Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 73

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::printArticle() - APP/Controller/ArtileDetailController.php, line 73

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 88

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 74

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::printArticle() - APP/Controller/ArtileDetailController.php, line 74

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 88

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Warning (512): Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853 [CORE/src/Http/ResponseEmitter.php, line 48]

if (Configure::read('debug')) {

trigger_error($message, E_USER_WARNING);

} else {

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html PUBLIC "-//W3C//DTD XHTML 1.0 Transitional//EN"

"http://www.w3.org/TR/xhtml1/DTD/xhtml1-transitional.dtd">

<html xmlns="http://www.w3.org/1999/xhtml">

<head>

<link rel="canonical" href="https://im4change.in/<pre class="cake-error"><a href="javascript:void(0);" onclick="document.getElementById('cakeErr6824c959792fc-trace').style.display = (document.getElementById('cakeErr6824c959792fc-trace').style.display == 'none' ? '' : 'none');"><b>Notice</b> (8)</a>: Undefined variable: urlPrefix [<b>APP/Template/Layout/printlayout.ctp</b>, line <b>8</b>]<div id="cakeErr6824c959792fc-trace" class="cake-stack-trace" style="display: none;"><a href="javascript:void(0);" onclick="document.getElementById('cakeErr6824c959792fc-code').style.display = (document.getElementById('cakeErr6824c959792fc-code').style.display == 'none' ? '' : 'none')">Code</a> <a href="javascript:void(0);" onclick="document.getElementById('cakeErr6824c959792fc-context').style.display = (document.getElementById('cakeErr6824c959792fc-context').style.display == 'none' ? '' : 'none')">Context</a><pre id="cakeErr6824c959792fc-code" class="cake-code-dump" style="display: none;"><code><span style="color: #000000"><span style="color: #0000BB"></span><span style="color: #007700"><</span><span style="color: #0000BB">head</span><span style="color: #007700">>

</span></span></code>

<span class="code-highlight"><code><span style="color: #000000"> <link rel="canonical" href="<span style="color: #0000BB"><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">Configure</span><span style="color: #007700">::</span><span style="color: #0000BB">read</span><span style="color: #007700">(</span><span style="color: #DD0000">'SITE_URL'</span><span style="color: #007700">); </span><span style="color: #0000BB">?><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$urlPrefix</span><span style="color: #007700">;</span><span style="color: #0000BB">?><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$article_current</span><span style="color: #007700">-></span><span style="color: #0000BB">category</span><span style="color: #007700">-></span><span style="color: #0000BB">slug</span><span style="color: #007700">; </span><span style="color: #0000BB">?></span>/<span style="color: #0000BB"><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$article_current</span><span style="color: #007700">-></span><span style="color: #0000BB">seo_url</span><span style="color: #007700">; </span><span style="color: #0000BB">?></span>.html"/>

</span></code></span>

<code><span style="color: #000000"><span style="color: #0000BB"> </span><span style="color: #007700"><</span><span style="color: #0000BB">meta http</span><span style="color: #007700">-</span><span style="color: #0000BB">equiv</span><span style="color: #007700">=</span><span style="color: #DD0000">"Content-Type" </span><span style="color: #0000BB">content</span><span style="color: #007700">=</span><span style="color: #DD0000">"text/html; charset=utf-8"</span><span style="color: #007700">/>

</span></span></code></pre><pre id="cakeErr6824c959792fc-context" class="cake-context" style="display: none;">$viewFile = '/home/brlfuser/public_html/src/Template/Layout/printlayout.ctp'

$dataForView = [

'article_current' => object(App\Model\Entity\Article) {

'id' => (int) 30950,

'title' => 'Limited outreach of subsidised crop loan scheme among small &amp; marginal farmers',

'subheading' => '',

'description' => '<br />

<div align="justify">

The budgetary support to interest subvention scheme has increased by almost 14 times between 2006-07 and 2016-17. However, the much-touted subsidised short-term credit scheme provides little help to the small and marginal farmers, apart from tenant farmers. <br />

<br />

According to the Committee on Medium-term Path on Financial Inclusion, which submitted its report in December 2015, the interest subvention scheme suffers from 3 types of defects: <strong>i.</strong> Subsidised credit may not be reaching the actual cultivators; <strong>ii.</strong> There are chances of subsidised credit being misused; and, <strong>iii.</strong> Since the interest subsidy scheme is for short-term crop loans, it discriminates against long-term loans and thereby, does not incentivise long-term capital formation in agriculture, which is required to boost farm productivity (please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3">click here</a> to access). <br />

<br />

The Committee on Medium-term Path on Financial Inclusion, which was chaired by Deepak Mohanty, in its report has, thus, recommended phasing out the interest subvention scheme and ploughing the subsidy amount into a universal crop insurance scheme for small and marginal farmers. <br />

<br />

Following the <a href="../empowerment/union-budget-73.html?pgno=2#union-budget-2016-17">budgetary allocation</a> of Rs. 15,000 crore in 2016-17 under the interest subvention scheme for short-term credit, Ashok Gulati in his article <em>No Gamechangers For Farmers</em>, written for The Indian Express (dated: 1 March, 2016) says that the credit subsidy scheme is subject to misuse by large farmers. Such farmers often borrow huge amounts of loan at subsidised rates and either invest the same in fixed deposits or lend it to those who are unable to access institutional credit at higher rates (please <a href="../latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access).<br />

<br />

Based on the All-India Debt and Investment Survey (2013), it has been shown by the Committee on Medium-term Path on Financial Inclusion that there exists an inverse relationship between the size class of land holdings and the proportion of farmers borrowing credit from money lenders, except for the land holding size classes 1.01-2.00 hectare and 2.01-4.00 hectare.

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

It means that a small proportion of farmers who cultivate on small-sized land holdings have access to institutional credit, including subsidised crop loan. Therefore, such farmers rely heavily on credit from private moneylenders, who charge exhorbitant rates. <br />

<br />

The data from All-India Debt and Investment Survey (2013) says that when the land holding size is less than 0.01 hectares, almost 13 percent, have access to credit from a formal banking institution, whereas 64 percent borrow from private moneylenders.&nbsp; &nbsp;<br />

<br />

<strong>About the Interest Subvention Scheme<br />

</strong><br />

The interest subvention scheme grants certain amount to banks every year so that they collect less interest from those farmers who repay back their debt in time.<br />

<br />

The <a href="https://www.nabard.org/english/int_sub_scheme.aspx">website</a> of National Bank for Agriculture and Rural Development (NABARD) says that the interest subvention scheme came into force with effect from <em>kharif</em> 2006-07. <br />

<br />

Following the policy of affordable short-term credit for farmers, which was announced during the budget speech of the Finance Minister in 2006-07, the Government of India provided interest subvention of 2 percent to Public Sector Banks, Regional Rural Banks and Cooperative Banks with respect to short-term production credit of upto Rs. 3 lakh provided to farmers out of their own resources, subject to the condition that they make available short-term credit @ 7 percent per annum at the ground-level. <br />

<br />

The rates for the interest subvention scheme has varied over the years, says NABARD. <br />

<br />

<em>Incentive to farmers on prompt repayments<br />

</em><br />

Since 2009-10, the Government of India revised the scheme and additional interest subvention was extended to farmers who repay their loans on or before the due date or the date fixed by the banks, subject to a maximum period of one year. <br />

<br />

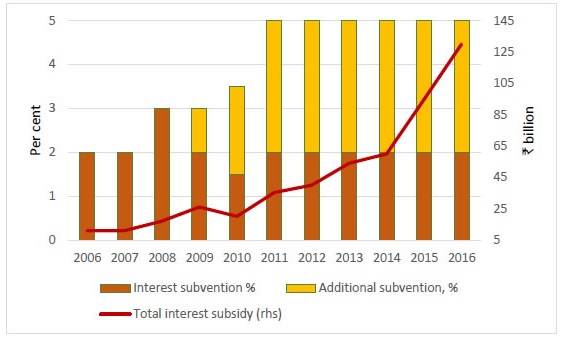

As could be seen from Chart 1 below, the interest subvention claims paid by the government have been increasing rapidly over the years. <br />

<br />

<strong>Chart 1: Interest rate subvention<br />

</strong><img src="tinymce/uploaded/Interest%20rate%20subvention.jpg" alt="Interest rate subvention" width="375" height="228" /><br />

<br />

<em><strong>Source:</strong> Report of the Committee on Medium-term Path on Financial Inclusion <br />

</em><br />

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<em>Interest subvention to small and marginal farmers against Negotiable Warehouse Receipts<br />

</em><br />

In order to discourage distress sale of farm produce by cultivators and to encourage them to store their produce in warehouses against warehouse receipts, the Government of India introduced a scheme in 2011-12 for extending concessional loans to the farmers against negotiable warehouse receipts. <br />

<br />

Post-harvest loans against Negotiable Warehouse Receipts (NWR) provided by banks to small and marginal farmers having Kisan Credit Cards, were made eligible for interest subvention, period of upto six months on the same rate as available to crop loan. However, small and marginal farmers, who did not avail crop loans through banking system, were not eligible for interest subvention. No additional subvention towards prompt repayment, as is available for crop loans, was envisaged under the scheme.<br />

<br />

<em>Interest subvention to NABARD <br />

</em><br />

As per the scheme, interest subvention would be made available to the NABARD for providing concessional refinance to Regional Rural Banks (RRBs) and Cooperative Banks. NABARD is subvented to the extent of difference between weighted average cost of funds mobilised and refinance rate. Additionally, administrative cost of 20 basis points is also provided by the Government of India.<br />

<br />

<br />

<strong><em>References:<br />

</em></strong><br />

Report of the Committee on Medium-term Path on Financial Inclusion (chaired by Deepak Mohanty), Reserve Bank of India, 28 March, 2016, please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3">click here</a> to access<br />

&nbsp;<br />

Note for Demands for Grants 2016-17, Payments to Financial Institutions, <a href="http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf">http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf</a> <br />

<br />

Note for Demands for Grants 2007-08, Payments to Financial Institutions, Ministry of Finance, please <a href="http://indiabudget.nic.in/ub2007-08/eb/sbe33.pdf">click here</a> to access &nbsp; <br />

<br />

Bank Credit to Agriculture in India in the 2000s: Dissecting the Revival -R Ramakumar and Pallavi Chavan, Review of Agrarian Studies, Vol. 4, No. 1, February-June, 2014, please <a href="http://www.ras.org.in/bank_credit_to_agriculture_in_india_in_the_2000s">click here</a> to access <br />

<br />

Counterproductive Farm Policies -PSM Rao, Outlook, 29 March, 2016, please <a href="../latest-news-updates/counterproductive-farm-policies-psm-rao-4678974.html">click here</a> to access<br />

&nbsp;<br />

Bulk of crop loan interest subvention for settling earlier dues, Business Standard, 3 March, 2016, please <a href="http://www.business-standard.com/article/economy-policy/bulk-of-crop-loan-interest-subvention-for-settling-earlier-dues-116030200950_1.html">click here</a> to access

</div>

<div align="justify">

<br />

No Gamechangers For Farmers -Ashok Gulati, The Indian Express, 1 March, 2016, please <a href="../latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access <br />

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<strong>Image Courtesy: Himanshu Joshi</strong>

</div>',

'credit_writer' => '',

'article_img' => 'im4change_10Crop_loan.jpg',

'article_img_thumb' => 'im4change_10Crop_loan.jpg',

'status' => (int) 1,

'show_on_home' => (int) 1,

'lang' => 'EN',

'category_id' => (int) 4,

'tag_keyword' => '',

'seo_url' => 'limited-outreach-of-subsidised-crop-loan-scheme-among-small-marginal-farmers-4679017',

'meta_title' => null,

'meta_keywords' => null,

'meta_description' => null,

'noindex' => (int) 0,

'publish_date' => object(Cake\I18n\FrozenDate) {},

'most_visit_section_id' => null,

'article_big_img' => null,

'liveid' => (int) 4679017,

'created' => object(Cake\I18n\FrozenTime) {},

'modified' => object(Cake\I18n\FrozenTime) {},

'edate' => '',

'tags' => [

[maximum depth reached]

],

'category' => object(App\Model\Entity\Category) {},

'[new]' => false,

'[accessible]' => [

[maximum depth reached]

],

'[dirty]' => [[maximum depth reached]],

'[original]' => [[maximum depth reached]],

'[virtual]' => [[maximum depth reached]],

'[hasErrors]' => false,

'[errors]' => [[maximum depth reached]],

'[invalid]' => [[maximum depth reached]],

'[repository]' => 'Articles'

},

'articleid' => (int) 30950,

'metaTitle' => 'NEWS ALERTS | Limited outreach of subsidised crop loan scheme among small &amp; marginal farmers',

'metaKeywords' => 'NABARD,Access to credit,Indebtedness,Institutional Credit,Small and Marginal Farmers,Interest Rates,Interest subsidy,interest subvention,Interest Subvention Scheme,Rural Credit,Farm Loans',

'metaDesc' => '

The budgetary support to interest subvention scheme has increased by almost 14 times between 2006-07 and 2016-17. However, the much-touted subsidised short-term credit scheme provides little help to the small and marginal farmers, apart from tenant farmers.

According to the...',

'disp' => '<br /><div align="justify">The budgetary support to interest subvention scheme has increased by almost 14 times between 2006-07 and 2016-17. However, the much-touted subsidised short-term credit scheme provides little help to the small and marginal farmers, apart from tenant farmers. <br /><br />According to the Committee on Medium-term Path on Financial Inclusion, which submitted its report in December 2015, the interest subvention scheme suffers from 3 types of defects: <strong>i.</strong> Subsidised credit may not be reaching the actual cultivators; <strong>ii.</strong> There are chances of subsidised credit being misused; and, <strong>iii.</strong> Since the interest subsidy scheme is for short-term crop loans, it discriminates against long-term loans and thereby, does not incentivise long-term capital formation in agriculture, which is required to boost farm productivity (please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3" title="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3">click here</a> to access). <br /><br />The Committee on Medium-term Path on Financial Inclusion, which was chaired by Deepak Mohanty, in its report has, thus, recommended phasing out the interest subvention scheme and ploughing the subsidy amount into a universal crop insurance scheme for small and marginal farmers. <br /><br />Following the <a href="https://im4change.in/empowerment/union-budget-73.html?pgno=2#union-budget-2016-17" title="https://im4change.in/empowerment/union-budget-73.html?pgno=2#union-budget-2016-17">budgetary allocation</a> of Rs. 15,000 crore in 2016-17 under the interest subvention scheme for short-term credit, Ashok Gulati in his article <em>No Gamechangers For Farmers</em>, written for The Indian Express (dated: 1 March, 2016) says that the credit subsidy scheme is subject to misuse by large farmers. Such farmers often borrow huge amounts of loan at subsidised rates and either invest the same in fixed deposits or lend it to those who are unable to access institutional credit at higher rates (please <a href="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html" title="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access).<br /><br />Based on the All-India Debt and Investment Survey (2013), it has been shown by the Committee on Medium-term Path on Financial Inclusion that there exists an inverse relationship between the size class of land holdings and the proportion of farmers borrowing credit from money lenders, except for the land holding size classes 1.01-2.00 hectare and 2.01-4.00 hectare.</div><div align="justify">&nbsp;</div><div align="justify">It means that a small proportion of farmers who cultivate on small-sized land holdings have access to institutional credit, including subsidised crop loan. Therefore, such farmers rely heavily on credit from private moneylenders, who charge exhorbitant rates. <br /><br />The data from All-India Debt and Investment Survey (2013) says that when the land holding size is less than 0.01 hectares, almost 13 percent, have access to credit from a formal banking institution, whereas 64 percent borrow from private moneylenders.&nbsp; &nbsp;<br /><br /><strong>About the Interest Subvention Scheme<br /></strong><br />The interest subvention scheme grants certain amount to banks every year so that they collect less interest from those farmers who repay back their debt in time.<br /><br />The <a href="https://www.nabard.org/english/int_sub_scheme.aspx" title="https://www.nabard.org/english/int_sub_scheme.aspx">website</a> of National Bank for Agriculture and Rural Development (NABARD) says that the interest subvention scheme came into force with effect from <em>kharif</em> 2006-07. <br /><br />Following the policy of affordable short-term credit for farmers, which was announced during the budget speech of the Finance Minister in 2006-07, the Government of India provided interest subvention of 2 percent to Public Sector Banks, Regional Rural Banks and Cooperative Banks with respect to short-term production credit of upto Rs. 3 lakh provided to farmers out of their own resources, subject to the condition that they make available short-term credit @ 7 percent per annum at the ground-level. <br /><br />The rates for the interest subvention scheme has varied over the years, says NABARD. <br /><br /><em>Incentive to farmers on prompt repayments<br /></em><br />Since 2009-10, the Government of India revised the scheme and additional interest subvention was extended to farmers who repay their loans on or before the due date or the date fixed by the banks, subject to a maximum period of one year. <br /><br />As could be seen from Chart 1 below, the interest subvention claims paid by the government have been increasing rapidly over the years. <br /><br /><strong>Chart 1: Interest rate subvention<br /></strong><img src="https://im4change.in/siteadmin/tinymce/uploaded/Interest%20rate%20subvention.jpg" alt="Interest rate subvention" width="375" height="228" /><br /><br /><em><strong>Source:</strong> Report of the Committee on Medium-term Path on Financial Inclusion <br /></em><br /></div><div align="justify">&nbsp;</div><div align="justify"><em>Interest subvention to small and marginal farmers against Negotiable Warehouse Receipts<br /></em><br />In order to discourage distress sale of farm produce by cultivators and to encourage them to store their produce in warehouses against warehouse receipts, the Government of India introduced a scheme in 2011-12 for extending concessional loans to the farmers against negotiable warehouse receipts. <br /><br />Post-harvest loans against Negotiable Warehouse Receipts (NWR) provided by banks to small and marginal farmers having Kisan Credit Cards, were made eligible for interest subvention, period of upto six months on the same rate as available to crop loan. However, small and marginal farmers, who did not avail crop loans through banking system, were not eligible for interest subvention. No additional subvention towards prompt repayment, as is available for crop loans, was envisaged under the scheme.<br /><br /><em>Interest subvention to NABARD <br /></em><br />As per the scheme, interest subvention would be made available to the NABARD for providing concessional refinance to Regional Rural Banks (RRBs) and Cooperative Banks. NABARD is subvented to the extent of difference between weighted average cost of funds mobilised and refinance rate. Additionally, administrative cost of 20 basis points is also provided by the Government of India.<br /><br /><br /><strong><em>References:<br /></em></strong><br />Report of the Committee on Medium-term Path on Financial Inclusion (chaired by Deepak Mohanty), Reserve Bank of India, 28 March, 2016, please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3" title="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3">click here</a> to access<br />&nbsp;<br />Note for Demands for Grants 2016-17, Payments to Financial Institutions, <a href="http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf" title="http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf">http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf</a> <br /><br />Note for Demands for Grants 2007-08, Payments to Financial Institutions, Ministry of Finance, please <a href="http://indiabudget.nic.in/ub2007-08/eb/sbe33.pdf" title="http://indiabudget.nic.in/ub2007-08/eb/sbe33.pdf">click here</a> to access &nbsp; <br /><br />Bank Credit to Agriculture in India in the 2000s: Dissecting the Revival -R Ramakumar and Pallavi Chavan, Review of Agrarian Studies, Vol. 4, No. 1, February-June, 2014, please <a href="http://www.ras.org.in/bank_credit_to_agriculture_in_india_in_the_2000s" title="http://www.ras.org.in/bank_credit_to_agriculture_in_india_in_the_2000s">click here</a> to access <br /><br />Counterproductive Farm Policies -PSM Rao, Outlook, 29 March, 2016, please <a href="https://im4change.in/latest-news-updates/counterproductive-farm-policies-psm-rao-4678974.html" title="https://im4change.in/latest-news-updates/counterproductive-farm-policies-psm-rao-4678974.html">click here</a> to access<br />&nbsp;<br />Bulk of crop loan interest subvention for settling earlier dues, Business Standard, 3 March, 2016, please <a href="http://www.business-standard.com/article/economy-policy/bulk-of-crop-loan-interest-subvention-for-settling-earlier-dues-116030200950_1.html" title="http://www.business-standard.com/article/economy-policy/bulk-of-crop-loan-interest-subvention-for-settling-earlier-dues-116030200950_1.html">click here</a> to access</div><div align="justify"><br />No Gamechangers For Farmers -Ashok Gulati, The Indian Express, 1 March, 2016, please <a href="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html" title="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access <br /></div><div align="justify">&nbsp;</div><div align="justify"><strong>Image Courtesy: Himanshu Joshi</strong></div>',

'lang' => 'English',

'SITE_URL' => 'https://im4change.in/',

'site_title' => 'im4change',

'adminprix' => 'admin'

]

$article_current = object(App\Model\Entity\Article) {

'id' => (int) 30950,

'title' => 'Limited outreach of subsidised crop loan scheme among small &amp; marginal farmers',

'subheading' => '',

'description' => '<br />

<div align="justify">

The budgetary support to interest subvention scheme has increased by almost 14 times between 2006-07 and 2016-17. However, the much-touted subsidised short-term credit scheme provides little help to the small and marginal farmers, apart from tenant farmers. <br />

<br />

According to the Committee on Medium-term Path on Financial Inclusion, which submitted its report in December 2015, the interest subvention scheme suffers from 3 types of defects: <strong>i.</strong> Subsidised credit may not be reaching the actual cultivators; <strong>ii.</strong> There are chances of subsidised credit being misused; and, <strong>iii.</strong> Since the interest subsidy scheme is for short-term crop loans, it discriminates against long-term loans and thereby, does not incentivise long-term capital formation in agriculture, which is required to boost farm productivity (please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3">click here</a> to access). <br />

<br />

The Committee on Medium-term Path on Financial Inclusion, which was chaired by Deepak Mohanty, in its report has, thus, recommended phasing out the interest subvention scheme and ploughing the subsidy amount into a universal crop insurance scheme for small and marginal farmers. <br />

<br />

Following the <a href="../empowerment/union-budget-73.html?pgno=2#union-budget-2016-17">budgetary allocation</a> of Rs. 15,000 crore in 2016-17 under the interest subvention scheme for short-term credit, Ashok Gulati in his article <em>No Gamechangers For Farmers</em>, written for The Indian Express (dated: 1 March, 2016) says that the credit subsidy scheme is subject to misuse by large farmers. Such farmers often borrow huge amounts of loan at subsidised rates and either invest the same in fixed deposits or lend it to those who are unable to access institutional credit at higher rates (please <a href="../latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access).<br />

<br />

Based on the All-India Debt and Investment Survey (2013), it has been shown by the Committee on Medium-term Path on Financial Inclusion that there exists an inverse relationship between the size class of land holdings and the proportion of farmers borrowing credit from money lenders, except for the land holding size classes 1.01-2.00 hectare and 2.01-4.00 hectare.

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

It means that a small proportion of farmers who cultivate on small-sized land holdings have access to institutional credit, including subsidised crop loan. Therefore, such farmers rely heavily on credit from private moneylenders, who charge exhorbitant rates. <br />

<br />

The data from All-India Debt and Investment Survey (2013) says that when the land holding size is less than 0.01 hectares, almost 13 percent, have access to credit from a formal banking institution, whereas 64 percent borrow from private moneylenders.&nbsp; &nbsp;<br />

<br />

<strong>About the Interest Subvention Scheme<br />

</strong><br />

The interest subvention scheme grants certain amount to banks every year so that they collect less interest from those farmers who repay back their debt in time.<br />

<br />

The <a href="https://www.nabard.org/english/int_sub_scheme.aspx">website</a> of National Bank for Agriculture and Rural Development (NABARD) says that the interest subvention scheme came into force with effect from <em>kharif</em> 2006-07. <br />

<br />

Following the policy of affordable short-term credit for farmers, which was announced during the budget speech of the Finance Minister in 2006-07, the Government of India provided interest subvention of 2 percent to Public Sector Banks, Regional Rural Banks and Cooperative Banks with respect to short-term production credit of upto Rs. 3 lakh provided to farmers out of their own resources, subject to the condition that they make available short-term credit @ 7 percent per annum at the ground-level. <br />

<br />

The rates for the interest subvention scheme has varied over the years, says NABARD. <br />

<br />

<em>Incentive to farmers on prompt repayments<br />

</em><br />

Since 2009-10, the Government of India revised the scheme and additional interest subvention was extended to farmers who repay their loans on or before the due date or the date fixed by the banks, subject to a maximum period of one year. <br />

<br />

As could be seen from Chart 1 below, the interest subvention claims paid by the government have been increasing rapidly over the years. <br />

<br />

<strong>Chart 1: Interest rate subvention<br />

</strong><img src="tinymce/uploaded/Interest%20rate%20subvention.jpg" alt="Interest rate subvention" width="375" height="228" /><br />

<br />

<em><strong>Source:</strong> Report of the Committee on Medium-term Path on Financial Inclusion <br />

</em><br />

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<em>Interest subvention to small and marginal farmers against Negotiable Warehouse Receipts<br />

</em><br />

In order to discourage distress sale of farm produce by cultivators and to encourage them to store their produce in warehouses against warehouse receipts, the Government of India introduced a scheme in 2011-12 for extending concessional loans to the farmers against negotiable warehouse receipts. <br />

<br />

Post-harvest loans against Negotiable Warehouse Receipts (NWR) provided by banks to small and marginal farmers having Kisan Credit Cards, were made eligible for interest subvention, period of upto six months on the same rate as available to crop loan. However, small and marginal farmers, who did not avail crop loans through banking system, were not eligible for interest subvention. No additional subvention towards prompt repayment, as is available for crop loans, was envisaged under the scheme.<br />

<br />

<em>Interest subvention to NABARD <br />

</em><br />

As per the scheme, interest subvention would be made available to the NABARD for providing concessional refinance to Regional Rural Banks (RRBs) and Cooperative Banks. NABARD is subvented to the extent of difference between weighted average cost of funds mobilised and refinance rate. Additionally, administrative cost of 20 basis points is also provided by the Government of India.<br />

<br />

<br />

<strong><em>References:<br />

</em></strong><br />

Report of the Committee on Medium-term Path on Financial Inclusion (chaired by Deepak Mohanty), Reserve Bank of India, 28 March, 2016, please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3">click here</a> to access<br />

&nbsp;<br />

Note for Demands for Grants 2016-17, Payments to Financial Institutions, <a href="http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf">http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf</a> <br />

<br />

Note for Demands for Grants 2007-08, Payments to Financial Institutions, Ministry of Finance, please <a href="http://indiabudget.nic.in/ub2007-08/eb/sbe33.pdf">click here</a> to access &nbsp; <br />

<br />

Bank Credit to Agriculture in India in the 2000s: Dissecting the Revival -R Ramakumar and Pallavi Chavan, Review of Agrarian Studies, Vol. 4, No. 1, February-June, 2014, please <a href="http://www.ras.org.in/bank_credit_to_agriculture_in_india_in_the_2000s">click here</a> to access <br />

<br />

Counterproductive Farm Policies -PSM Rao, Outlook, 29 March, 2016, please <a href="../latest-news-updates/counterproductive-farm-policies-psm-rao-4678974.html">click here</a> to access<br />

&nbsp;<br />

Bulk of crop loan interest subvention for settling earlier dues, Business Standard, 3 March, 2016, please <a href="http://www.business-standard.com/article/economy-policy/bulk-of-crop-loan-interest-subvention-for-settling-earlier-dues-116030200950_1.html">click here</a> to access

</div>

<div align="justify">

<br />

No Gamechangers For Farmers -Ashok Gulati, The Indian Express, 1 March, 2016, please <a href="../latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access <br />

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<strong>Image Courtesy: Himanshu Joshi</strong>

</div>',

'credit_writer' => '',

'article_img' => 'im4change_10Crop_loan.jpg',

'article_img_thumb' => 'im4change_10Crop_loan.jpg',

'status' => (int) 1,

'show_on_home' => (int) 1,

'lang' => 'EN',

'category_id' => (int) 4,

'tag_keyword' => '',

'seo_url' => 'limited-outreach-of-subsidised-crop-loan-scheme-among-small-marginal-farmers-4679017',

'meta_title' => null,

'meta_keywords' => null,

'meta_description' => null,

'noindex' => (int) 0,

'publish_date' => object(Cake\I18n\FrozenDate) {},

'most_visit_section_id' => null,

'article_big_img' => null,

'liveid' => (int) 4679017,

'created' => object(Cake\I18n\FrozenTime) {},

'modified' => object(Cake\I18n\FrozenTime) {},

'edate' => '',

'tags' => [

(int) 0 => object(Cake\ORM\Entity) {},

(int) 1 => object(Cake\ORM\Entity) {},

(int) 2 => object(Cake\ORM\Entity) {},

(int) 3 => object(Cake\ORM\Entity) {},

(int) 4 => object(Cake\ORM\Entity) {},

(int) 5 => object(Cake\ORM\Entity) {},

(int) 6 => object(Cake\ORM\Entity) {},

(int) 7 => object(Cake\ORM\Entity) {},

(int) 8 => object(Cake\ORM\Entity) {},

(int) 9 => object(Cake\ORM\Entity) {},

(int) 10 => object(Cake\ORM\Entity) {}

],

'category' => object(App\Model\Entity\Category) {},

'[new]' => false,

'[accessible]' => [

'*' => true,

'id' => false

],

'[dirty]' => [],

'[original]' => [],

'[virtual]' => [],

'[hasErrors]' => false,

'[errors]' => [],

'[invalid]' => [],

'[repository]' => 'Articles'

}

$articleid = (int) 30950

$metaTitle = 'NEWS ALERTS | Limited outreach of subsidised crop loan scheme among small &amp; marginal farmers'

$metaKeywords = 'NABARD,Access to credit,Indebtedness,Institutional Credit,Small and Marginal Farmers,Interest Rates,Interest subsidy,interest subvention,Interest Subvention Scheme,Rural Credit,Farm Loans'

$metaDesc = '

The budgetary support to interest subvention scheme has increased by almost 14 times between 2006-07 and 2016-17. However, the much-touted subsidised short-term credit scheme provides little help to the small and marginal farmers, apart from tenant farmers.

According to the...'

$disp = '<br /><div align="justify">The budgetary support to interest subvention scheme has increased by almost 14 times between 2006-07 and 2016-17. However, the much-touted subsidised short-term credit scheme provides little help to the small and marginal farmers, apart from tenant farmers. <br /><br />According to the Committee on Medium-term Path on Financial Inclusion, which submitted its report in December 2015, the interest subvention scheme suffers from 3 types of defects: <strong>i.</strong> Subsidised credit may not be reaching the actual cultivators; <strong>ii.</strong> There are chances of subsidised credit being misused; and, <strong>iii.</strong> Since the interest subsidy scheme is for short-term crop loans, it discriminates against long-term loans and thereby, does not incentivise long-term capital formation in agriculture, which is required to boost farm productivity (please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3" title="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3">click here</a> to access). <br /><br />The Committee on Medium-term Path on Financial Inclusion, which was chaired by Deepak Mohanty, in its report has, thus, recommended phasing out the interest subvention scheme and ploughing the subsidy amount into a universal crop insurance scheme for small and marginal farmers. <br /><br />Following the <a href="https://im4change.in/empowerment/union-budget-73.html?pgno=2#union-budget-2016-17" title="https://im4change.in/empowerment/union-budget-73.html?pgno=2#union-budget-2016-17">budgetary allocation</a> of Rs. 15,000 crore in 2016-17 under the interest subvention scheme for short-term credit, Ashok Gulati in his article <em>No Gamechangers For Farmers</em>, written for The Indian Express (dated: 1 March, 2016) says that the credit subsidy scheme is subject to misuse by large farmers. Such farmers often borrow huge amounts of loan at subsidised rates and either invest the same in fixed deposits or lend it to those who are unable to access institutional credit at higher rates (please <a href="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html" title="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access).<br /><br />Based on the All-India Debt and Investment Survey (2013), it has been shown by the Committee on Medium-term Path on Financial Inclusion that there exists an inverse relationship between the size class of land holdings and the proportion of farmers borrowing credit from money lenders, except for the land holding size classes 1.01-2.00 hectare and 2.01-4.00 hectare.</div><div align="justify">&nbsp;</div><div align="justify">It means that a small proportion of farmers who cultivate on small-sized land holdings have access to institutional credit, including subsidised crop loan. Therefore, such farmers rely heavily on credit from private moneylenders, who charge exhorbitant rates. <br /><br />The data from All-India Debt and Investment Survey (2013) says that when the land holding size is less than 0.01 hectares, almost 13 percent, have access to credit from a formal banking institution, whereas 64 percent borrow from private moneylenders.&nbsp; &nbsp;<br /><br /><strong>About the Interest Subvention Scheme<br /></strong><br />The interest subvention scheme grants certain amount to banks every year so that they collect less interest from those farmers who repay back their debt in time.<br /><br />The <a href="https://www.nabard.org/english/int_sub_scheme.aspx" title="https://www.nabard.org/english/int_sub_scheme.aspx">website</a> of National Bank for Agriculture and Rural Development (NABARD) says that the interest subvention scheme came into force with effect from <em>kharif</em> 2006-07. <br /><br />Following the policy of affordable short-term credit for farmers, which was announced during the budget speech of the Finance Minister in 2006-07, the Government of India provided interest subvention of 2 percent to Public Sector Banks, Regional Rural Banks and Cooperative Banks with respect to short-term production credit of upto Rs. 3 lakh provided to farmers out of their own resources, subject to the condition that they make available short-term credit @ 7 percent per annum at the ground-level. <br /><br />The rates for the interest subvention scheme has varied over the years, says NABARD. <br /><br /><em>Incentive to farmers on prompt repayments<br /></em><br />Since 2009-10, the Government of India revised the scheme and additional interest subvention was extended to farmers who repay their loans on or before the due date or the date fixed by the banks, subject to a maximum period of one year. <br /><br />As could be seen from Chart 1 below, the interest subvention claims paid by the government have been increasing rapidly over the years. <br /><br /><strong>Chart 1: Interest rate subvention<br /></strong><img src="https://im4change.in/siteadmin/tinymce/uploaded/Interest%20rate%20subvention.jpg" alt="Interest rate subvention" width="375" height="228" /><br /><br /><em><strong>Source:</strong> Report of the Committee on Medium-term Path on Financial Inclusion <br /></em><br /></div><div align="justify">&nbsp;</div><div align="justify"><em>Interest subvention to small and marginal farmers against Negotiable Warehouse Receipts<br /></em><br />In order to discourage distress sale of farm produce by cultivators and to encourage them to store their produce in warehouses against warehouse receipts, the Government of India introduced a scheme in 2011-12 for extending concessional loans to the farmers against negotiable warehouse receipts. <br /><br />Post-harvest loans against Negotiable Warehouse Receipts (NWR) provided by banks to small and marginal farmers having Kisan Credit Cards, were made eligible for interest subvention, period of upto six months on the same rate as available to crop loan. However, small and marginal farmers, who did not avail crop loans through banking system, were not eligible for interest subvention. No additional subvention towards prompt repayment, as is available for crop loans, was envisaged under the scheme.<br /><br /><em>Interest subvention to NABARD <br /></em><br />As per the scheme, interest subvention would be made available to the NABARD for providing concessional refinance to Regional Rural Banks (RRBs) and Cooperative Banks. NABARD is subvented to the extent of difference between weighted average cost of funds mobilised and refinance rate. Additionally, administrative cost of 20 basis points is also provided by the Government of India.<br /><br /><br /><strong><em>References:<br /></em></strong><br />Report of the Committee on Medium-term Path on Financial Inclusion (chaired by Deepak Mohanty), Reserve Bank of India, 28 March, 2016, please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3" title="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3">click here</a> to access<br />&nbsp;<br />Note for Demands for Grants 2016-17, Payments to Financial Institutions, <a href="http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf" title="http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf">http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf</a> <br /><br />Note for Demands for Grants 2007-08, Payments to Financial Institutions, Ministry of Finance, please <a href="http://indiabudget.nic.in/ub2007-08/eb/sbe33.pdf" title="http://indiabudget.nic.in/ub2007-08/eb/sbe33.pdf">click here</a> to access &nbsp; <br /><br />Bank Credit to Agriculture in India in the 2000s: Dissecting the Revival -R Ramakumar and Pallavi Chavan, Review of Agrarian Studies, Vol. 4, No. 1, February-June, 2014, please <a href="http://www.ras.org.in/bank_credit_to_agriculture_in_india_in_the_2000s" title="http://www.ras.org.in/bank_credit_to_agriculture_in_india_in_the_2000s">click here</a> to access <br /><br />Counterproductive Farm Policies -PSM Rao, Outlook, 29 March, 2016, please <a href="https://im4change.in/latest-news-updates/counterproductive-farm-policies-psm-rao-4678974.html" title="https://im4change.in/latest-news-updates/counterproductive-farm-policies-psm-rao-4678974.html">click here</a> to access<br />&nbsp;<br />Bulk of crop loan interest subvention for settling earlier dues, Business Standard, 3 March, 2016, please <a href="http://www.business-standard.com/article/economy-policy/bulk-of-crop-loan-interest-subvention-for-settling-earlier-dues-116030200950_1.html" title="http://www.business-standard.com/article/economy-policy/bulk-of-crop-loan-interest-subvention-for-settling-earlier-dues-116030200950_1.html">click here</a> to access</div><div align="justify"><br />No Gamechangers For Farmers -Ashok Gulati, The Indian Express, 1 March, 2016, please <a href="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html" title="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access <br /></div><div align="justify">&nbsp;</div><div align="justify"><strong>Image Courtesy: Himanshu Joshi</strong></div>'

$lang = 'English'

$SITE_URL = 'https://im4change.in/'

$site_title = 'im4change'

$adminprix = 'admin'</pre><pre class="stack-trace">include - APP/Template/Layout/printlayout.ctp, line 8

Cake\View\View::_evaluate() - CORE/src/View/View.php, line 1413

Cake\View\View::_render() - CORE/src/View/View.php, line 1374

Cake\View\View::renderLayout() - CORE/src/View/View.php, line 927

Cake\View\View::render() - CORE/src/View/View.php, line 885

Cake\Controller\Controller::render() - CORE/src/Controller/Controller.php, line 791

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 126

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 88

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51</pre></div></pre>news-alerts-57/limited-outreach-of-subsidised-crop-loan-scheme-among-small-marginal-farmers-4679017.html"/>

<meta http-equiv="Content-Type" content="text/html; charset=utf-8"/>

<link href="https://im4change.in/css/control.css" rel="stylesheet" type="text/css"

media="all"/>

<title>NEWS ALERTS | Limited outreach of subsidised crop loan scheme among small & marginal farmers | Im4change.org</title>

<meta name="description" content="

The budgetary support to interest subvention scheme has increased by almost 14 times between 2006-07 and 2016-17. However, the much-touted subsidised short-term credit scheme provides little help to the small and marginal farmers, apart from tenant farmers.

According to the..."/>

<script src="https://im4change.in/js/jquery-1.10.2.js"></script>

<script type="text/javascript" src="https://im4change.in/js/jquery-migrate.min.js"></script>

<script language="javascript" type="text/javascript">

$(document).ready(function () {

var img = $("img")[0]; // Get my img elem

var pic_real_width, pic_real_height;

$("<img/>") // Make in memory copy of image to avoid css issues

.attr("src", $(img).attr("src"))

.load(function () {

pic_real_width = this.width; // Note: $(this).width() will not

pic_real_height = this.height; // work for in memory images.

});

});

</script>

<style type="text/css">

@media screen {

div.divFooter {

display: block;

}

}

@media print {

.printbutton {

display: none !important;

}

}

</style>

</head>

<body>

<table cellpadding="0" cellspacing="0" border="0" width="98%" align="center">

<tr>

<td class="top_bg">

<div class="divFooter">

<img src="https://im4change.in/images/logo1.jpg" height="59" border="0"

alt="Resource centre on India's rural distress" style="padding-top:14px;"/>

</div>

</td>

</tr>

<tr>

<td id="topspace"> </td>

</tr>

<tr id="topspace">

<td> </td>

</tr>

<tr>

<td height="50" style="border-bottom:1px solid #000; padding-top:10px;" class="printbutton">

<form><input type="button" value=" Print this page "

onclick="window.print();return false;"/></form>

</td>

</tr>

<tr>

<td width="100%">

<h1 class="news_headlines" style="font-style:normal">

<strong>Limited outreach of subsidised crop loan scheme among small & marginal farmers</strong></h1>

</td>

</tr>

<tr>

<td width="100%" style="font-family:Arial, 'Segoe Script', 'Segoe UI', sans-serif, serif"><font size="3">

<br /><div align="justify">The budgetary support to interest subvention scheme has increased by almost 14 times between 2006-07 and 2016-17. However, the much-touted subsidised short-term credit scheme provides little help to the small and marginal farmers, apart from tenant farmers. <br /><br />According to the Committee on Medium-term Path on Financial Inclusion, which submitted its report in December 2015, the interest subvention scheme suffers from 3 types of defects: <strong>i.</strong> Subsidised credit may not be reaching the actual cultivators; <strong>ii.</strong> There are chances of subsidised credit being misused; and, <strong>iii.</strong> Since the interest subsidy scheme is for short-term crop loans, it discriminates against long-term loans and thereby, does not incentivise long-term capital formation in agriculture, which is required to boost farm productivity (please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=836#CH3" title="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=836#CH3">click here</a> to access). <br /><br />The Committee on Medium-term Path on Financial Inclusion, which was chaired by Deepak Mohanty, in its report has, thus, recommended phasing out the interest subvention scheme and ploughing the subsidy amount into a universal crop insurance scheme for small and marginal farmers. <br /><br />Following the <a href="https://im4change.in/empowerment/union-budget-73.html?pgno=2#union-budget-2016-17" title="https://im4change.in/empowerment/union-budget-73.html?pgno=2#union-budget-2016-17">budgetary allocation</a> of Rs. 15,000 crore in 2016-17 under the interest subvention scheme for short-term credit, Ashok Gulati in his article <em>No Gamechangers For Farmers</em>, written for The Indian Express (dated: 1 March, 2016) says that the credit subsidy scheme is subject to misuse by large farmers. Such farmers often borrow huge amounts of loan at subsidised rates and either invest the same in fixed deposits or lend it to those who are unable to access institutional credit at higher rates (please <a href="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html" title="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access).<br /><br />Based on the All-India Debt and Investment Survey (2013), it has been shown by the Committee on Medium-term Path on Financial Inclusion that there exists an inverse relationship between the size class of land holdings and the proportion of farmers borrowing credit from money lenders, except for the land holding size classes 1.01-2.00 hectare and 2.01-4.00 hectare.</div><div align="justify"> </div><div align="justify">It means that a small proportion of farmers who cultivate on small-sized land holdings have access to institutional credit, including subsidised crop loan. Therefore, such farmers rely heavily on credit from private moneylenders, who charge exhorbitant rates. <br /><br />The data from All-India Debt and Investment Survey (2013) says that when the land holding size is less than 0.01 hectares, almost 13 percent, have access to credit from a formal banking institution, whereas 64 percent borrow from private moneylenders. <br /><br /><strong>About the Interest Subvention Scheme<br /></strong><br />The interest subvention scheme grants certain amount to banks every year so that they collect less interest from those farmers who repay back their debt in time.<br /><br />The <a href="https://www.nabard.org/english/int_sub_scheme.aspx" title="https://www.nabard.org/english/int_sub_scheme.aspx">website</a> of National Bank for Agriculture and Rural Development (NABARD) says that the interest subvention scheme came into force with effect from <em>kharif</em> 2006-07. <br /><br />Following the policy of affordable short-term credit for farmers, which was announced during the budget speech of the Finance Minister in 2006-07, the Government of India provided interest subvention of 2 percent to Public Sector Banks, Regional Rural Banks and Cooperative Banks with respect to short-term production credit of upto Rs. 3 lakh provided to farmers out of their own resources, subject to the condition that they make available short-term credit @ 7 percent per annum at the ground-level. <br /><br />The rates for the interest subvention scheme has varied over the years, says NABARD. <br /><br /><em>Incentive to farmers on prompt repayments<br /></em><br />Since 2009-10, the Government of India revised the scheme and additional interest subvention was extended to farmers who repay their loans on or before the due date or the date fixed by the banks, subject to a maximum period of one year. <br /><br />As could be seen from Chart 1 below, the interest subvention claims paid by the government have been increasing rapidly over the years. <br /><br /><strong>Chart 1: Interest rate subvention<br /></strong><img src="https://im4change.in/siteadmin/tinymce/uploaded/Interest%20rate%20subvention.jpg" alt="Interest rate subvention" width="375" height="228" /><br /><br /><em><strong>Source:</strong> Report of the Committee on Medium-term Path on Financial Inclusion <br /></em><br /></div><div align="justify"> </div><div align="justify"><em>Interest subvention to small and marginal farmers against Negotiable Warehouse Receipts<br /></em><br />In order to discourage distress sale of farm produce by cultivators and to encourage them to store their produce in warehouses against warehouse receipts, the Government of India introduced a scheme in 2011-12 for extending concessional loans to the farmers against negotiable warehouse receipts. <br /><br />Post-harvest loans against Negotiable Warehouse Receipts (NWR) provided by banks to small and marginal farmers having Kisan Credit Cards, were made eligible for interest subvention, period of upto six months on the same rate as available to crop loan. However, small and marginal farmers, who did not avail crop loans through banking system, were not eligible for interest subvention. No additional subvention towards prompt repayment, as is available for crop loans, was envisaged under the scheme.<br /><br /><em>Interest subvention to NABARD <br /></em><br />As per the scheme, interest subvention would be made available to the NABARD for providing concessional refinance to Regional Rural Banks (RRBs) and Cooperative Banks. NABARD is subvented to the extent of difference between weighted average cost of funds mobilised and refinance rate. Additionally, administrative cost of 20 basis points is also provided by the Government of India.<br /><br /><br /><strong><em>References:<br /></em></strong><br />Report of the Committee on Medium-term Path on Financial Inclusion (chaired by Deepak Mohanty), Reserve Bank of India, 28 March, 2016, please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=836#CH3" title="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=836#CH3">click here</a> to access<br /> <br />Note for Demands for Grants 2016-17, Payments to Financial Institutions, <a href="http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf" title="http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf">http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf</a> <br /><br />Note for Demands for Grants 2007-08, Payments to Financial Institutions, Ministry of Finance, please <a href="http://indiabudget.nic.in/ub2007-08/eb/sbe33.pdf" title="http://indiabudget.nic.in/ub2007-08/eb/sbe33.pdf">click here</a> to access <br /><br />Bank Credit to Agriculture in India in the 2000s: Dissecting the Revival -R Ramakumar and Pallavi Chavan, Review of Agrarian Studies, Vol. 4, No. 1, February-June, 2014, please <a href="http://www.ras.org.in/bank_credit_to_agriculture_in_india_in_the_2000s" title="http://www.ras.org.in/bank_credit_to_agriculture_in_india_in_the_2000s">click here</a> to access <br /><br />Counterproductive Farm Policies -PSM Rao, Outlook, 29 March, 2016, please <a href="https://im4change.in/latest-news-updates/counterproductive-farm-policies-psm-rao-4678974.html" title="https://im4change.in/latest-news-updates/counterproductive-farm-policies-psm-rao-4678974.html">click here</a> to access<br /> <br />Bulk of crop loan interest subvention for settling earlier dues, Business Standard, 3 March, 2016, please <a href="http://www.business-standard.com/article/economy-policy/bulk-of-crop-loan-interest-subvention-for-settling-earlier-dues-116030200950_1.html" title="http://www.business-standard.com/article/economy-policy/bulk-of-crop-loan-interest-subvention-for-settling-earlier-dues-116030200950_1.html">click here</a> to access</div><div align="justify"><br />No Gamechangers For Farmers -Ashok Gulati, The Indian Express, 1 March, 2016, please <a href="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html" title="https://im4change.in/latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access <br /></div><div align="justify"> </div><div align="justify"><strong>Image Courtesy: Himanshu Joshi</strong></div> </font>

</td>

</tr>

<tr>

<td> </td>

</tr>

<tr>

<td height="50" style="border-top:1px solid #000; border-bottom:1px solid #000;padding-top:10px;">

<form><input type="button" value=" Print this page "

onclick="window.print();return false;"/></form>

</td>

</tr>

</table></body>

</html>'

}

$maxBufferLength = (int) 8192

$file = '/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php'

$line = (int) 853

$message = 'Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853'

Cake\Http\ResponseEmitter::emit() - CORE/src/Http/ResponseEmitter.php, line 48

Cake\Http\Server::emit() - CORE/src/Http/Server.php, line 141

[main] - ROOT/webroot/index.php, line 39

Warning (2): Cannot modify header information - headers already sent by (output started at /home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php:853) [CORE/src/Http/ResponseEmitter.php, line 148]

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html PUBLIC "-//W3C//DTD XHTML 1.0 Transitional//EN"

"http://www.w3.org/TR/xhtml1/DTD/xhtml1-transitional.dtd">

<html xmlns="http://www.w3.org/1999/xhtml">

<head>

<link rel="canonical" href="https://im4change.in/<pre class="cake-error"><a href="javascript:void(0);" onclick="document.getElementById('cakeErr6824c959792fc-trace').style.display = (document.getElementById('cakeErr6824c959792fc-trace').style.display == 'none' ? '' : 'none');"><b>Notice</b> (8)</a>: Undefined variable: urlPrefix [<b>APP/Template/Layout/printlayout.ctp</b>, line <b>8</b>]<div id="cakeErr6824c959792fc-trace" class="cake-stack-trace" style="display: none;"><a href="javascript:void(0);" onclick="document.getElementById('cakeErr6824c959792fc-code').style.display = (document.getElementById('cakeErr6824c959792fc-code').style.display == 'none' ? '' : 'none')">Code</a> <a href="javascript:void(0);" onclick="document.getElementById('cakeErr6824c959792fc-context').style.display = (document.getElementById('cakeErr6824c959792fc-context').style.display == 'none' ? '' : 'none')">Context</a><pre id="cakeErr6824c959792fc-code" class="cake-code-dump" style="display: none;"><code><span style="color: #000000"><span style="color: #0000BB"></span><span style="color: #007700"><</span><span style="color: #0000BB">head</span><span style="color: #007700">>

</span></span></code>

<span class="code-highlight"><code><span style="color: #000000"> <link rel="canonical" href="<span style="color: #0000BB"><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">Configure</span><span style="color: #007700">::</span><span style="color: #0000BB">read</span><span style="color: #007700">(</span><span style="color: #DD0000">'SITE_URL'</span><span style="color: #007700">); </span><span style="color: #0000BB">?><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$urlPrefix</span><span style="color: #007700">;</span><span style="color: #0000BB">?><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$article_current</span><span style="color: #007700">-></span><span style="color: #0000BB">category</span><span style="color: #007700">-></span><span style="color: #0000BB">slug</span><span style="color: #007700">; </span><span style="color: #0000BB">?></span>/<span style="color: #0000BB"><?php </span><span style="color: #007700">echo </span><span style="color: #0000BB">$article_current</span><span style="color: #007700">-></span><span style="color: #0000BB">seo_url</span><span style="color: #007700">; </span><span style="color: #0000BB">?></span>.html"/>

</span></code></span>

<code><span style="color: #000000"><span style="color: #0000BB"> </span><span style="color: #007700"><</span><span style="color: #0000BB">meta http</span><span style="color: #007700">-</span><span style="color: #0000BB">equiv</span><span style="color: #007700">=</span><span style="color: #DD0000">"Content-Type" </span><span style="color: #0000BB">content</span><span style="color: #007700">=</span><span style="color: #DD0000">"text/html; charset=utf-8"</span><span style="color: #007700">/>

</span></span></code></pre><pre id="cakeErr6824c959792fc-context" class="cake-context" style="display: none;">$viewFile = '/home/brlfuser/public_html/src/Template/Layout/printlayout.ctp'

$dataForView = [

'article_current' => object(App\Model\Entity\Article) {

'id' => (int) 30950,

'title' => 'Limited outreach of subsidised crop loan scheme among small &amp; marginal farmers',

'subheading' => '',

'description' => '<br />

<div align="justify">

The budgetary support to interest subvention scheme has increased by almost 14 times between 2006-07 and 2016-17. However, the much-touted subsidised short-term credit scheme provides little help to the small and marginal farmers, apart from tenant farmers. <br />

<br />

According to the Committee on Medium-term Path on Financial Inclusion, which submitted its report in December 2015, the interest subvention scheme suffers from 3 types of defects: <strong>i.</strong> Subsidised credit may not be reaching the actual cultivators; <strong>ii.</strong> There are chances of subsidised credit being misused; and, <strong>iii.</strong> Since the interest subsidy scheme is for short-term crop loans, it discriminates against long-term loans and thereby, does not incentivise long-term capital formation in agriculture, which is required to boost farm productivity (please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3">click here</a> to access). <br />

<br />

The Committee on Medium-term Path on Financial Inclusion, which was chaired by Deepak Mohanty, in its report has, thus, recommended phasing out the interest subvention scheme and ploughing the subsidy amount into a universal crop insurance scheme for small and marginal farmers. <br />

<br />

Following the <a href="../empowerment/union-budget-73.html?pgno=2#union-budget-2016-17">budgetary allocation</a> of Rs. 15,000 crore in 2016-17 under the interest subvention scheme for short-term credit, Ashok Gulati in his article <em>No Gamechangers For Farmers</em>, written for The Indian Express (dated: 1 March, 2016) says that the credit subsidy scheme is subject to misuse by large farmers. Such farmers often borrow huge amounts of loan at subsidised rates and either invest the same in fixed deposits or lend it to those who are unable to access institutional credit at higher rates (please <a href="../latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access).<br />

<br />

Based on the All-India Debt and Investment Survey (2013), it has been shown by the Committee on Medium-term Path on Financial Inclusion that there exists an inverse relationship between the size class of land holdings and the proportion of farmers borrowing credit from money lenders, except for the land holding size classes 1.01-2.00 hectare and 2.01-4.00 hectare.

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

It means that a small proportion of farmers who cultivate on small-sized land holdings have access to institutional credit, including subsidised crop loan. Therefore, such farmers rely heavily on credit from private moneylenders, who charge exhorbitant rates. <br />

<br />

The data from All-India Debt and Investment Survey (2013) says that when the land holding size is less than 0.01 hectares, almost 13 percent, have access to credit from a formal banking institution, whereas 64 percent borrow from private moneylenders.&nbsp; &nbsp;<br />

<br />

<strong>About the Interest Subvention Scheme<br />

</strong><br />

The interest subvention scheme grants certain amount to banks every year so that they collect less interest from those farmers who repay back their debt in time.<br />

<br />

The <a href="https://www.nabard.org/english/int_sub_scheme.aspx">website</a> of National Bank for Agriculture and Rural Development (NABARD) says that the interest subvention scheme came into force with effect from <em>kharif</em> 2006-07. <br />

<br />

Following the policy of affordable short-term credit for farmers, which was announced during the budget speech of the Finance Minister in 2006-07, the Government of India provided interest subvention of 2 percent to Public Sector Banks, Regional Rural Banks and Cooperative Banks with respect to short-term production credit of upto Rs. 3 lakh provided to farmers out of their own resources, subject to the condition that they make available short-term credit @ 7 percent per annum at the ground-level. <br />

<br />

The rates for the interest subvention scheme has varied over the years, says NABARD. <br />

<br />

<em>Incentive to farmers on prompt repayments<br />

</em><br />

Since 2009-10, the Government of India revised the scheme and additional interest subvention was extended to farmers who repay their loans on or before the due date or the date fixed by the banks, subject to a maximum period of one year. <br />

<br />

As could be seen from Chart 1 below, the interest subvention claims paid by the government have been increasing rapidly over the years. <br />

<br />

<strong>Chart 1: Interest rate subvention<br />

</strong><img src="tinymce/uploaded/Interest%20rate%20subvention.jpg" alt="Interest rate subvention" width="375" height="228" /><br />

<br />

<em><strong>Source:</strong> Report of the Committee on Medium-term Path on Financial Inclusion <br />

</em><br />

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<em>Interest subvention to small and marginal farmers against Negotiable Warehouse Receipts<br />

</em><br />

In order to discourage distress sale of farm produce by cultivators and to encourage them to store their produce in warehouses against warehouse receipts, the Government of India introduced a scheme in 2011-12 for extending concessional loans to the farmers against negotiable warehouse receipts. <br />

<br />

Post-harvest loans against Negotiable Warehouse Receipts (NWR) provided by banks to small and marginal farmers having Kisan Credit Cards, were made eligible for interest subvention, period of upto six months on the same rate as available to crop loan. However, small and marginal farmers, who did not avail crop loans through banking system, were not eligible for interest subvention. No additional subvention towards prompt repayment, as is available for crop loans, was envisaged under the scheme.<br />

<br />

<em>Interest subvention to NABARD <br />

</em><br />

As per the scheme, interest subvention would be made available to the NABARD for providing concessional refinance to Regional Rural Banks (RRBs) and Cooperative Banks. NABARD is subvented to the extent of difference between weighted average cost of funds mobilised and refinance rate. Additionally, administrative cost of 20 basis points is also provided by the Government of India.<br />

<br />

<br />

<strong><em>References:<br />

</em></strong><br />

Report of the Committee on Medium-term Path on Financial Inclusion (chaired by Deepak Mohanty), Reserve Bank of India, 28 March, 2016, please <a href="https://rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&amp;ID=836#CH3">click here</a> to access<br />

&nbsp;<br />

Note for Demands for Grants 2016-17, Payments to Financial Institutions, <a href="http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf">http://indiabudget.nic.in/ub2016-17/eb/sbe1.pdf</a> <br />

<br />

Note for Demands for Grants 2007-08, Payments to Financial Institutions, Ministry of Finance, please <a href="http://indiabudget.nic.in/ub2007-08/eb/sbe33.pdf">click here</a> to access &nbsp; <br />

<br />

Bank Credit to Agriculture in India in the 2000s: Dissecting the Revival -R Ramakumar and Pallavi Chavan, Review of Agrarian Studies, Vol. 4, No. 1, February-June, 2014, please <a href="http://www.ras.org.in/bank_credit_to_agriculture_in_india_in_the_2000s">click here</a> to access <br />

<br />

Counterproductive Farm Policies -PSM Rao, Outlook, 29 March, 2016, please <a href="../latest-news-updates/counterproductive-farm-policies-psm-rao-4678974.html">click here</a> to access<br />

&nbsp;<br />

Bulk of crop loan interest subvention for settling earlier dues, Business Standard, 3 March, 2016, please <a href="http://www.business-standard.com/article/economy-policy/bulk-of-crop-loan-interest-subvention-for-settling-earlier-dues-116030200950_1.html">click here</a> to access

</div>

<div align="justify">

<br />

No Gamechangers For Farmers -Ashok Gulati, The Indian Express, 1 March, 2016, please <a href="../latest-news-updates/no-gamechangers-for-farmers-ashok-gulati-4678722.html">click here</a> to access <br />

</div>

<div align="justify">

&nbsp;

</div>

<div align="justify">

<strong>Image Courtesy: Himanshu Joshi</strong>

</div>',

'credit_writer' => '',

'article_img' => 'im4change_10Crop_loan.jpg',

'article_img_thumb' => 'im4change_10Crop_loan.jpg',

'status' => (int) 1,

'show_on_home' => (int) 1,

'lang' => 'EN',

'category_id' => (int) 4,

'tag_keyword' => '',

'seo_url' => 'limited-outreach-of-subsidised-crop-loan-scheme-among-small-marginal-farmers-4679017',

'meta_title' => null,

'meta_keywords' => null,

'meta_description' => null,

'noindex' => (int) 0,

'publish_date' => object(Cake\I18n\FrozenDate) {},

'most_visit_section_id' => null,

'article_big_img' => null,

'liveid' => (int) 4679017,

'created' => object(Cake\I18n\FrozenTime) {},

'modified' => object(Cake\I18n\FrozenTime) {},

'edate' => '',

'tags' => [

[maximum depth reached]

],

'category' => object(App\Model\Entity\Category) {},

'[new]' => false,

'[accessible]' => [

[maximum depth reached]

],

'[dirty]' => [[maximum depth reached]],

'[original]' => [[maximum depth reached]],

'[virtual]' => [[maximum depth reached]],

'[hasErrors]' => false,

'[errors]' => [[maximum depth reached]],

'[invalid]' => [[maximum depth reached]],

'[repository]' => 'Articles'

},

'articleid' => (int) 30950,

'metaTitle' => 'NEWS ALERTS | Limited outreach of subsidised crop loan scheme among small &amp; marginal farmers',

'metaKeywords' => 'NABARD,Access to credit,Indebtedness,Institutional Credit,Small and Marginal Farmers,Interest Rates,Interest subsidy,interest subvention,Interest Subvention Scheme,Rural Credit,Farm Loans',

'metaDesc' => '

The budgetary support to interest subvention scheme has increased by almost 14 times between 2006-07 and 2016-17. However, the much-touted subsidised short-term credit scheme provides little help to the small and marginal farmers, apart from tenant farmers.

According to the...',