML 1.0 Transitional//EN"

"http://www.w3.org/TR/xhtml1/DTD/xhtml1-transitional.dtd">

<html xmlns="http://www.w3.org/1999/xhtml">

<head>

<link rel="canonical" href="https://im4change.in/<pre class="cake-error"><a href="javascript:void(0);" onclick="document.getElementById('cakeErr67fa95c3f2e7c-trace').style.display = (document.getElementById('cakeErr67fa95c3f2e7c-trace').style.display == 'none' ? '' : 'none');"><b>Notice</b> (8)</a>: Undefined variable: urlPrefix [<b>APP/Template/Layout/printlayout.ctp</b>, line <b>8</b>]<div id="cakeErr67fa95c3f2e7c-trace" class="cake-stack-trace" style="display: none;"><a href="javascript:void(0);" onclick="document.getElementById('cakeErr67fa95c3f2e7c-code').style.display = (document.getElementById('cakeErr67fa95c3f2e7c-code').style.display == 'none' ? '' : 'none')">Code</a> <a href="javascript:void(0);" onclick="document.getElementById('cakeErr67fa95c3f2e7c-context').style.display = (document.getElementById('cakeErr67fa95c3f2e7c-context').style.display == 'none' ? '' : 'none')">Context</a><pre id="cakeErr67fa95c3f2e7c-code" class="cake-code-dump" style="display: none;"><code><span style="color: #000000"><span style="color: #0000BB"></span><span style="color: #007700"><</span><span style="color: #0000BB">head</span><span style="color: #007700">>

</span></span></code>

<span class="code-highlight"><code><span style="color: #000000"> <link rel="canonical" href="<span style="color: #0000BB"><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">Configure</span><span style="color: #007700">::</span><span style="color: #0000BB">read</span><span style="color: #007700">(</span><span style="color: #DD0000">'SITE_URL'</span><span style="color: #007700">); </span><span style="color: #0000BB">?><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$urlPrefix</span><span style="color: #007700">;</span><span style="color: #0000BB">?><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$article_current</span><span style="color: #007700">-></span><span style="color: #0000BB">category</span><span style="color: #007700">-></span><span style="color: #0000BB">slug</span><span style="color: #007700">; </span><span style="color: #0000BB">?></span>/<span style="color: #0000BB"><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$article_current</span><span style="color: #007700">-></span><span style="color: #0000BB">seo_url</span><span style="color: #007700">; </span><span style="color: #0000BB">?></span>.html"/>

</span></code></span>

<code><span style="color: #000000"><span style="color: #0000BB"> </span><span style="color: #007700"><</span><span style="color: #0000BB">meta http</span><span style="color: #007700">-</span><span style="color: #0000BB">equiv</span><span style="color: #007700">=</span><span style="color: #DD0000">"Content-Type" </span><span style="color: #0000BB">content</span><span style="color: #007700">=</span><span style="color: #DD0000">"text/html; charset=utf-8"</span><span style="color: #007700">/>

</span></span></code></pre><pre id="cakeErr67fa95c3f2e7c-context" class="cake-context" style="display: none;">$viewFile = '/home/brlfuser/public_html/src/Template/Layout/printlayout.ctp'

$dataForView = [

'article_current' => object(App\Model\Entity\Article) {

'id' => (int) 25809,

'title' => 'Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi &amp; Surabhi Agarwal',

'subheading' => '',

'description' => '<div align="justify">

-The Business Standard

</div>

<p align="justify">

<em>Against NDA's 75 million target, UPA added 61 million in 2013-14</em>

</p>

<p align="justify">

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank accounts under the scheme by Thursday and looked ahead to the target of achieving 75 million accounts by January 2015.

</p>

<p align="justify">

<img src="tinymce/uploaded/Financial Inclusion.jpg" alt="Financial Inclusion" width="400" height="411" />

</p>

<p align="justify">

In fact, given that the UPA government added an additional 60.9 million accounts in 2013-14, the target is an easy one. The real challenge is of keeping the accounts alive, funding the overdraft mechanism and ensuring confusion over the insurance cover is resolved.

</p>

<p align="justify">

A meeting on Monday in the finance ministry could resolve some of the make-or-break problems of the grand scheme. The finance ministry will try to resolve the confusion created over the account-linked accident insurance the government has already announced. Other components of the Jan Dhan scheme too are yet to be fleshed out. Each of the new bank accounts is to come with a RuPay debit card, a Rs 5,000 overdraft facility, a Rs 1 lakh accident insurance and Rs 30,000 life insurance. Keeping these accounts running, the insurance-claim system functional, funnelling money through cash transfer mechanisms and making the overdraft facilities financially viable will imply costs for different financial sector actors. Or, more likely, for these costs to be subsidised by the government.

</p>

<p align="justify">

&quot;We know the costs involved from work done earlier for the direct benefit transfer and financial inclusion schemes. But this is really several schemes rolled into one over phases and we will have to sort the fine details,&quot; said a senior official in the government.

</p>

<p align="justify">

The immediate challenge for the government will be to figure out the financial viability of maintaining the accounts and the linked insurance schemes. The RBI-promoted National Payments Corporation of India (NPCI) which offers the RuPay card, had already given the contract for accident insurance to HDFC Ergo for a period of three years. But this insurance was linked to the transaction history of the accountholder. The industry was led to believe there would be an insurance top-up by the government on this of Rs 1 lakh, costing NPCI Rs 1 per customer every year.

</p>

<p align="justify">

NPCI plans the insurance cost from the income generated out of transaction on the RuPay platform.

</p>

<p align="justify">

For every ATM transaction the issuing bank pays NPCI 40 paise. For every point of sale or ecommerce transaction NPCI gets 60 paise from the issuing bank and 30 paise from the accepting bank. All existing RuPay debit card holders would be able to avail of this facility, sources told Business Standard but not those holding saving accounts without the RuPay card. The card itself will cost about Rs 50 each roughly, though the scale could bring down costs marginally, sources said.

</p>

<p align="justify">

A former banker also noted that the financial viability of running these millions of accounts would depend on the minimum balances maintained and the number of transactions carried out in a year. A source in the government said earlier assessments suggested that out of the 180 million bank accounts opened under the financial inclusion scheme so far, a vast majority sat dormant or unused once they were opened. The RBI also noted that even as the volume of accounts had increased substantially keeping the transactions flowing remained a challenge. In other words, the banking inclusion system generated empty accounts to meet set targets.

</p>

<p align="justify">

Back-of-the envelope calculations suggest that for public sector banks an average monthly balance of Rs 50,000 is essential to meet the costs of operating an account. But another expert who has worked on the banking correspondent model economics said a much lower average balance of Rs 15,000-12,000 could help banks meet costs. But for millions of poor who could finally have an account number, this is likely to be only a dream.

</p>

<p align="justify">

The overdraft facility that the Jan Dhan scheme commits could be valuable for the poor but clarity has still not emerged on where the funds would be diverted from to finance it. Some news reports suggest that the overdraft facility will be guaranteed by an Rs 1,000 crore fund from NABARD. But this may not be sufficient if the overdraft facility really takes off. Assuming one account each for 75 million households, an overdraft facility of Rs 5,000 each amounts to Rs 37,500 crore. Even if one is to assume a risk proportion of 20-25 per cent, it would imply a minimum of Rs 7,000 crore loss to the banking sector.

</p>

<p align="justify">

A more fundamental question that the scheme has not yet resolved is the last-mile connectivity essential for financial inclusion. The government says it would be based on banking correspondents, which are not brick and mortar banks but private companies. It's cheaper than running branches but still requiring a substantial flow of money to and from the accounts to generate commission for the agents involved. The last government was unable to ensure that flow in the absence of the fertiliser, food and kerosene subsidy being turned into cash-based ones. The previous government had assessed in its internal discussions that a robust and competitive banking correspondent model required at least 200,000 working sub-agents. If one was to expect these individuals to earn even Rs 1,000 a month from acting as the last-mile connector, the previous government had assessed it would require moving the entire social sector subsidy bill through the banking correspondent funnel, including MNREGA, food, fertiliser and kerosene subsidies. This has not happened and while India already has 248,000 sub-agents most of them do not really work. Hiring an additional 50,000 sub-agents that get paid Rs 5,000 a month is bound to not be productive either.

</p>

<p align="justify">

The costs of running this banking correspondent model will be tested even more as the financial inclusion scheme reaches deeper into rural India, sources admit. &quot;If one wants these accounts to be functional and not remain dormant then the density of banking correspondent has to be increased. But that also increases the cost of delivery,&quot; explained an official who had worked on this scheme in the previous government.

</p>

<p align="justify">

Additionally, the economics of the cash transfer schemes for the banks would be dependent on what kind of float period is allowed by the government and not just the volume of funds involved.

</p>

<p align="justify">

--

</p>

<p align="justify">

<strong>PROBLEM AREAS</strong>

</p>

<p align="justify">

<strong> </strong>Accident insurance cover Meeting on Monday to resolve confusion<br />

Funding the banking correspondent model finance unclear. 248,000 correspondent agents in country<br />

Cost of overdraft facility No clarity on who shall bear the cost<br />

Existing saving accounts without RuPay card not to get other benefits<br />

Creating new accounts not a challenge, increasing transaction per account is

</p>',

'credit_writer' => 'The Business Standard, 30 August, 2014, http://wap.business-standard.com/article/economy-policy/jan-dhan-yojana-many-questions-remain-114083000024_1.html',

'article_img' => '',

'article_img_thumb' => '',

'status' => (int) 1,

'show_on_home' => (int) 1,

'lang' => 'EN',

'category_id' => (int) 16,

'tag_keyword' => '',

'seo_url' => 'jan-dhan-yojana-many-questions-remain-ishan-bakshi-nitin-sethi-surabhi-agarwal-4673846',

'meta_title' => null,

'meta_keywords' => null,

'meta_description' => null,

'noindex' => (int) 0,

'publish_date' => object(Cake\I18n\FrozenDate) {},

'most_visit_section_id' => null,

'article_big_img' => null,

'liveid' => (int) 4673846,

'created' => object(Cake\I18n\FrozenTime) {},

'modified' => object(Cake\I18n\FrozenTime) {},

'edate' => '',

'tags' => [

[maximum depth reached]

],

'category' => object(App\Model\Entity\Category) {},

'[new]' => false,

'[accessible]' => [

[maximum depth reached]

],

'[dirty]' => [[maximum depth reached]],

'[original]' => [[maximum depth reached]],

'[virtual]' => [[maximum depth reached]],

'[hasErrors]' => false,

'[errors]' => [[maximum depth reached]],

'[invalid]' => [[maximum depth reached]],

'[repository]' => 'Articles'

},

'articleid' => (int) 25809,

'metaTitle' => 'LATEST NEWS UPDATES | Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi &amp; Surabhi Agarwal',

'metaKeywords' => 'Below Poverty Line,Jan Dhan Yojana,Financial Inclusion,banking,Poverty',

'metaDesc' => '

-The Business Standard

Against NDA's 75 million target, UPA added 61 million in 2013-14

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank...',

'disp' => '<div align="justify">-The Business Standard</div><p align="justify"><em>Against NDA's 75 million target, UPA added 61 million in 2013-14</em></p><p align="justify">The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank accounts under the scheme by Thursday and looked ahead to the target of achieving 75 million accounts by January 2015.</p><p align="justify"><img src="https://im4change.in/siteadmin/tinymce/uploaded/Financial Inclusion.jpg" alt="Financial Inclusion" width="400" height="411" /></p><p align="justify">In fact, given that the UPA government added an additional 60.9 million accounts in 2013-14, the target is an easy one. The real challenge is of keeping the accounts alive, funding the overdraft mechanism and ensuring confusion over the insurance cover is resolved.</p><p align="justify">A meeting on Monday in the finance ministry could resolve some of the make-or-break problems of the grand scheme. The finance ministry will try to resolve the confusion created over the account-linked accident insurance the government has already announced. Other components of the Jan Dhan scheme too are yet to be fleshed out. Each of the new bank accounts is to come with a RuPay debit card, a Rs 5,000 overdraft facility, a Rs 1 lakh accident insurance and Rs 30,000 life insurance. Keeping these accounts running, the insurance-claim system functional, funnelling money through cash transfer mechanisms and making the overdraft facilities financially viable will imply costs for different financial sector actors. Or, more likely, for these costs to be subsidised by the government.</p><p align="justify">&quot;We know the costs involved from work done earlier for the direct benefit transfer and financial inclusion schemes. But this is really several schemes rolled into one over phases and we will have to sort the fine details,&quot; said a senior official in the government.</p><p align="justify">The immediate challenge for the government will be to figure out the financial viability of maintaining the accounts and the linked insurance schemes. The RBI-promoted National Payments Corporation of India (NPCI) which offers the RuPay card, had already given the contract for accident insurance to HDFC Ergo for a period of three years. But this insurance was linked to the transaction history of the accountholder. The industry was led to believe there would be an insurance top-up by the government on this of Rs 1 lakh, costing NPCI Rs 1 per customer every year.</p><p align="justify">NPCI plans the insurance cost from the income generated out of transaction on the RuPay platform.</p><p align="justify">For every ATM transaction the issuing bank pays NPCI 40 paise. For every point of sale or ecommerce transaction NPCI gets 60 paise from the issuing bank and 30 paise from the accepting bank. All existing RuPay debit card holders would be able to avail of this facility, sources told Business Standard but not those holding saving accounts without the RuPay card. The card itself will cost about Rs 50 each roughly, though the scale could bring down costs marginally, sources said.</p><p align="justify">A former banker also noted that the financial viability of running these millions of accounts would depend on the minimum balances maintained and the number of transactions carried out in a year. A source in the government said earlier assessments suggested that out of the 180 million bank accounts opened under the financial inclusion scheme so far, a vast majority sat dormant or unused once they were opened. The RBI also noted that even as the volume of accounts had increased substantially keeping the transactions flowing remained a challenge. In other words, the banking inclusion system generated empty accounts to meet set targets.</p><p align="justify">Back-of-the envelope calculations suggest that for public sector banks an average monthly balance of Rs 50,000 is essential to meet the costs of operating an account. But another expert who has worked on the banking correspondent model economics said a much lower average balance of Rs 15,000-12,000 could help banks meet costs. But for millions of poor who could finally have an account number, this is likely to be only a dream.</p><p align="justify">The overdraft facility that the Jan Dhan scheme commits could be valuable for the poor but clarity has still not emerged on where the funds would be diverted from to finance it. Some news reports suggest that the overdraft facility will be guaranteed by an Rs 1,000 crore fund from NABARD. But this may not be sufficient if the overdraft facility really takes off. Assuming one account each for 75 million households, an overdraft facility of Rs 5,000 each amounts to Rs 37,500 crore. Even if one is to assume a risk proportion of 20-25 per cent, it would imply a minimum of Rs 7,000 crore loss to the banking sector.</p><p align="justify">A more fundamental question that the scheme has not yet resolved is the last-mile connectivity essential for financial inclusion. The government says it would be based on banking correspondents, which are not brick and mortar banks but private companies. It's cheaper than running branches but still requiring a substantial flow of money to and from the accounts to generate commission for the agents involved. The last government was unable to ensure that flow in the absence of the fertiliser, food and kerosene subsidy being turned into cash-based ones. The previous government had assessed in its internal discussions that a robust and competitive banking correspondent model required at least 200,000 working sub-agents. If one was to expect these individuals to earn even Rs 1,000 a month from acting as the last-mile connector, the previous government had assessed it would require moving the entire social sector subsidy bill through the banking correspondent funnel, including MNREGA, food, fertiliser and kerosene subsidies. This has not happened and while India already has 248,000 sub-agents most of them do not really work. Hiring an additional 50,000 sub-agents that get paid Rs 5,000 a month is bound to not be productive either.</p><p align="justify">The costs of running this banking correspondent model will be tested even more as the financial inclusion scheme reaches deeper into rural India, sources admit. &quot;If one wants these accounts to be functional and not remain dormant then the density of banking correspondent has to be increased. But that also increases the cost of delivery,&quot; explained an official who had worked on this scheme in the previous government.</p><p align="justify">Additionally, the economics of the cash transfer schemes for the banks would be dependent on what kind of float period is allowed by the government and not just the volume of funds involved.</p><p align="justify">--</p><p align="justify"><strong>PROBLEM AREAS</strong></p><p align="justify"><strong> </strong>Accident insurance cover Meeting on Monday to resolve confusion<br /> Funding the banking correspondent model finance unclear. 248,000 correspondent agents in country<br /> Cost of overdraft facility No clarity on who shall bear the cost<br /> Existing saving accounts without RuPay card not to get other benefits<br /> Creating new accounts not a challenge, increasing transaction per account is</p>',

'lang' => 'English',

'SITE_URL' => 'https://im4change.in/',

'site_title' => 'im4change',

'adminprix' => 'admin'

]

$article_current = object(App\Model\Entity\Article) {

'id' => (int) 25809,

'title' => 'Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi &amp; Surabhi Agarwal',

'subheading' => '',

'description' => '<div align="justify">

-The Business Standard

</div>

<p align="justify">

<em>Against NDA's 75 million target, UPA added 61 million in 2013-14</em>

</p>

<p align="justify">

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank accounts under the scheme by Thursday and looked ahead to the target of achieving 75 million accounts by January 2015.

</p>

<p align="justify">

<img src="tinymce/uploaded/Financial Inclusion.jpg" alt="Financial Inclusion" width="400" height="411" />

</p>

<p align="justify">

In fact, given that the UPA government added an additional 60.9 million accounts in 2013-14, the target is an easy one. The real challenge is of keeping the accounts alive, funding the overdraft mechanism and ensuring confusion over the insurance cover is resolved.

</p>

<p align="justify">

A meeting on Monday in the finance ministry could resolve some of the make-or-break problems of the grand scheme. The finance ministry will try to resolve the confusion created over the account-linked accident insurance the government has already announced. Other components of the Jan Dhan scheme too are yet to be fleshed out. Each of the new bank accounts is to come with a RuPay debit card, a Rs 5,000 overdraft facility, a Rs 1 lakh accident insurance and Rs 30,000 life insurance. Keeping these accounts running, the insurance-claim system functional, funnelling money through cash transfer mechanisms and making the overdraft facilities financially viable will imply costs for different financial sector actors. Or, more likely, for these costs to be subsidised by the government.

</p>

<p align="justify">

&quot;We know the costs involved from work done earlier for the direct benefit transfer and financial inclusion schemes. But this is really several schemes rolled into one over phases and we will have to sort the fine details,&quot; said a senior official in the government.

</p>

<p align="justify">