Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 73

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::printArticle() - APP/Controller/ArtileDetailController.php, line 73

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 88

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 74

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::printArticle() - APP/Controller/ArtileDetailController.php, line 74

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 88

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Warning (512): Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853 [CORE/src/Http/ResponseEmitter.php, line 48]

if (Configure::read('debug')) {

trigger_error($message, E_USER_WARNING);

} else {

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html PUBLIC "-//W3C//DTD XHTML 1.0 Transitional//EN"

"http://www.w3.org/TR/xhtml1/DTD/xhtml1-transitional.dtd">

<html xmlns="http://www.w3.org/1999/xhtml">

<head>

<link rel="canonical" href="https://im4change.in/<pre class="cake-error"><a href="javascript:void(0);" onclick="document.getElementById('cakeErr67f0ea8b0be76-trace').style.display = (document.getElementById('cakeErr67f0ea8b0be76-trace').style.display == 'none' ? '' : 'none');"><b>Notice</b> (8)</a>: Undefined variable: urlPrefix [<b>APP/Template/Layout/printlayout.ctp</b>, line <b>8</b>]<div id="cakeErr67f0ea8b0be76-trace" class="cake-stack-trace" style="display: none;"><a href="javascript:void(0);" onclick="document.getElementById('cakeErr67f0ea8b0be76-code').style.display = (document.getElementById('cakeErr67f0ea8b0be76-code').style.display == 'none' ? '' : 'none')">Code</a> <a href="javascript:void(0);" onclick="document.getElementById('cakeErr67f0ea8b0be76-context').style.display = (document.getElementById('cakeErr67f0ea8b0be76-context').style.display == 'none' ? '' : 'none')">Context</a><pre id="cakeErr67f0ea8b0be76-code" class="cake-code-dump" style="display: none;"><code><span style="color: #000000"><span style="color: #0000BB"></span><span style="color: #007700"><</span><span style="color: #0000BB">head</span><span style="color: #007700">>

</span></span></code>

<span class="code-highlight"><code><span style="color: #000000"> <link rel="canonical" href="<span style="color: #0000BB"><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">Configure</span><span style="color: #007700">::</span><span style="color: #0000BB">read</span><span style="color: #007700">(</span><span style="color: #DD0000">'SITE_URL'</span><span style="color: #007700">); </span><span style="color: #0000BB">?><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$urlPrefix</span><span style="color: #007700">;</span><span style="color: #0000BB">?><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$article_current</span><span style="color: #007700">-></span><span style="color: #0000BB">category</span><span style="color: #007700">-></span><span style="color: #0000BB">slug</span><span style="color: #007700">; </span><span style="color: #0000BB">?></span>/<span style="color: #0000BB"><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$article_current</span><span style="color: #007700">-></span><span style="color: #0000BB">seo_url</span><span style="color: #007700">; </span><span style="color: #0000BB">?></span>.html"/>

</span></code></span>

<code><span style="color: #000000"><span style="color: #0000BB"> </span><span style="color: #007700"><</span><span style="color: #0000BB">meta http</span><span style="color: #007700">-</span><span style="color: #0000BB">equiv</span><span style="color: #007700">=</span><span style="color: #DD0000">"Content-Type" </span><span style="color: #0000BB">content</span><span style="color: #007700">=</span><span style="color: #DD0000">"text/html; charset=utf-8"</span><span style="color: #007700">/>

</span></span></code></pre><pre id="cakeErr67f0ea8b0be76-context" class="cake-context" style="display: none;">$viewFile = '/home/brlfuser/public_html/src/Template/Layout/printlayout.ctp'

$dataForView = [

'article_current' => object(App\Model\Entity\Article) {

'id' => (int) 33984,

'title' => 'No clear-cut trend in economy going cashless',

'subheading' => '',

'description' => '<br />

<div align="justify">

Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens&rsquo; Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being used by over 220 million users across the country. Although Paytm was launched in 2010, the popularity of its mobile wallet services and payment gateway among the ordinary citizens grew several folds only after 8 November, 2016 i.e. when the government banned currency notes of denomination Rs. 500/- and Rs. 1000/-.<br />

<br />

Following demonetisation, there has been a push on the part of the officialdom to move towards a digital economy, from the existing cash-based economy. A look at the data pertaining to electronic payments <em>(through various modes)</em>, which is provided by the Reserve Bank of India, would reveal the following facts:<br />

<br />

* The total volume of digital transactions in the economy reached a peak of 957.5 million in December, 2016, but it did not reach such a high level in the subsequent months. It means that the ordinary citizens moved towards cashless transactions out of compulsion <em>(following demonetisation of Rs. 500/- and Rs. 1000/- notes)</em>, and not out of choice. That is why the initial enthusiasm for cashless transactions petered out later on.<br />

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<iframe src="http://plot.ly/~ShambhuGhatakb01c/25.embed" width="900" height="800"></iframe>&nbsp;

<br />

</div>

<div align="justify">

<em><strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br />

<br />

<strong>Notes: <br />

<br />

</strong>The growth rates in volume and value of cashless transactions (over previous months) have been calculated by the Inclusive Media for Change team.<br />

<br />

The data provided by RBI is provisional.<br />

&nbsp;<br />

The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br />

<br />

NACH figures are for approved transactions only <br />

<br />

The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br />

<br />

The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br />

<br />

Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br />

<br />

Mobile Banking figures are taken from 5 banks.<br />

<br />

</em>* Although the growth rate in total volume of digital transactions (over previous month) touched 42.6 percent in December last year, it did not reach such a high level afterwards. It indicates that the initial excitement among the users pertaining to cashless transactions tapered off once the demonetisation period got over. Please check chart-1. <br />

<br />

* The growth in total volume of digital transactions (over previous month) turned negative in the months of January, February and April. The growth in total volume of digital transactions (over previous month) was negligible in May, 2017. Kindly see chart-1.<br />

<br />

* The total value of cashless transactions reached a peak of approximately Rs. 1.5 lakh billion in March, 2017.<br />

<br />

* The growth in total value of digital transactions (over previous month) became negative in the months of January, February and April. The growth rate in total value of digital transactions (over previous month) was 1.4 percent in May, 2017. Please see chart-1.<br />

<br />

* The RBI data on electronic payments reveal that there has been a spurt in both volume and value of total cashless transactions during March, 2017 as compared to the previous two months. &nbsp;<br />

<br />

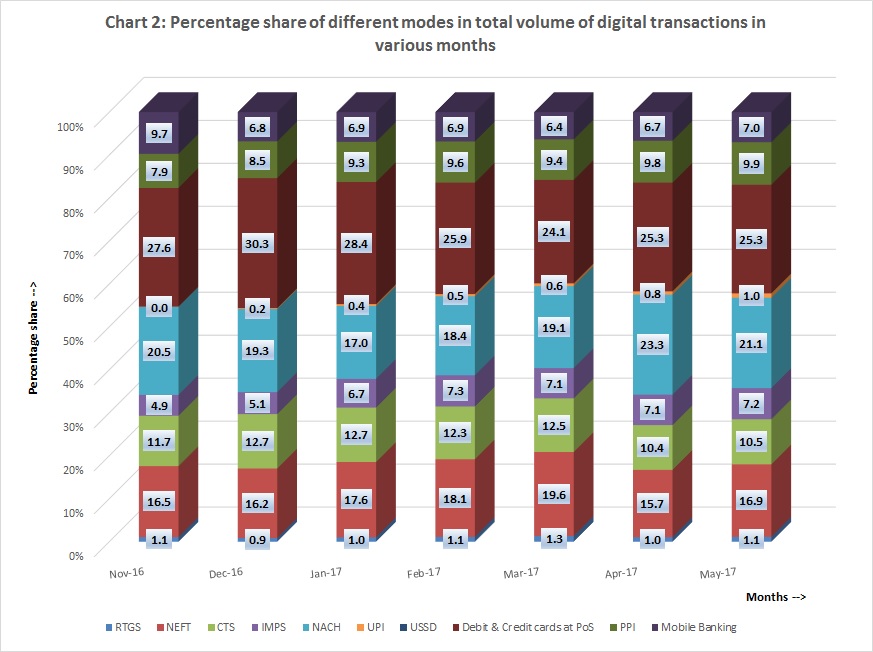

<img src="tinymce/uploaded/Chart%202%20Percentage%20share%20of%20various%20modes%20in%20total%20volume%20of%20transactions.jpg" alt="Chart 2 Percentage share of various modes in total volume of transactions" width="329" height="245" /><br />

<br />

<em>

<strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br />

<br />

<strong>Notes: <br />

</strong><br />

The percentage shares of various modes in total volume of electronic transactions (during different months) have been calculated by the Inclusive Media for Change team.<br />

<br />

The data provided by RBI is provisional.<br />

&nbsp;<br />

The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br />

<br />

NACH figures are for approved transactions only <br />

<br />

The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br />

<br />

The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br />

<br />

Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br />

<br />

Mobile Banking figures are taken from 5 banks.<br />

<br />

</em>* During the month of May, 2017, the percentage share of the mode 'debit &amp; credit cards at PoS' (i.e. 25.3 percent) in total volume of digital transactions has been the highest, followed by 'NACH' (21.1 percent), 'NEFT' (16.9 percent) and 'CTS' (10.5 percent). For the same month, the percentage share of the mode 'USSD' (i.e. zero percent) in total volume of digital transactions has been the lowest, followed by UPI (1.0 percent), 'RTGS' (1.1 percent) and 'mobile banking' (7.0 percent). Please consult chart-2.<br />

<br />

* The percentage share of the mode 'mobile banking' in total volume of cashless transactions reached a peak of 9.7 percent in November, 2016 but never reached such a high level later on. Kindly see chart-2. It indicates how the government&rsquo;s demonetisation measure aided mobile banking initially. <br />

<br />

<strong>Table-1: Percentage share of different modes in total value of digital transactions during various months</strong><br />

<br />

</div>

<div align="justify">

<img src="tinymce/uploaded/Table%201%20Percentage%20share%20of%20various%20modes%20in%20total%20value%20of%20digital%20transactions.jpg" alt="Table 1 Percentage share of various modes in total value of digital transactions" width="246" height="69" />&nbsp;

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<em><strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br />

<br />

<strong>Notes: <br />

</strong><br />

The percentage shares of different modes in total value of electronic transactions (during various months) have been calculated by the Inclusive Media for Change team.<br />

<br />

The data provided by RBI is provisional.<br />

&nbsp;<br />

The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br />

<br />

NACH figures are for approved transactions only <br />

<br />

The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br />

<br />

The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br />

<br />

Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br />

<br />

Mobile Banking figures are taken from 5 banks.<br />

<br />

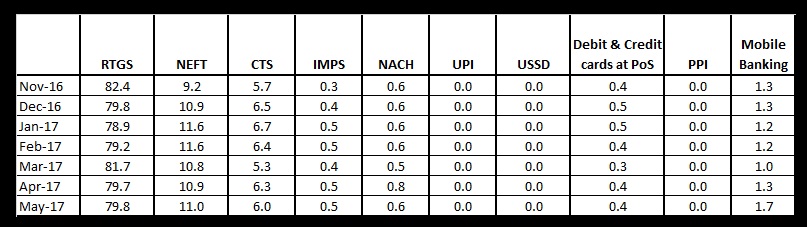

</em>* From the table-1, it could be observed that in the month of May, 2017, the percentage share of the mode 'RTGS' (i.e. 79.8 percent) in total value of digital transactions has been the highest, followed by 'NEFT' (11.0 percent), 'CTS' (6.0 percent) and 'mobile banking' (1.7 percent). For the same month, the percentage shares of the modes -- 'UPI', 'USSD' and &lsquo;PPI&rsquo; (all zero percent) in total value of digital transactions have been the lowest, followed by 'debit &amp; credit cards at PoS' (0.4 percent), 'IMPS' (0.5 percent) and 'NACH' (0.6 percent). <br />

<br />

* On comparing chart-2 against table-1, it could be said that although 'RTGS' has a meagre share in total volume of cashless transactions, which hovers around 1 percent, it occupies an overwhelmingly large share (around 80 percent) in the total value of electronic transactions <em>(from November, 2016 to May, 2017)</em>.<br />

<br />

* The percentage share of the mode 'mobile banking' in total value of cashless transactions has stayed below 2.0 percent during the last 7 months. <br />

<br />

<strong>Importance of going digital</strong><br />

<br />

Among other things, it has been argued by economists that a move towards a cashless economy would result in: a. Improvement in financial transparency and reduction in the generation of black money; b. Increase in tax base and thus tax collection; c. Financial inclusion; d. Reduction in incidence of corruption and tax evasion; and e. Reduction in the cost of printing hard currency. &nbsp;<br />

<br />

According to the official website <a href="http://cashlessindia.gov.in">http://cashlessindia.gov.in</a>, there are various modes of digital payments that are available before the citizens. They are as follows: <br />

<br />

1. Banking cards which include debit cards, credit cards, prepaid cards etc. Examples: RuPay, Visa, MasterCard etc.; <br />

2. Unstructured Supplementary Service Data (USSD);<br />

3. Aadhaar Enabled Payment System (AEPS);<br />

4. Unified Payments Interface (UPI); <br />

5. Mobile Wallets: Most banks have their e-wallets, and some of the private companies are also providing mobile wallets such as: Paytm, Freecharge, Mobikwik, Oxigen, mRuppee, Airtel Money, Jio Money, SBI Buddy, itz Cash, Citrus Pay, Vodafone M-Pesa, Axis Bank Lime, ICICI Pockets, SpeedPay etc.;<br />

6. Point-of-Sale devices (PoS devices);<br />

7. Internet Banking, which includes National Electronic Fund Transfer (NEFT), Real Time Gross Settlement (RTGS), Electronic Clearing System (ECS) &amp; Immediate Payment Service (IMPS); <br />

8. Mobile Banking;<br />

9. Micro ATMs.<br />

<br />

<br />

<strong><em>References: </em></strong><br />

<br />

Electronic Payment Systems &ndash; Data Dissemination (Updated as on June 11, 2017), Reserve Bank of India, please <a href="http://rbidocs.rbi.org.in/rdocs/content/docs/ELECT07022016_A.xls">click here</a> to access<br />

&nbsp;

<br />

Promoting Digital Payments among People, please <a href="http://cashlessindia.gov.in/promoting_digital_payments_people.html">click here</a> to access<br />

<br />

Paytm founder Vijay Shekhar Sharma to buy Rs 82 crore worth real estate in Lutyens&rsquo; Delhi, The Indian Express, 7 June, 2017, please <a href="http://indianexpress.com/article/business/paytm-founder-vijay-shekhar-sharma-to-buy-rs-82-crore-worth-real-estate-in-lutyens-delhi-4692547/">click here</a> to access <br />

&nbsp;<br />

Mobile wallets see a soaring growth post-demonetisation -Sunny Sen, Hindustan Times, 1 January, 2017, please <a href="http://www.hindustantimes.com/business-news/mobile-wallets-see-a-soaring-growth-post-demonetisation/story-zwdBi3UGqG1qZD92AEF9GK.html">click here</a> to access <br />

<br />

Here are the advantages of cashless payments and the pitfalls you should beware of -Riju Dave, The Economic Times, 12 December, 2016, please <a href="http://economictimes.indiatimes.com/wealth/spend/going-cashless-is-it-good-for-you/articleshow/55908649.cms">click here</a> to access&nbsp; <br />

<br />

Demonetisation&rsquo;s impact on mobile wallets, Livemint.com, 7 December, 2016, please <a href="http://www.livemint.com/Industry/qauzUZqgYFhwhPnt18CgIM/Demonetisation-and-the-digital-economy.html">click here</a> to access, <br />

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<strong>Image Courtesy: Inclusive Media for Change/ Shambhu Ghatak</strong> <br />

</div>',

'credit_writer' => '',

'article_img' => 'im4change_20Cashless_transaction_image.jpg',

'article_img_thumb' => 'im4change_20Cashless_transaction_image.jpg',

'status' => (int) 1,

'show_on_home' => (int) 1,

'lang' => 'EN',

'category_id' => (int) 4,

'tag_keyword' => '',

'seo_url' => 'no-clear-cut-trend-in-economy-going-cashless-4682083',

'meta_title' => null,

'meta_keywords' => null,

'meta_description' => null,

'noindex' => (int) 0,

'publish_date' => object(Cake\I18n\FrozenDate) {},

'most_visit_section_id' => null,

'article_big_img' => null,

'liveid' => (int) 4682083,

'created' => object(Cake\I18n\FrozenTime) {},

'modified' => object(Cake\I18n\FrozenTime) {},

'edate' => '',

'tags' => [

[maximum depth reached]

],

'category' => object(App\Model\Entity\Category) {},

'[new]' => false,

'[accessible]' => [

[maximum depth reached]

],

'[dirty]' => [[maximum depth reached]],

'[original]' => [[maximum depth reached]],

'[virtual]' => [[maximum depth reached]],

'[hasErrors]' => false,

'[errors]' => [[maximum depth reached]],

'[invalid]' => [[maximum depth reached]],

'[repository]' => 'Articles'

},

'articleid' => (int) 33984,

'metaTitle' => 'NEWS ALERTS | No clear-cut trend in economy going cashless',

'metaKeywords' => 'Digital Wallets,Digital India,Digital Payments,Electronic Banking Transactions,Electronic payment,Electronic payments,Cashless Economy,Mobile Banking',

'metaDesc' => '

Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens&rsquo; Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being...',

'disp' => '<br /><div align="justify">Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens&rsquo; Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being used by over 220 million users across the country. Although Paytm was launched in 2010, the popularity of its mobile wallet services and payment gateway among the ordinary citizens grew several folds only after 8 November, 2016 i.e. when the government banned currency notes of denomination Rs. 500/- and Rs. 1000/-.<br /><br />Following demonetisation, there has been a push on the part of the officialdom to move towards a digital economy, from the existing cash-based economy. A look at the data pertaining to electronic payments <em>(through various modes)</em>, which is provided by the Reserve Bank of India, would reveal the following facts:<br /><br />* The total volume of digital transactions in the economy reached a peak of 957.5 million in December, 2016, but it did not reach such a high level in the subsequent months. It means that the ordinary citizens moved towards cashless transactions out of compulsion <em>(following demonetisation of Rs. 500/- and Rs. 1000/- notes)</em>, and not out of choice. That is why the initial enthusiasm for cashless transactions petered out later on.<br /></div><div align="justify">&nbsp;</div><div align="justify"><iframe src="http://plot.ly/~ShambhuGhatakb01c/25.embed" width="900" height="800"></iframe>&nbsp;<br /></div><div align="justify"><em><strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br /><br /><strong>Notes: <br /><br /></strong>The growth rates in volume and value of cashless transactions (over previous months) have been calculated by the Inclusive Media for Change team.<br /><br />The data provided by RBI is provisional.<br />&nbsp;<br />The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br /><br />NACH figures are for approved transactions only <br /><br />The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br /><br />The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br /><br />Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br /><br />Mobile Banking figures are taken from 5 banks.<br /><br /></em>* Although the growth rate in total volume of digital transactions (over previous month) touched 42.6 percent in December last year, it did not reach such a high level afterwards. It indicates that the initial excitement among the users pertaining to cashless transactions tapered off once the demonetisation period got over. Please check chart-1. <br /><br />* The growth in total volume of digital transactions (over previous month) turned negative in the months of January, February and April. The growth in total volume of digital transactions (over previous month) was negligible in May, 2017. Kindly see chart-1.<br /><br />* The total value of cashless transactions reached a peak of approximately Rs. 1.5 lakh billion in March, 2017.<br /><br />* The growth in total value of digital transactions (over previous month) became negative in the months of January, February and April. The growth rate in total value of digital transactions (over previous month) was 1.4 percent in May, 2017. Please see chart-1.<br /><br />* The RBI data on electronic payments reveal that there has been a spurt in both volume and value of total cashless transactions during March, 2017 as compared to the previous two months. &nbsp;<br /><br /><img src="https://im4change.in/siteadmin/tinymce/uploaded/Chart%202%20Percentage%20share%20of%20various%20modes%20in%20total%20volume%20of%20transactions.jpg" alt="Chart 2 Percentage share of various modes in total volume of transactions" width="329" height="245" /><br /><br /><em><strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br /><br /><strong>Notes: <br /></strong><br />The percentage shares of various modes in total volume of electronic transactions (during different months) have been calculated by the Inclusive Media for Change team.<br /><br />The data provided by RBI is provisional.<br />&nbsp;<br />The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br /><br />NACH figures are for approved transactions only <br /><br />The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br /><br />The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br /><br />Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br /><br />Mobile Banking figures are taken from 5 banks.<br /><br /></em>* During the month of May, 2017, the percentage share of the mode 'debit &amp; credit cards at PoS' (i.e. 25.3 percent) in total volume of digital transactions has been the highest, followed by 'NACH' (21.1 percent), 'NEFT' (16.9 percent) and 'CTS' (10.5 percent). For the same month, the percentage share of the mode 'USSD' (i.e. zero percent) in total volume of digital transactions has been the lowest, followed by UPI (1.0 percent), 'RTGS' (1.1 percent) and 'mobile banking' (7.0 percent). Please consult chart-2.<br /><br />* The percentage share of the mode 'mobile banking' in total volume of cashless transactions reached a peak of 9.7 percent in November, 2016 but never reached such a high level later on. Kindly see chart-2. It indicates how the government&rsquo;s demonetisation measure aided mobile banking initially. <br /><br /><strong>Table-1: Percentage share of different modes in total value of digital transactions during various months</strong><br /><br /></div><div align="justify"><img src="https://im4change.in/siteadmin/tinymce/uploaded/Table%201%20Percentage%20share%20of%20various%20modes%20in%20total%20value%20of%20digital%20transactions.jpg" alt="Table 1 Percentage share of various modes in total value of digital transactions" width="246" height="69" />&nbsp;</div><div align="justify">&nbsp;</div><div align="justify"><em><strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br /><br /><strong>Notes: <br /></strong><br />The percentage shares of different modes in total value of electronic transactions (during various months) have been calculated by the Inclusive Media for Change team.<br /><br />The data provided by RBI is provisional.<br />&nbsp;<br />The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br /><br />NACH figures are for approved transactions only <br /><br />The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br /><br />The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br /><br />Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br /><br />Mobile Banking figures are taken from 5 banks.<br /><br /></em>* From the table-1, it could be observed that in the month of May, 2017, the percentage share of the mode 'RTGS' (i.e. 79.8 percent) in total value of digital transactions has been the highest, followed by 'NEFT' (11.0 percent), 'CTS' (6.0 percent) and 'mobile banking' (1.7 percent). For the same month, the percentage shares of the modes -- 'UPI', 'USSD' and &lsquo;PPI&rsquo; (all zero percent) in total value of digital transactions have been the lowest, followed by 'debit &amp; credit cards at PoS' (0.4 percent), 'IMPS' (0.5 percent) and 'NACH' (0.6 percent). <br /><br />* On comparing chart-2 against table-1, it could be said that although 'RTGS' has a meagre share in total volume of cashless transactions, which hovers around 1 percent, it occupies an overwhelmingly large share (around 80 percent) in the total value of electronic transactions <em>(from November, 2016 to May, 2017)</em>.<br /><br />* The percentage share of the mode 'mobile banking' in total value of cashless transactions has stayed below 2.0 percent during the last 7 months. <br /><br /><strong>Importance of going digital</strong><br /><br />Among other things, it has been argued by economists that a move towards a cashless economy would result in: a. Improvement in financial transparency and reduction in the generation of black money; b. Increase in tax base and thus tax collection; c. Financial inclusion; d. Reduction in incidence of corruption and tax evasion; and e. Reduction in the cost of printing hard currency. &nbsp;<br /><br />According to the official website <a href="http://cashlessindia.gov.in" title="http://cashlessindia.gov.in">http://cashlessindia.gov.in</a>, there are various modes of digital payments that are available before the citizens. They are as follows: <br /><br />1. Banking cards which include debit cards, credit cards, prepaid cards etc. Examples: RuPay, Visa, MasterCard etc.; <br />2. Unstructured Supplementary Service Data (USSD);<br />3. Aadhaar Enabled Payment System (AEPS);<br />4. Unified Payments Interface (UPI); <br />5. Mobile Wallets: Most banks have their e-wallets, and some of the private companies are also providing mobile wallets such as: Paytm, Freecharge, Mobikwik, Oxigen, mRuppee, Airtel Money, Jio Money, SBI Buddy, itz Cash, Citrus Pay, Vodafone M-Pesa, Axis Bank Lime, ICICI Pockets, SpeedPay etc.;<br />6. Point-of-Sale devices (PoS devices);<br />7. Internet Banking, which includes National Electronic Fund Transfer (NEFT), Real Time Gross Settlement (RTGS), Electronic Clearing System (ECS) &amp; Immediate Payment Service (IMPS); <br />8. Mobile Banking;<br />9. Micro ATMs.<br /><br /><br /><strong><em>References: </em></strong><br /><br />Electronic Payment Systems &ndash; Data Dissemination (Updated as on June 11, 2017), Reserve Bank of India, please <a href="http://rbidocs.rbi.org.in/rdocs/content/docs/ELECT07022016_A.xls" title="http://rbidocs.rbi.org.in/rdocs/content/docs/ELECT07022016_A.xls">click here</a> to access<br />&nbsp;<br />Promoting Digital Payments among People, please <a href="http://cashlessindia.gov.in/promoting_digital_payments_people.html" title="http://cashlessindia.gov.in/promoting_digital_payments_people.html">click here</a> to access<br /><br />Paytm founder Vijay Shekhar Sharma to buy Rs 82 crore worth real estate in Lutyens&rsquo; Delhi, The Indian Express, 7 June, 2017, please <a href="http://indianexpress.com/article/business/paytm-founder-vijay-shekhar-sharma-to-buy-rs-82-crore-worth-real-estate-in-lutyens-delhi-4692547/" title="http://indianexpress.com/article/business/paytm-founder-vijay-shekhar-sharma-to-buy-rs-82-crore-worth-real-estate-in-lutyens-delhi-4692547/">click here</a> to access <br />&nbsp;<br />Mobile wallets see a soaring growth post-demonetisation -Sunny Sen, Hindustan Times, 1 January, 2017, please <a href="http://www.hindustantimes.com/business-news/mobile-wallets-see-a-soaring-growth-post-demonetisation/story-zwdBi3UGqG1qZD92AEF9GK.html" title="http://www.hindustantimes.com/business-news/mobile-wallets-see-a-soaring-growth-post-demonetisation/story-zwdBi3UGqG1qZD92AEF9GK.html">click here</a> to access <br /><br />Here are the advantages of cashless payments and the pitfalls you should beware of -Riju Dave, The Economic Times, 12 December, 2016, please <a href="http://economictimes.indiatimes.com/wealth/spend/going-cashless-is-it-good-for-you/articleshow/55908649.cms" title="http://economictimes.indiatimes.com/wealth/spend/going-cashless-is-it-good-for-you/articleshow/55908649.cms">click here</a> to access&nbsp; <br /><br />Demonetisation&rsquo;s impact on mobile wallets, Livemint.com, 7 December, 2016, please <a href="http://www.livemint.com/Industry/qauzUZqgYFhwhPnt18CgIM/Demonetisation-and-the-digital-economy.html" title="http://www.livemint.com/Industry/qauzUZqgYFhwhPnt18CgIM/Demonetisation-and-the-digital-economy.html">click here</a> to access, <br /></div><div align="justify">&nbsp;</div><div align="justify">&nbsp;</div><div align="justify"><strong>Image Courtesy: Inclusive Media for Change/ Shambhu Ghatak</strong> <br /></div>',

'lang' => 'English',

'SITE_URL' => 'https://im4change.in/',

'site_title' => 'im4change',

'adminprix' => 'admin'

]

$article_current = object(App\Model\Entity\Article) {

'id' => (int) 33984,

'title' => 'No clear-cut trend in economy going cashless',

'subheading' => '',

'description' => '<br />

<div align="justify">

Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens&rsquo; Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being used by over 220 million users across the country. Although Paytm was launched in 2010, the popularity of its mobile wallet services and payment gateway among the ordinary citizens grew several folds only after 8 November, 2016 i.e. when the government banned currency notes of denomination Rs. 500/- and Rs. 1000/-.<br />

<br />

Following demonetisation, there has been a push on the part of the officialdom to move towards a digital economy, from the existing cash-based economy. A look at the data pertaining to electronic payments <em>(through various modes)</em>, which is provided by the Reserve Bank of India, would reveal the following facts:<br />

<br />

* The total volume of digital transactions in the economy reached a peak of 957.5 million in December, 2016, but it did not reach such a high level in the subsequent months. It means that the ordinary citizens moved towards cashless transactions out of compulsion <em>(following demonetisation of Rs. 500/- and Rs. 1000/- notes)</em>, and not out of choice. That is why the initial enthusiasm for cashless transactions petered out later on.<br />

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<iframe src="http://plot.ly/~ShambhuGhatakb01c/25.embed" width="900" height="800"></iframe>&nbsp;

<br />

</div>

<div align="justify">

<em><strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br />

<br />

<strong>Notes: <br />

<br />

</strong>The growth rates in volume and value of cashless transactions (over previous months) have been calculated by the Inclusive Media for Change team.<br />

<br />

The data provided by RBI is provisional.<br />

&nbsp;<br />

The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br />

<br />

NACH figures are for approved transactions only <br />

<br />

The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br />

<br />

The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br />

<br />

Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br />

<br />

Mobile Banking figures are taken from 5 banks.<br />

<br />

</em>* Although the growth rate in total volume of digital transactions (over previous month) touched 42.6 percent in December last year, it did not reach such a high level afterwards. It indicates that the initial excitement among the users pertaining to cashless transactions tapered off once the demonetisation period got over. Please check chart-1. <br />

<br />

* The growth in total volume of digital transactions (over previous month) turned negative in the months of January, February and April. The growth in total volume of digital transactions (over previous month) was negligible in May, 2017. Kindly see chart-1.<br />

<br />

* The total value of cashless transactions reached a peak of approximately Rs. 1.5 lakh billion in March, 2017.<br />

<br />

* The growth in total value of digital transactions (over previous month) became negative in the months of January, February and April. The growth rate in total value of digital transactions (over previous month) was 1.4 percent in May, 2017. Please see chart-1.<br />

<br />

* The RBI data on electronic payments reveal that there has been a spurt in both volume and value of total cashless transactions during March, 2017 as compared to the previous two months. &nbsp;<br />

<br />

<img src="tinymce/uploaded/Chart%202%20Percentage%20share%20of%20various%20modes%20in%20total%20volume%20of%20transactions.jpg" alt="Chart 2 Percentage share of various modes in total volume of transactions" width="329" height="245" /><br />

<br />

<em>

<strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br />

<br />

<strong>Notes: <br />

</strong><br />

The percentage shares of various modes in total volume of electronic transactions (during different months) have been calculated by the Inclusive Media for Change team.<br />

<br />

The data provided by RBI is provisional.<br />

&nbsp;<br />

The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br />

<br />

NACH figures are for approved transactions only <br />

<br />

The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br />

<br />

The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br />

<br />

Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br />

<br />

Mobile Banking figures are taken from 5 banks.<br />

<br />

</em>* During the month of May, 2017, the percentage share of the mode 'debit &amp; credit cards at PoS' (i.e. 25.3 percent) in total volume of digital transactions has been the highest, followed by 'NACH' (21.1 percent), 'NEFT' (16.9 percent) and 'CTS' (10.5 percent). For the same month, the percentage share of the mode 'USSD' (i.e. zero percent) in total volume of digital transactions has been the lowest, followed by UPI (1.0 percent), 'RTGS' (1.1 percent) and 'mobile banking' (7.0 percent). Please consult chart-2.<br />

<br />

* The percentage share of the mode 'mobile banking' in total volume of cashless transactions reached a peak of 9.7 percent in November, 2016 but never reached such a high level later on. Kindly see chart-2. It indicates how the government&rsquo;s demonetisation measure aided mobile banking initially. <br />

<br />

<strong>Table-1: Percentage share of different modes in total value of digital transactions during various months</strong><br />

<br />

</div>

<div align="justify">

<img src="tinymce/uploaded/Table%201%20Percentage%20share%20of%20various%20modes%20in%20total%20value%20of%20digital%20transactions.jpg" alt="Table 1 Percentage share of various modes in total value of digital transactions" width="246" height="69" />&nbsp;

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<em><strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br />

<br />

<strong>Notes: <br />

</strong><br />

The percentage shares of different modes in total value of electronic transactions (during various months) have been calculated by the Inclusive Media for Change team.<br />

<br />

The data provided by RBI is provisional.<br />

&nbsp;<br />

The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br />

<br />

NACH figures are for approved transactions only <br />

<br />

The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br />

<br />

The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br />

<br />

Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br />

<br />

Mobile Banking figures are taken from 5 banks.<br />

<br />

</em>* From the table-1, it could be observed that in the month of May, 2017, the percentage share of the mode 'RTGS' (i.e. 79.8 percent) in total value of digital transactions has been the highest, followed by 'NEFT' (11.0 percent), 'CTS' (6.0 percent) and 'mobile banking' (1.7 percent). For the same month, the percentage shares of the modes -- 'UPI', 'USSD' and &lsquo;PPI&rsquo; (all zero percent) in total value of digital transactions have been the lowest, followed by 'debit &amp; credit cards at PoS' (0.4 percent), 'IMPS' (0.5 percent) and 'NACH' (0.6 percent). <br />

<br />

* On comparing chart-2 against table-1, it could be said that although 'RTGS' has a meagre share in total volume of cashless transactions, which hovers around 1 percent, it occupies an overwhelmingly large share (around 80 percent) in the total value of electronic transactions <em>(from November, 2016 to May, 2017)</em>.<br />

<br />

* The percentage share of the mode 'mobile banking' in total value of cashless transactions has stayed below 2.0 percent during the last 7 months. <br />

<br />

<strong>Importance of going digital</strong><br />

<br />

Among other things, it has been argued by economists that a move towards a cashless economy would result in: a. Improvement in financial transparency and reduction in the generation of black money; b. Increase in tax base and thus tax collection; c. Financial inclusion; d. Reduction in incidence of corruption and tax evasion; and e. Reduction in the cost of printing hard currency. &nbsp;<br />

<br />

According to the official website <a href="http://cashlessindia.gov.in">http://cashlessindia.gov.in</a>, there are various modes of digital payments that are available before the citizens. They are as follows: <br />

<br />

1. Banking cards which include debit cards, credit cards, prepaid cards etc. Examples: RuPay, Visa, MasterCard etc.; <br />

2. Unstructured Supplementary Service Data (USSD);<br />

3. Aadhaar Enabled Payment System (AEPS);<br />

4. Unified Payments Interface (UPI); <br />

5. Mobile Wallets: Most banks have their e-wallets, and some of the private companies are also providing mobile wallets such as: Paytm, Freecharge, Mobikwik, Oxigen, mRuppee, Airtel Money, Jio Money, SBI Buddy, itz Cash, Citrus Pay, Vodafone M-Pesa, Axis Bank Lime, ICICI Pockets, SpeedPay etc.;<br />

6. Point-of-Sale devices (PoS devices);<br />

7. Internet Banking, which includes National Electronic Fund Transfer (NEFT), Real Time Gross Settlement (RTGS), Electronic Clearing System (ECS) &amp; Immediate Payment Service (IMPS); <br />

8. Mobile Banking;<br />

9. Micro ATMs.<br />

<br />

<br />

<strong><em>References: </em></strong><br />

<br />

Electronic Payment Systems &ndash; Data Dissemination (Updated as on June 11, 2017), Reserve Bank of India, please <a href="http://rbidocs.rbi.org.in/rdocs/content/docs/ELECT07022016_A.xls">click here</a> to access<br />

&nbsp;

<br />

Promoting Digital Payments among People, please <a href="http://cashlessindia.gov.in/promoting_digital_payments_people.html">click here</a> to access<br />

<br />

Paytm founder Vijay Shekhar Sharma to buy Rs 82 crore worth real estate in Lutyens&rsquo; Delhi, The Indian Express, 7 June, 2017, please <a href="http://indianexpress.com/article/business/paytm-founder-vijay-shekhar-sharma-to-buy-rs-82-crore-worth-real-estate-in-lutyens-delhi-4692547/">click here</a> to access <br />

&nbsp;<br />

Mobile wallets see a soaring growth post-demonetisation -Sunny Sen, Hindustan Times, 1 January, 2017, please <a href="http://www.hindustantimes.com/business-news/mobile-wallets-see-a-soaring-growth-post-demonetisation/story-zwdBi3UGqG1qZD92AEF9GK.html">click here</a> to access <br />

<br />

Here are the advantages of cashless payments and the pitfalls you should beware of -Riju Dave, The Economic Times, 12 December, 2016, please <a href="http://economictimes.indiatimes.com/wealth/spend/going-cashless-is-it-good-for-you/articleshow/55908649.cms">click here</a> to access&nbsp; <br />

<br />

Demonetisation&rsquo;s impact on mobile wallets, Livemint.com, 7 December, 2016, please <a href="http://www.livemint.com/Industry/qauzUZqgYFhwhPnt18CgIM/Demonetisation-and-the-digital-economy.html">click here</a> to access, <br />

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<strong>Image Courtesy: Inclusive Media for Change/ Shambhu Ghatak</strong> <br />

</div>',

'credit_writer' => '',

'article_img' => 'im4change_20Cashless_transaction_image.jpg',

'article_img_thumb' => 'im4change_20Cashless_transaction_image.jpg',

'status' => (int) 1,

'show_on_home' => (int) 1,

'lang' => 'EN',

'category_id' => (int) 4,

'tag_keyword' => '',

'seo_url' => 'no-clear-cut-trend-in-economy-going-cashless-4682083',

'meta_title' => null,

'meta_keywords' => null,

'meta_description' => null,

'noindex' => (int) 0,

'publish_date' => object(Cake\I18n\FrozenDate) {},

'most_visit_section_id' => null,

'article_big_img' => null,

'liveid' => (int) 4682083,

'created' => object(Cake\I18n\FrozenTime) {},

'modified' => object(Cake\I18n\FrozenTime) {},

'edate' => '',

'tags' => [

(int) 0 => object(Cake\ORM\Entity) {},

(int) 1 => object(Cake\ORM\Entity) {},

(int) 2 => object(Cake\ORM\Entity) {},

(int) 3 => object(Cake\ORM\Entity) {},

(int) 4 => object(Cake\ORM\Entity) {},

(int) 5 => object(Cake\ORM\Entity) {},

(int) 6 => object(Cake\ORM\Entity) {},

(int) 7 => object(Cake\ORM\Entity) {}

],

'category' => object(App\Model\Entity\Category) {},

'[new]' => false,

'[accessible]' => [

'*' => true,

'id' => false

],

'[dirty]' => [],

'[original]' => [],

'[virtual]' => [],

'[hasErrors]' => false,

'[errors]' => [],

'[invalid]' => [],

'[repository]' => 'Articles'

}

$articleid = (int) 33984

$metaTitle = 'NEWS ALERTS | No clear-cut trend in economy going cashless'

$metaKeywords = 'Digital Wallets,Digital India,Digital Payments,Electronic Banking Transactions,Electronic payment,Electronic payments,Cashless Economy,Mobile Banking'

$metaDesc = '

Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens&rsquo; Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being...'

$disp = '<br /><div align="justify">Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens&rsquo; Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being used by over 220 million users across the country. Although Paytm was launched in 2010, the popularity of its mobile wallet services and payment gateway among the ordinary citizens grew several folds only after 8 November, 2016 i.e. when the government banned currency notes of denomination Rs. 500/- and Rs. 1000/-.<br /><br />Following demonetisation, there has been a push on the part of the officialdom to move towards a digital economy, from the existing cash-based economy. A look at the data pertaining to electronic payments <em>(through various modes)</em>, which is provided by the Reserve Bank of India, would reveal the following facts:<br /><br />* The total volume of digital transactions in the economy reached a peak of 957.5 million in December, 2016, but it did not reach such a high level in the subsequent months. It means that the ordinary citizens moved towards cashless transactions out of compulsion <em>(following demonetisation of Rs. 500/- and Rs. 1000/- notes)</em>, and not out of choice. That is why the initial enthusiasm for cashless transactions petered out later on.<br /></div><div align="justify">&nbsp;</div><div align="justify"><iframe src="http://plot.ly/~ShambhuGhatakb01c/25.embed" width="900" height="800"></iframe>&nbsp;<br /></div><div align="justify"><em><strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br /><br /><strong>Notes: <br /><br /></strong>The growth rates in volume and value of cashless transactions (over previous months) have been calculated by the Inclusive Media for Change team.<br /><br />The data provided by RBI is provisional.<br />&nbsp;<br />The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br /><br />NACH figures are for approved transactions only <br /><br />The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br /><br />The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br /><br />Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br /><br />Mobile Banking figures are taken from 5 banks.<br /><br /></em>* Although the growth rate in total volume of digital transactions (over previous month) touched 42.6 percent in December last year, it did not reach such a high level afterwards. It indicates that the initial excitement among the users pertaining to cashless transactions tapered off once the demonetisation period got over. Please check chart-1. <br /><br />* The growth in total volume of digital transactions (over previous month) turned negative in the months of January, February and April. The growth in total volume of digital transactions (over previous month) was negligible in May, 2017. Kindly see chart-1.<br /><br />* The total value of cashless transactions reached a peak of approximately Rs. 1.5 lakh billion in March, 2017.<br /><br />* The growth in total value of digital transactions (over previous month) became negative in the months of January, February and April. The growth rate in total value of digital transactions (over previous month) was 1.4 percent in May, 2017. Please see chart-1.<br /><br />* The RBI data on electronic payments reveal that there has been a spurt in both volume and value of total cashless transactions during March, 2017 as compared to the previous two months. &nbsp;<br /><br /><img src="https://im4change.in/siteadmin/tinymce/uploaded/Chart%202%20Percentage%20share%20of%20various%20modes%20in%20total%20volume%20of%20transactions.jpg" alt="Chart 2 Percentage share of various modes in total volume of transactions" width="329" height="245" /><br /><br /><em><strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br /><br /><strong>Notes: <br /></strong><br />The percentage shares of various modes in total volume of electronic transactions (during different months) have been calculated by the Inclusive Media for Change team.<br /><br />The data provided by RBI is provisional.<br />&nbsp;<br />The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br /><br />NACH figures are for approved transactions only <br /><br />The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br /><br />The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br /><br />Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br /><br />Mobile Banking figures are taken from 5 banks.<br /><br /></em>* During the month of May, 2017, the percentage share of the mode 'debit &amp; credit cards at PoS' (i.e. 25.3 percent) in total volume of digital transactions has been the highest, followed by 'NACH' (21.1 percent), 'NEFT' (16.9 percent) and 'CTS' (10.5 percent). For the same month, the percentage share of the mode 'USSD' (i.e. zero percent) in total volume of digital transactions has been the lowest, followed by UPI (1.0 percent), 'RTGS' (1.1 percent) and 'mobile banking' (7.0 percent). Please consult chart-2.<br /><br />* The percentage share of the mode 'mobile banking' in total volume of cashless transactions reached a peak of 9.7 percent in November, 2016 but never reached such a high level later on. Kindly see chart-2. It indicates how the government&rsquo;s demonetisation measure aided mobile banking initially. <br /><br /><strong>Table-1: Percentage share of different modes in total value of digital transactions during various months</strong><br /><br /></div><div align="justify"><img src="https://im4change.in/siteadmin/tinymce/uploaded/Table%201%20Percentage%20share%20of%20various%20modes%20in%20total%20value%20of%20digital%20transactions.jpg" alt="Table 1 Percentage share of various modes in total value of digital transactions" width="246" height="69" />&nbsp;</div><div align="justify">&nbsp;</div><div align="justify"><em><strong>Source: </strong>Electronic Payment Systems &ndash; Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br /><br /><strong>Notes: <br /></strong><br />The percentage shares of different modes in total value of electronic transactions (during various months) have been calculated by the Inclusive Media for Change team.<br /><br />The data provided by RBI is provisional.<br />&nbsp;<br />The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br /><br />NACH figures are for approved transactions only <br /><br />The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br /><br />The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br /><br />Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br /><br />Mobile Banking figures are taken from 5 banks.<br /><br /></em>* From the table-1, it could be observed that in the month of May, 2017, the percentage share of the mode 'RTGS' (i.e. 79.8 percent) in total value of digital transactions has been the highest, followed by 'NEFT' (11.0 percent), 'CTS' (6.0 percent) and 'mobile banking' (1.7 percent). For the same month, the percentage shares of the modes -- 'UPI', 'USSD' and &lsquo;PPI&rsquo; (all zero percent) in total value of digital transactions have been the lowest, followed by 'debit &amp; credit cards at PoS' (0.4 percent), 'IMPS' (0.5 percent) and 'NACH' (0.6 percent). <br /><br />* On comparing chart-2 against table-1, it could be said that although 'RTGS' has a meagre share in total volume of cashless transactions, which hovers around 1 percent, it occupies an overwhelmingly large share (around 80 percent) in the total value of electronic transactions <em>(from November, 2016 to May, 2017)</em>.<br /><br />* The percentage share of the mode 'mobile banking' in total value of cashless transactions has stayed below 2.0 percent during the last 7 months. <br /><br /><strong>Importance of going digital</strong><br /><br />Among other things, it has been argued by economists that a move towards a cashless economy would result in: a. Improvement in financial transparency and reduction in the generation of black money; b. Increase in tax base and thus tax collection; c. Financial inclusion; d. Reduction in incidence of corruption and tax evasion; and e. Reduction in the cost of printing hard currency. &nbsp;<br /><br />According to the official website <a href="http://cashlessindia.gov.in" title="http://cashlessindia.gov.in">http://cashlessindia.gov.in</a>, there are various modes of digital payments that are available before the citizens. They are as follows: <br /><br />1. Banking cards which include debit cards, credit cards, prepaid cards etc. Examples: RuPay, Visa, MasterCard etc.; <br />2. Unstructured Supplementary Service Data (USSD);<br />3. Aadhaar Enabled Payment System (AEPS);<br />4. Unified Payments Interface (UPI); <br />5. Mobile Wallets: Most banks have their e-wallets, and some of the private companies are also providing mobile wallets such as: Paytm, Freecharge, Mobikwik, Oxigen, mRuppee, Airtel Money, Jio Money, SBI Buddy, itz Cash, Citrus Pay, Vodafone M-Pesa, Axis Bank Lime, ICICI Pockets, SpeedPay etc.;<br />6. Point-of-Sale devices (PoS devices);<br />7. Internet Banking, which includes National Electronic Fund Transfer (NEFT), Real Time Gross Settlement (RTGS), Electronic Clearing System (ECS) &amp; Immediate Payment Service (IMPS); <br />8. Mobile Banking;<br />9. Micro ATMs.<br /><br /><br /><strong><em>References: </em></strong><br /><br />Electronic Payment Systems &ndash; Data Dissemination (Updated as on June 11, 2017), Reserve Bank of India, please <a href="http://rbidocs.rbi.org.in/rdocs/content/docs/ELECT07022016_A.xls" title="http://rbidocs.rbi.org.in/rdocs/content/docs/ELECT07022016_A.xls">click here</a> to access<br />&nbsp;<br />Promoting Digital Payments among People, please <a href="http://cashlessindia.gov.in/promoting_digital_payments_people.html" title="http://cashlessindia.gov.in/promoting_digital_payments_people.html">click here</a> to access<br /><br />Paytm founder Vijay Shekhar Sharma to buy Rs 82 crore worth real estate in Lutyens&rsquo; Delhi, The Indian Express, 7 June, 2017, please <a href="http://indianexpress.com/article/business/paytm-founder-vijay-shekhar-sharma-to-buy-rs-82-crore-worth-real-estate-in-lutyens-delhi-4692547/" title="http://indianexpress.com/article/business/paytm-founder-vijay-shekhar-sharma-to-buy-rs-82-crore-worth-real-estate-in-lutyens-delhi-4692547/">click here</a> to access <br />&nbsp;<br />Mobile wallets see a soaring growth post-demonetisation -Sunny Sen, Hindustan Times, 1 January, 2017, please <a href="http://www.hindustantimes.com/business-news/mobile-wallets-see-a-soaring-growth-post-demonetisation/story-zwdBi3UGqG1qZD92AEF9GK.html" title="http://www.hindustantimes.com/business-news/mobile-wallets-see-a-soaring-growth-post-demonetisation/story-zwdBi3UGqG1qZD92AEF9GK.html">click here</a> to access <br /><br />Here are the advantages of cashless payments and the pitfalls you should beware of -Riju Dave, The Economic Times, 12 December, 2016, please <a href="http://economictimes.indiatimes.com/wealth/spend/going-cashless-is-it-good-for-you/articleshow/55908649.cms" title="http://economictimes.indiatimes.com/wealth/spend/going-cashless-is-it-good-for-you/articleshow/55908649.cms">click here</a> to access&nbsp; <br /><br />Demonetisation&rsquo;s impact on mobile wallets, Livemint.com, 7 December, 2016, please <a href="http://www.livemint.com/Industry/qauzUZqgYFhwhPnt18CgIM/Demonetisation-and-the-digital-economy.html" title="http://www.livemint.com/Industry/qauzUZqgYFhwhPnt18CgIM/Demonetisation-and-the-digital-economy.html">click here</a> to access, <br /></div><div align="justify">&nbsp;</div><div align="justify">&nbsp;</div><div align="justify"><strong>Image Courtesy: Inclusive Media for Change/ Shambhu Ghatak</strong> <br /></div>'

$lang = 'English'

$SITE_URL = 'https://im4change.in/'

$site_title = 'im4change'

$adminprix = 'admin'</pre><pre class="stack-trace">include - APP/Template/Layout/printlayout.ctp, line 8

Cake\View\View::_evaluate() - CORE/src/View/View.php, line 1413

Cake\View\View::_render() - CORE/src/View/View.php, line 1374

Cake\View\View::renderLayout() - CORE/src/View/View.php, line 927

Cake\View\View::render() - CORE/src/View/View.php, line 885

Cake\Controller\Controller::render() - CORE/src/Controller/Controller.php, line 791

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 126

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 88

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51</pre></div></pre>news-alerts-57/no-clear-cut-trend-in-economy-going-cashless-4682083.html"/>

<meta http-equiv="Content-Type" content="text/html; charset=utf-8"/>

<link href="https://im4change.in/css/control.css" rel="stylesheet" type="text/css"

media="all"/>

<title>NEWS ALERTS | No clear-cut trend in economy going cashless | Im4change.org</title>

<meta name="description" content="

Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens’ Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being..."/>

<script src="https://im4change.in/js/jquery-1.10.2.js"></script>

<script type="text/javascript" src="https://im4change.in/js/jquery-migrate.min.js"></script>

<script language="javascript" type="text/javascript">

$(document).ready(function () {

var img = $("img")[0]; // Get my img elem

var pic_real_width, pic_real_height;

$("<img/>") // Make in memory copy of image to avoid css issues

.attr("src", $(img).attr("src"))

.load(function () {

pic_real_width = this.width; // Note: $(this).width() will not

pic_real_height = this.height; // work for in memory images.

});

});

</script>

<style type="text/css">

@media screen {

div.divFooter {

display: block;

}

}

@media print {

.printbutton {

display: none !important;

}

}

</style>

</head>

<body>

<table cellpadding="0" cellspacing="0" border="0" width="98%" align="center">

<tr>

<td class="top_bg">

<div class="divFooter">

<img src="https://im4change.in/images/logo1.jpg" height="59" border="0"

alt="Resource centre on India's rural distress" style="padding-top:14px;"/>

</div>

</td>

</tr>

<tr>

<td id="topspace"> </td>

</tr>

<tr id="topspace">

<td> </td>

</tr>

<tr>

<td height="50" style="border-bottom:1px solid #000; padding-top:10px;" class="printbutton">

<form><input type="button" value=" Print this page "

onclick="window.print();return false;"/></form>

</td>

</tr>

<tr>

<td width="100%">

<h1 class="news_headlines" style="font-style:normal">

<strong>No clear-cut trend in economy going cashless</strong></h1>

</td>

</tr>

<tr>

<td width="100%" style="font-family:Arial, 'Segoe Script', 'Segoe UI', sans-serif, serif"><font size="3">