Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 150

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::index() - APP/Controller/ArtileDetailController.php, line 150

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 97

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 151

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::index() - APP/Controller/ArtileDetailController.php, line 151

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 97

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Warning (512): Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853 [CORE/src/Http/ResponseEmitter.php, line 48]

if (Configure::read('debug')) {

trigger_error($message, E_USER_WARNING);

} else {

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html>

<!--[if lt IE 7 ]>

<html class="ie ie6" lang='en'> <![endif]-->

<!--[if IE 7 ]>

<html class="ie ie7" lang='en'> <![endif]-->

<!--[if IE 8 ]>

<html class="ie ie8" lang='en'> <![endif]-->

<!--[if (gte IE 9)|!(IE)]><!-->

<html lang='en'>

<!--<![endif]-->

<head><meta http-equiv="Content-Type" content="text/html; charset=utf-8">

<title>

NEWS ALERTS | Has personal loans seen a rebound ahead of the festive season? The answer is in the negative </title>

<meta name="description" content="Just before Dhanteras and Diwali this year, the Reserve Bank of India (RBI) released the November edition of its monthly bulletin. The latest RBI Monthly Bulletin says that the GDP has contracted by -8.6 percent in the second quarter of..."/>

<meta name="keywords" content="Atmanirbhar Bharat,Atmanirbhar Bharat Package 3.0,Bank for International Settlements,BIS,Dhanteras,House Price Index,Housing Loans,Housing Prices,Ministry of Road Transport & Highways,Parivahan Sewa,Personal Loans,RBI,RBI Monthly Bulletin,Real Residential Property Prices,Reserve Bank of India,Vehicle Loans,Ministry of Road Transport & Highways"/>

<meta name="news_keywords" content="Atmanirbhar Bharat,Atmanirbhar Bharat Package 3.0,Bank for International Settlements,BIS,Dhanteras,House Price Index,Housing Loans,Housing Prices,Ministry of Road Transport & Highways,Parivahan Sewa,Personal Loans,RBI,RBI Monthly Bulletin,Real Residential Property Prices,Reserve Bank of India,Vehicle Loans,Ministry of Road Transport & Highways">

<link rel="alternate" type="application/rss+xml" title="ROR" href="/ror.xml"/>

<link rel="alternate" type="application/rss+xml" title="RSS 2.0" href="/feeds/"/>

<link rel="stylesheet" href="/css/bootstrap.min.css?1697864993"/> <link rel="stylesheet" href="/css/style.css?v=1.1.2"/> <link rel="stylesheet" href="/css/style-inner.css?1577045210"/> <link rel="stylesheet" id="Oswald-css"

href="https://fonts.googleapis.com/css?family=Oswald%3Aregular%2C700&ver=3.8.1" type="text/css"

media="all">

<link rel="stylesheet" href="/css/jquery.modal.min.css?1578285302"/> <script src="/js/jquery-1.10.2.js?1575549704"></script> <script src="/js/jquery-migrate.min.js?1575549704"></script> <link rel="shortcut icon" href="/favicon.ico" title="Favicon">

<link rel="stylesheet" href="/css/jquery-ui.css?1580720609"/> <script src="/js/jquery-ui.js?1575549704"></script> <link rel="preload" as="style" href="https://www.im4change.org/css/custom.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery.modal.min.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery-ui.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/li-scroller.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<!-- <link rel="preload" as="style" href="https://www.im4change.org/css/style.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous"> -->

<link rel="preload" as="style" href="https://www.im4change.org/css/style-inner.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel='dns-prefetch' href="//im4change.org/css/custom.css" crossorigin >

<link rel="preload" as="script" href="https://www.im4change.org/js/bootstrap.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.li-scroller.1.0.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.modal.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.ui.totop.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-1.10.2.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-migrate.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-ui.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/setting.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/tie-scripts.js">

<!--[if IE]>

<script type="text/javascript">jQuery(document).ready(function () {

jQuery(".menu-item").has("ul").children("a").attr("aria-haspopup", "true");

});</script>

<![endif]-->

<!--[if lt IE 9]>

<script src="/js/html5.js"></script>

<script src="/js/selectivizr-min.js"></script>

<![endif]-->

<!--[if IE 8]>

<link rel="stylesheet" type="text/css" media="all" href="/css/ie8.css"/>

<![endif]-->

<meta property="og:title" content="NEWS ALERTS | Has personal loans seen a rebound ahead of the festive season? The answer is in the negative" />

<meta property="og:url" content="https://im4change.in/news-alerts-57/has-personal-loans-seen-a-rebound-ahead-of-the-festive-season-the-answer-is-in-the-negative.html" />

<meta property="og:type" content="article" />

<meta property="og:description" content="Just before Dhanteras and Diwali this year, the Reserve Bank of India (RBI) released the November edition of its monthly bulletin. The latest RBI Monthly Bulletin says that the GDP has contracted by -8.6 percent in the second quarter of..." />

<meta property="og:image" content="" />

<meta property="fb:app_id" content="0" />

<meta name="viewport" content="width=device-width, initial-scale=1, maximum-scale=1, user-scalable=no">

<link rel="apple-touch-icon-precomposed" sizes="144x144" href="https://im4change.in/images/apple1.png">

<link rel="apple-touch-icon-precomposed" sizes="120x120" href="https://im4change.in/images/apple2.png">

<link rel="apple-touch-icon-precomposed" sizes="72x72" href="https://im4change.in/images/apple3.png">

<link rel="apple-touch-icon-precomposed" href="https://im4change.in/images/apple4.png">

<style>

.gsc-results-wrapper-overlay{

top: 38% !important;

height: 50% !important;

}

.gsc-search-button-v2{

border-color: #035588 !important;

background-color: #035588 !important;

}

.gsib_a{

height: 30px !important;

padding: 2px 8px 1px 6px !important;

}

.gsc-search-button-v2{

height: 41px !important;

}

input.gsc-input{

background: none !important;

}

@media only screen and (max-width: 600px) {

.gsc-results-wrapper-overlay{

top: 11% !important;

width: 87% !important;

left: 9% !important;

height: 43% !important;

}

.gsc-search-button-v2{

padding: 10px 10px !important;

}

.gsc-input-box{

height: 28px !important;

}

/* .gsib_a {

padding: 0px 9px 4px 9px !important;

}*/

}

@media only screen and (min-width: 1200px) and (max-width: 1920px) {

table.gsc-search-box{

width: 15% !important;

float: right !important;

margin-top: -118px !important;

}

.gsc-search-button-v2 {

padding: 6px !important;

}

}

</style>

<script>

$(function () {

$("#accordion").accordion({

event: "click hoverintent"

});

});

/*

* hoverIntent | Copyright 2011 Brian Cherne

* http://cherne.net/brian/resources/jquery.hoverIntent.html

* modified by the jQuery UI team

*/

$.event.special.hoverintent = {

setup: function () {

$(this).bind("mouseover", jQuery.event.special.hoverintent.handler);

},

teardown: function () {

$(this).unbind("mouseover", jQuery.event.special.hoverintent.handler);

},

handler: function (event) {

var currentX, currentY, timeout,

args = arguments,

target = $(event.target),

previousX = event.pageX,

previousY = event.pageY;

function track(event) {

currentX = event.pageX;

currentY = event.pageY;

}

;

function clear() {

target

.unbind("mousemove", track)

.unbind("mouseout", clear);

clearTimeout(timeout);

}

function handler() {

var prop,

orig = event;

if ((Math.abs(previousX - currentX) +

Math.abs(previousY - currentY)) < 7) {

clear();

event = $.Event("hoverintent");

for (prop in orig) {

if (!(prop in event)) {

event[prop] = orig[prop];

}

}

// Prevent accessing the original event since the new event

// is fired asynchronously and the old event is no longer

// usable (#6028)

delete event.originalEvent;

target.trigger(event);

} else {

previousX = currentX;

previousY = currentY;

timeout = setTimeout(handler, 100);

}

}

timeout = setTimeout(handler, 100);

target.bind({

mousemove: track,

mouseout: clear

});

}

};

</script>

<script type="text/javascript">

var _gaq = _gaq || [];

_gaq.push(['_setAccount', 'UA-472075-3']);

_gaq.push(['_trackPageview']);

(function () {

var ga = document.createElement('script');

ga.type = 'text/javascript';

ga.async = true;

ga.src = ('https:' == document.location.protocol ? 'https://ssl' : 'http://www') + '.google-analytics.com/ga.js';

var s = document.getElementsByTagName('script')[0];

s.parentNode.insertBefore(ga, s);

})();

</script>

<link rel="stylesheet" href="/css/custom.css?v=1.16"/> <script src="/js/jquery.ui.totop.js?1575549704"></script> <script src="/js/setting.js?1575549704"></script> <link rel="manifest" href="/manifest.json">

<meta name="theme-color" content="#616163" />

<meta name="apple-mobile-web-app-capable" content="yes">

<meta name="apple-mobile-web-app-status-bar-style" content="black">

<meta name="apple-mobile-web-app-title" content="im4change">

<link rel="apple-touch-icon" href="/icons/logo-192x192.png">

</head>

<body id="top" class="home inner blog">

<div class="background-cover"></div>

<div class="wrapper animated">

<header id="theme-header" class="header_inner" style="position: relative;">

<div class="logo inner_logo" style="left:20px !important">

<a title="Home" href="https://im4change.in/">

<img src="https://im4change.in/images/logo2.jpg?1582080632" class="logo_image" alt="im4change"/> </a>

</div>

<div class="langhindi" style="color: #000;display:none;"

href="https://im4change.in/">

<a class="more-link" href="https://im4change.in/">Home</a>

<a href="https://im4change.in/hindi/" class="langbutton ">हिन्दी</a>

</div>

<nav class="fade-in animated2" id="main-nav">

<div class="container">

<div class="main-menu">

<ul class="menu" id="menu-main">

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children"

style="left: -40px;"><a

target="_blank" href="https://im4change.in/">Home</a>

</li>

<li class="menu-item mega-menu menu-item-type-taxonomy mega-menu menu-item-object-category mega-menu menu-item-has-children parent-list"

style=" margin-left: -40px;"><a href="#">KNOWLEDGE GATEWAY <span class="sub-indicator"></span>

</a>

<div class="mega-menu-block background_menu" style="padding-top:25px;">

<div class="container">

<div class="mega-menu-content">

<div class="mega-menu-item">

<h3><b>Farm Crisis</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/farmers039-suicides-14.html"

class="left postionrel">Farm Suicides </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/unemployment-30.html"

class="left postionrel">Unemployment </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/rural-distress-70.html"

class="left postionrel">Rural distress </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/migration-34.html"

class="left postionrel">Migration </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/key-facts-72.html"

class="left postionrel">Key Facts </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/debt-trap-15.html"

class="left postionrel">Debt Trap </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Empowerment</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/union-budget-73.html"

class="left postionrel">Union Budget And Other Economic Policies </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/forest-and-tribal-rights-61.html"

class="left postionrel">Forest and Tribal Rights </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-education-60.html"

class="left postionrel">Right to Education </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-food-59.html"

class="left postionrel">Right to Food </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/displacement-3279.html"

class="left postionrel">Displacement </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-work-mg-nrega-39.html"

class="left postionrel">Right to Work (MG-NREGA) </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/gender-3280.html"

class="left postionrel">GENDER </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-information-58.html"

class="left postionrel">Right to Information </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/social-audit-48.html"

class="left postionrel">Social Audit </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Hunger / HDI</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/poverty-and-inequality-20499.html"

class="left postionrel">Poverty and inequality </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/malnutrition-41.html"

class="left postionrel">Malnutrition </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/public-health-51.html"

class="left postionrel">Public Health </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/education-50.html"

class="left postionrel">Education </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/hunger-overview-40.html"

class="left postionrel">Hunger Overview </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/hdi-overview-45.html"

class="left postionrel">HDI Overview </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/pds-ration-food-security-42.html"

class="left postionrel">PDS/ Ration/ Food Security </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/sdgs-113.html"

class="left postionrel">SDGs </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/mid-day-meal-scheme-mdms-53.html"

class="left postionrel">Mid Day Meal Scheme (MDMS) </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Environment</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/time-bomb-ticking-52.html"

class="left postionrel">Time Bomb Ticking </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/water-and-sanitation-55.html"

class="left postionrel">Water and Sanitation </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/impact-on-agriculture-54.html"

class="left postionrel">Impact on Agriculture </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Law & Justice</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/social-justice-20500.html"

class="left postionrel">Social Justice </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/access-to-justice-47.html"

class="left postionrel">Access to Justice </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/human-rights-56.html"

class="left postionrel">Human Rights </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/corruption-35.html"

class="left postionrel">Corruption </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/general-insecurity-46.html"

class="left postionrel">General Insecurity </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/disaster-relief-49.html"

class="left postionrel">Disaster & Relief </a>

</p>

</div>

</div>

</div>

</div>

</li>

<li class="menu-item menu-item-type-post_type menu-item-object-page "><a target="_blank" href="https://im4change.in/nceus_reports.php">NCEUS reports</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children parent-list ">

<a target="_blank" href="https://im4change.in/about-us-9.html">About Us <span

class="sub-indicator"></span></a>

<ul class="sub-menu aboutmenu">

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/objectives-8.html">Objectives</a>

</li>

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/contactus.php">Contact

Us</a></li>

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/about-us-9.html">About

Us</a></li>

</ul>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children ">

<a target="_blank" href="https://im4change.in/fellowships.php" title="Fellowships">Fellowships</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/media-workshops.php">Workshops</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/research.php">Research</a></li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/links-64">Partners</a></li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children"

id="menu-item-539"><a target="_blank" href="https://im4change.in/hindi/"

class="langbutton langlinkfont17">हिन्दी</a></li>

</ul>

</div> </div>

<!-- <div style="float: right;">

<script async src="https://cse.google.com/cse.js?cx=18b4f2e0f11bed3dd"></script>

<div class="gcse-search"></div>

</div> -->

<div class="search-block" style=" margin-left: 8px; margin-right: 7px;">

<form method="get" id="searchform" name="searchform"

action="https://im4change.in/search"

onsubmit="return searchvalidate();">

<button class="search-button" type="submit" value="Search"></button>

<input type="text" id="s" name="qryStr" value=""

onfocus="if (this.value == 'Search...') {this.value = '';}"

onblur="if (this.value == '') {this.value = 'Search...';}">

</form>

</div>

</nav>

</header>

<div class="container">

<div id="main-content" class=" main1 container fade-in animated3 sidebar-narrow-left">

<div class="content-wrap">

<div class="content" style="width: 900px;min-height: 500px;">

<div class="background_inner innBack" align="center">

<img src="https://im4change.in/images/media/Image Personal Loans.jpg"

alt="Has personal loans seen a rebound ahead of the festive season? The answer is in the negative"

class="box_shadow mt5 imgRes" style="max-width:500px;"/>

</div>

<section class="cat-box recent-box innerCatRecent">

<h1 class="cat-box-title">Has personal loans seen a rebound ahead of the festive season? The answer is in the negative</h1>

<a href="JavaScript:void(0);" onclick="return shareArticle(57611);">

<img src="https://im4change.in/images/email.png?1582080630" border="0" width="24" align="right" alt="Share this article"/> </a>

<a href="https://im4change.in/news-alerts-57/has-personal-loans-seen-a-rebound-ahead-of-the-festive-season-the-answer-is-in-the-negative/print"

rel="nofollow">

<img src="https://im4change.in/images/icon-print.png?1582080630" border="0" width="24" align="right" alt="Share this article"/>

</a>

</section>

<section class="recent-box innerCatRecent">

<small class="pb-1"><span class="dateIcn">

<img src="https://im4change.in/images/published.svg?1582080666" alt="published"/>

Published on</span><span class="text-date"> Nov 16, 2020</span>

<span

class="dateIcn">

<img src="https://im4change.in/images/modified.svg?1582080666" alt="modified"/> Modified on </span><span class="text-date"> May 14, 2021</span>

</small>

</section>

<div class="clear"></div>

<div style="padding-top: 10px;">

<div class="innerLineHeight">

<div class="middleContent innerInput news-alerts-57">

<table>

<tr>

<td>

<div>

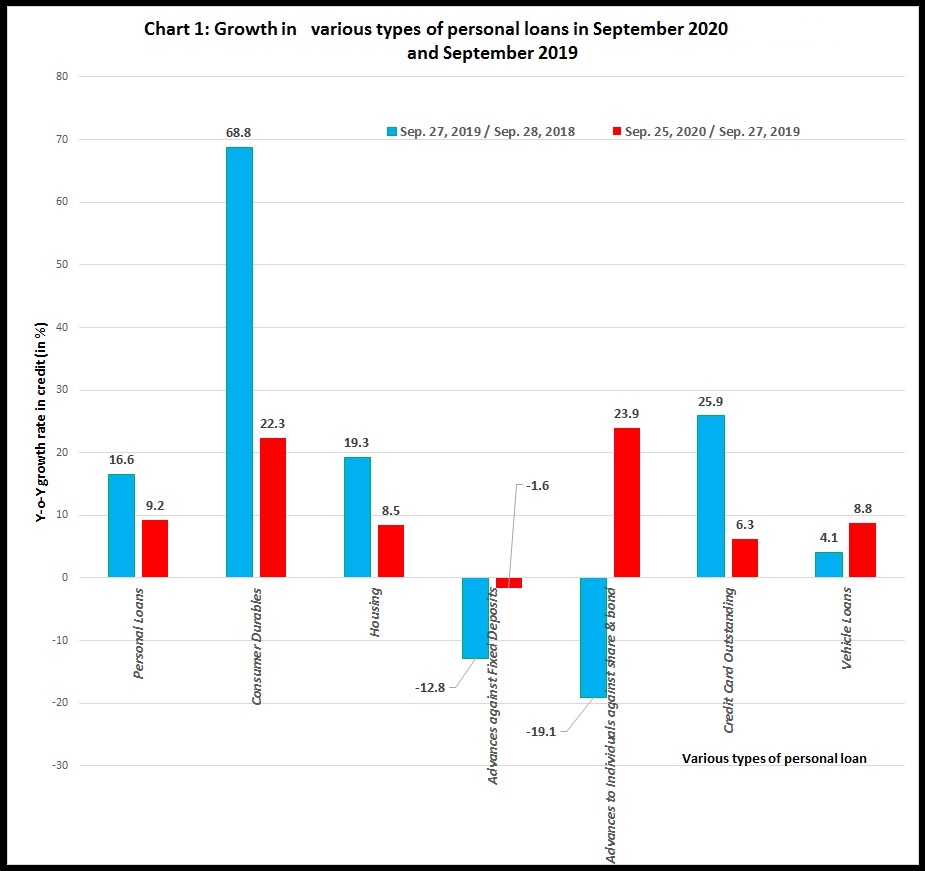

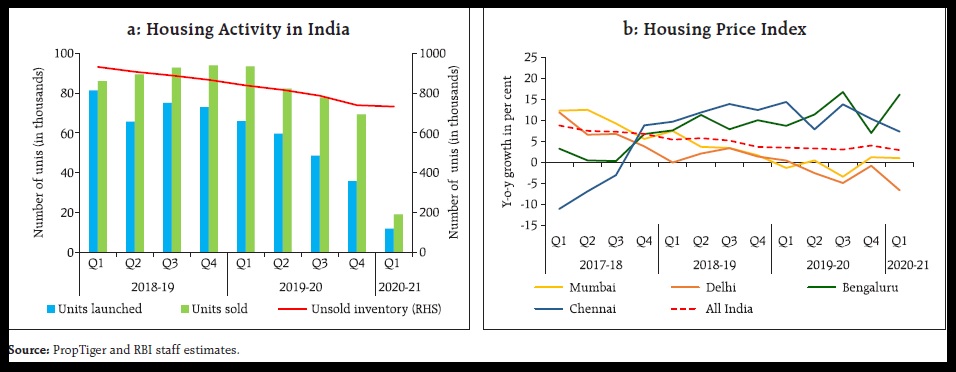

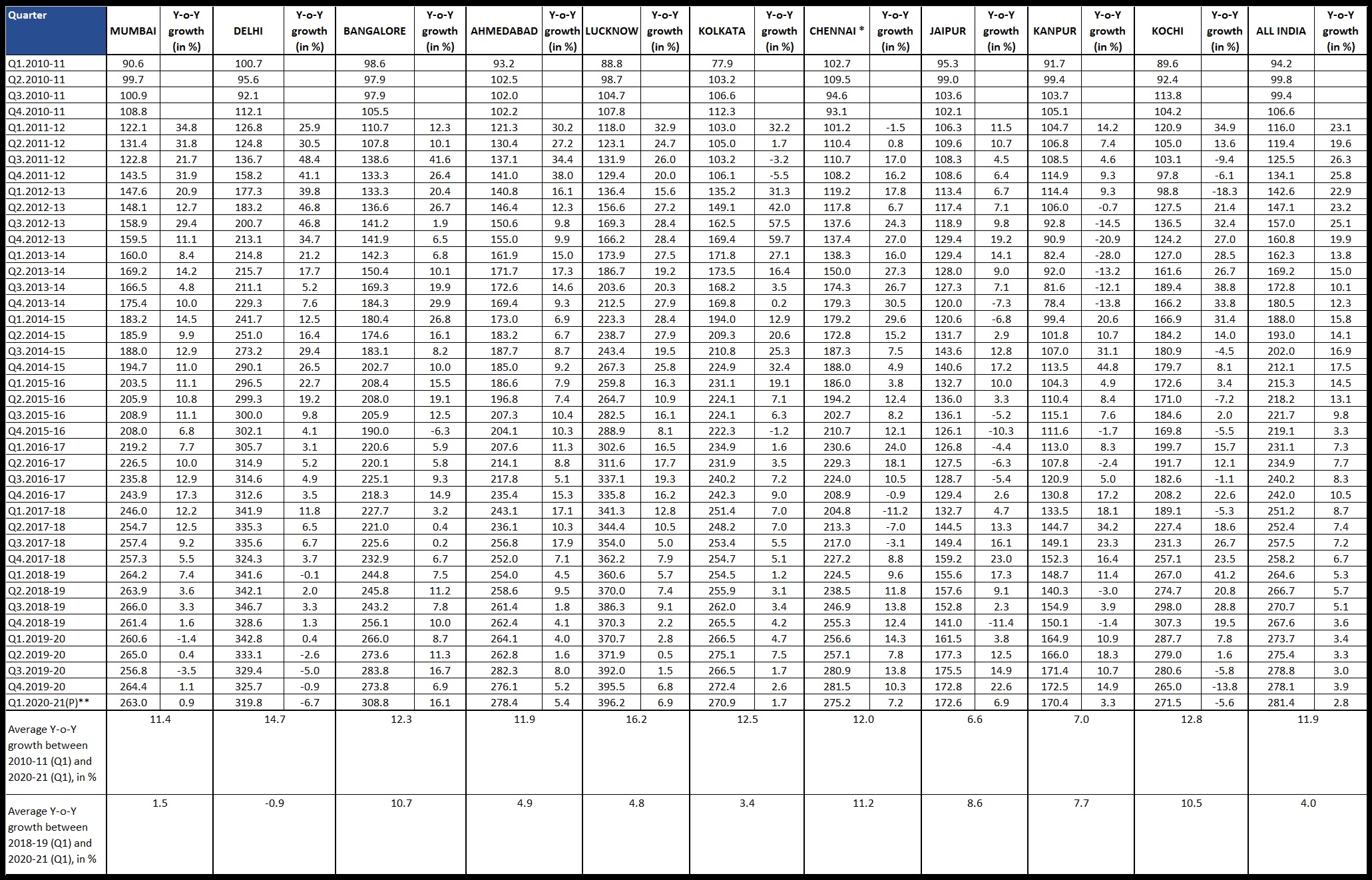

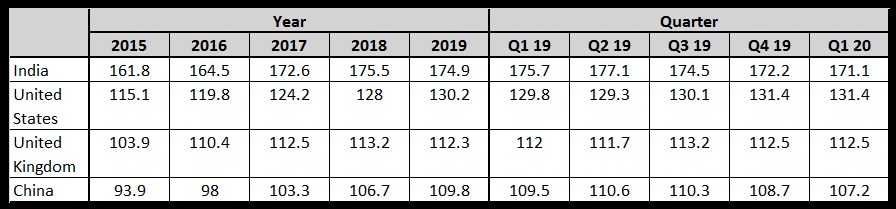

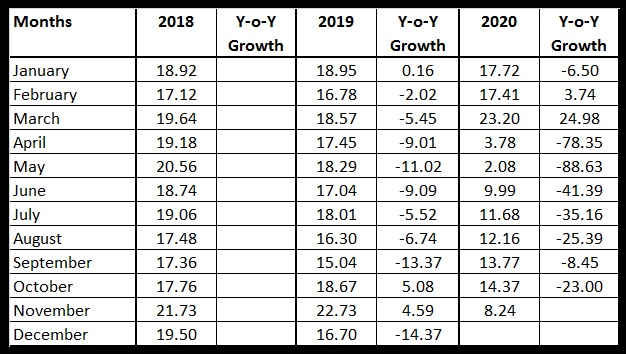

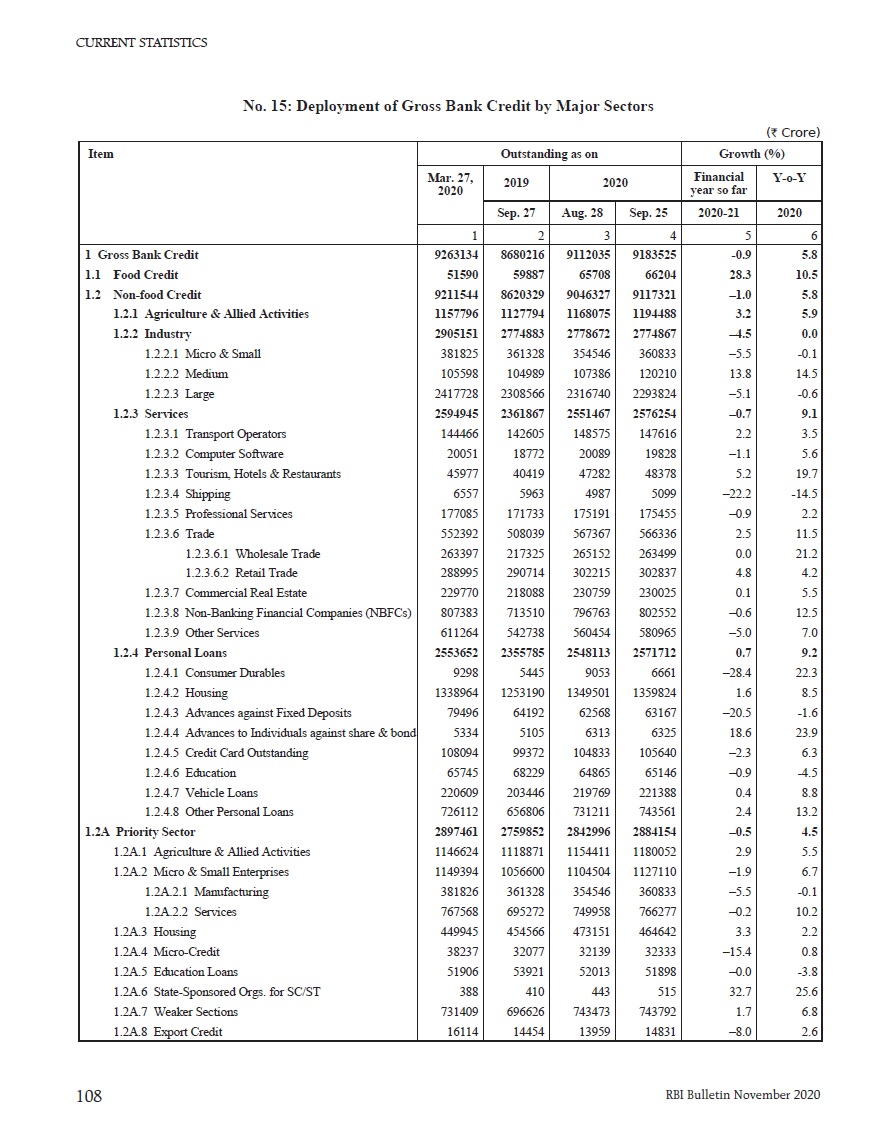

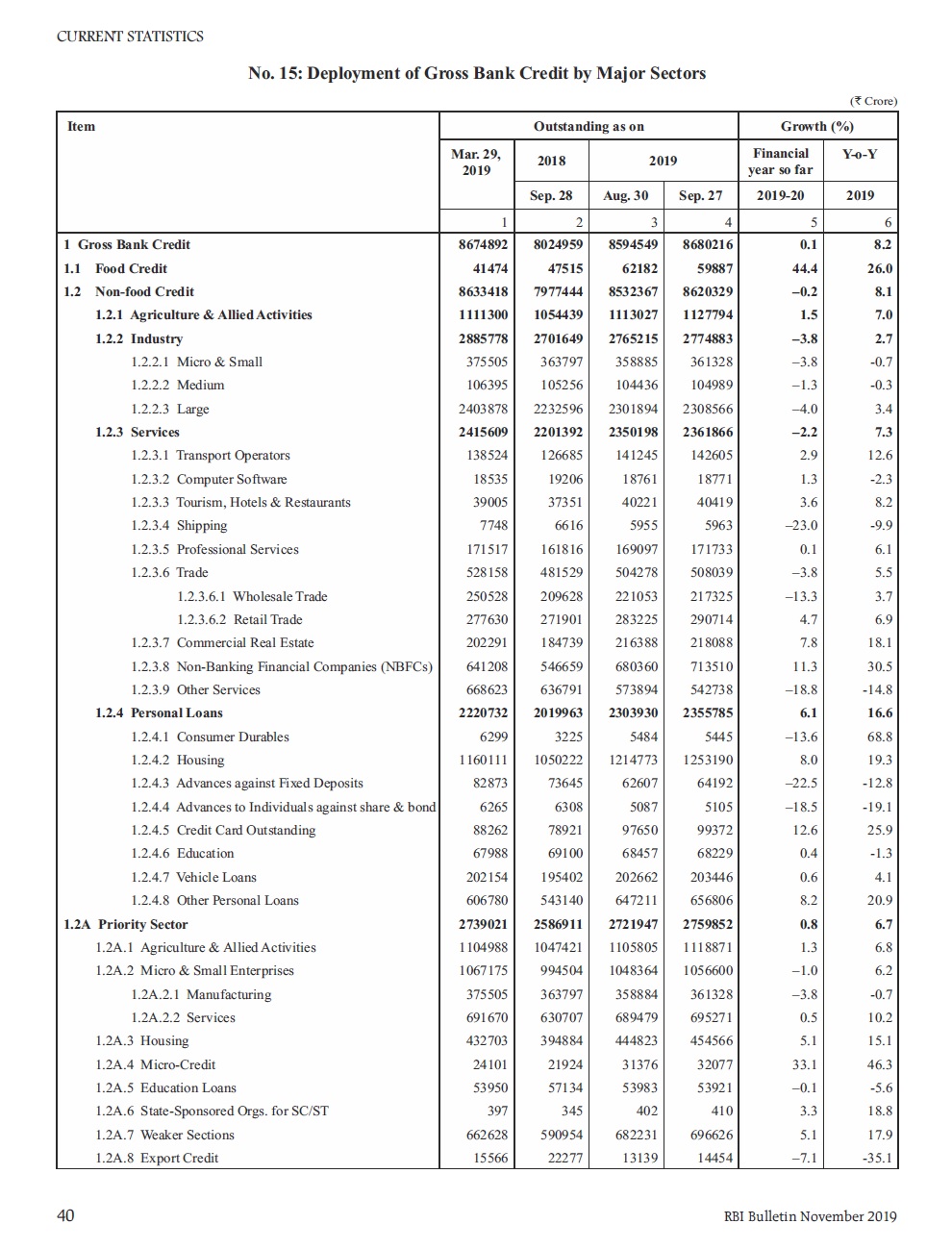

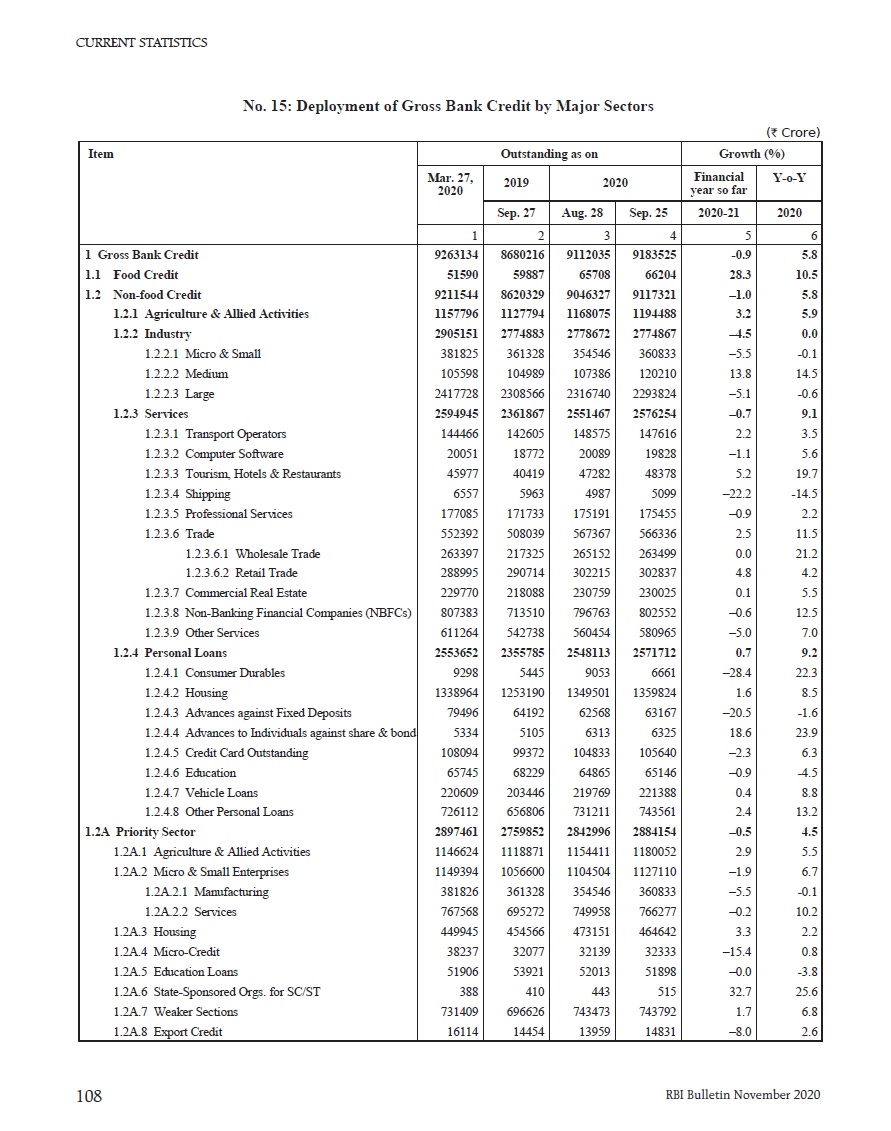

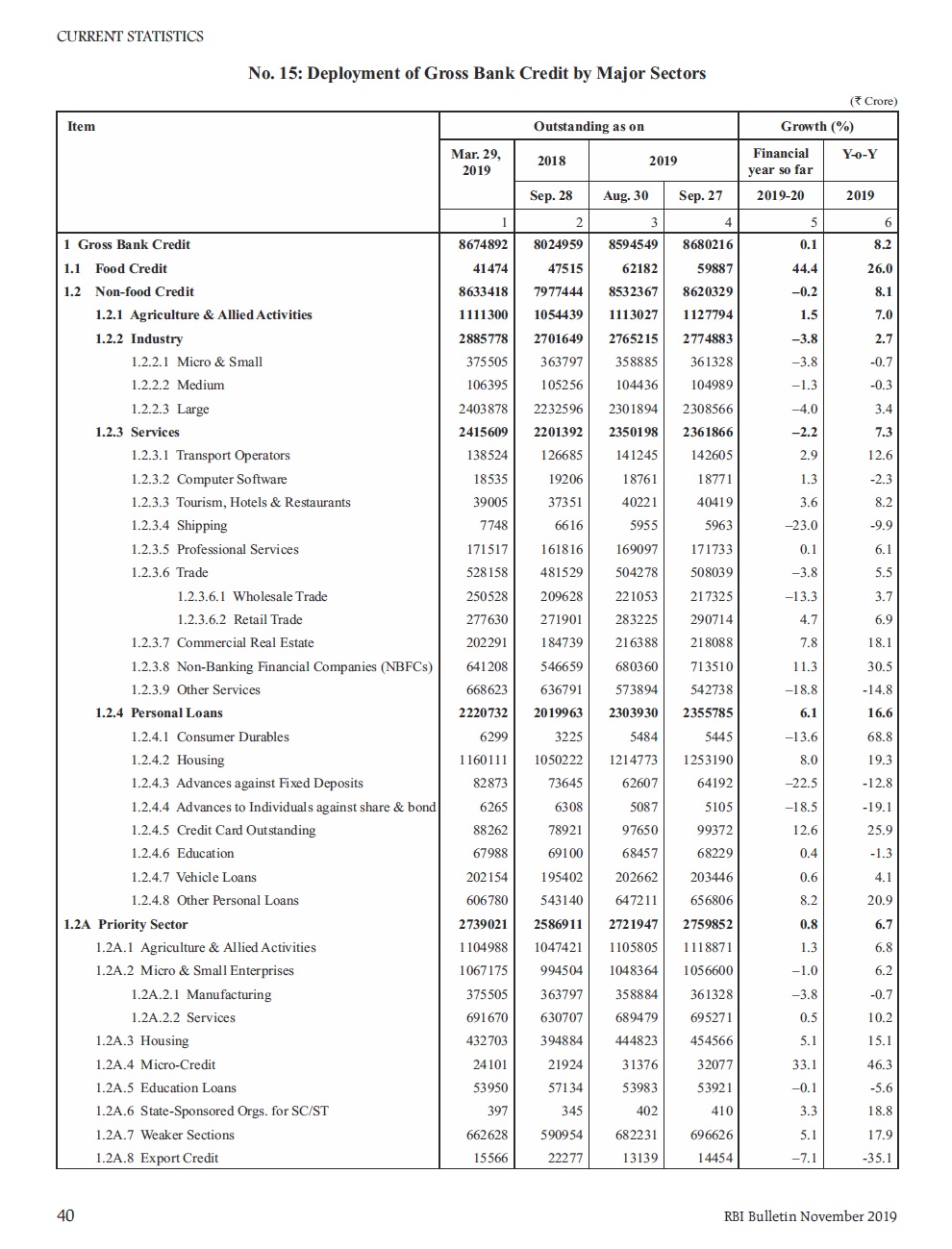

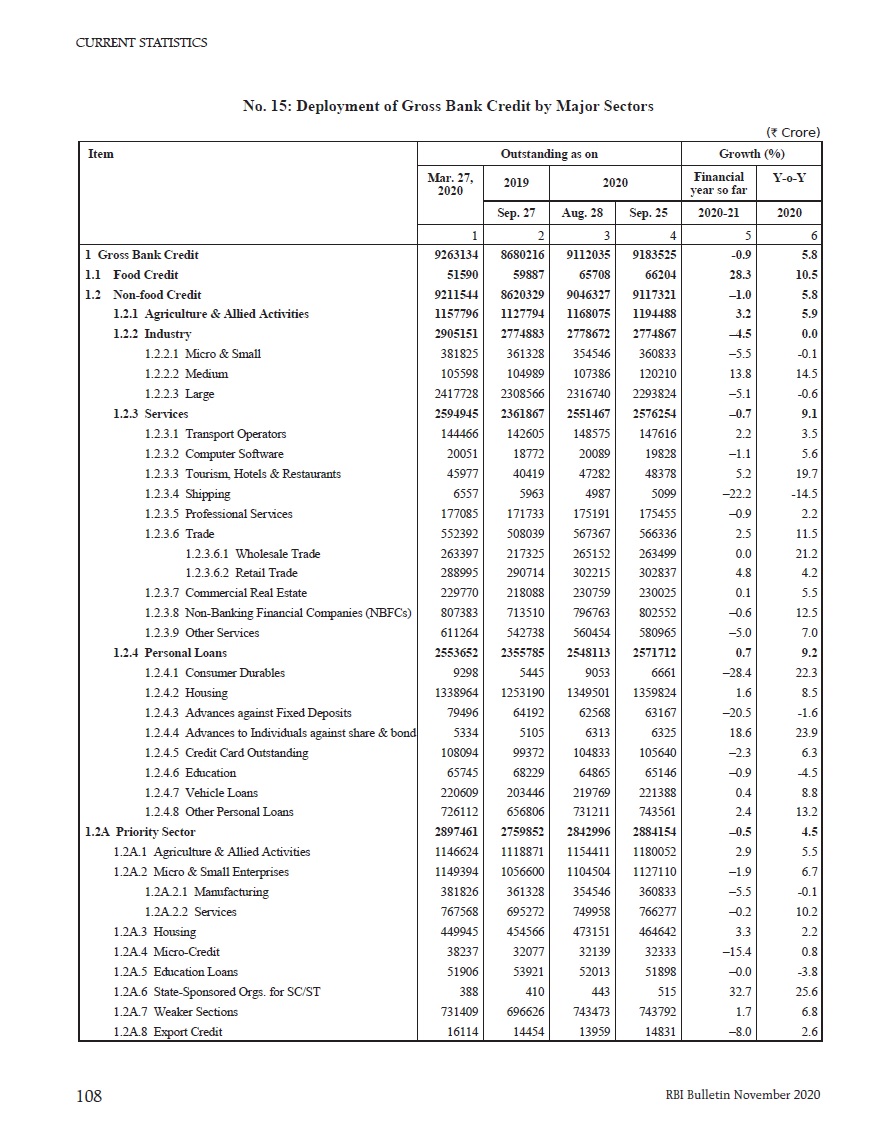

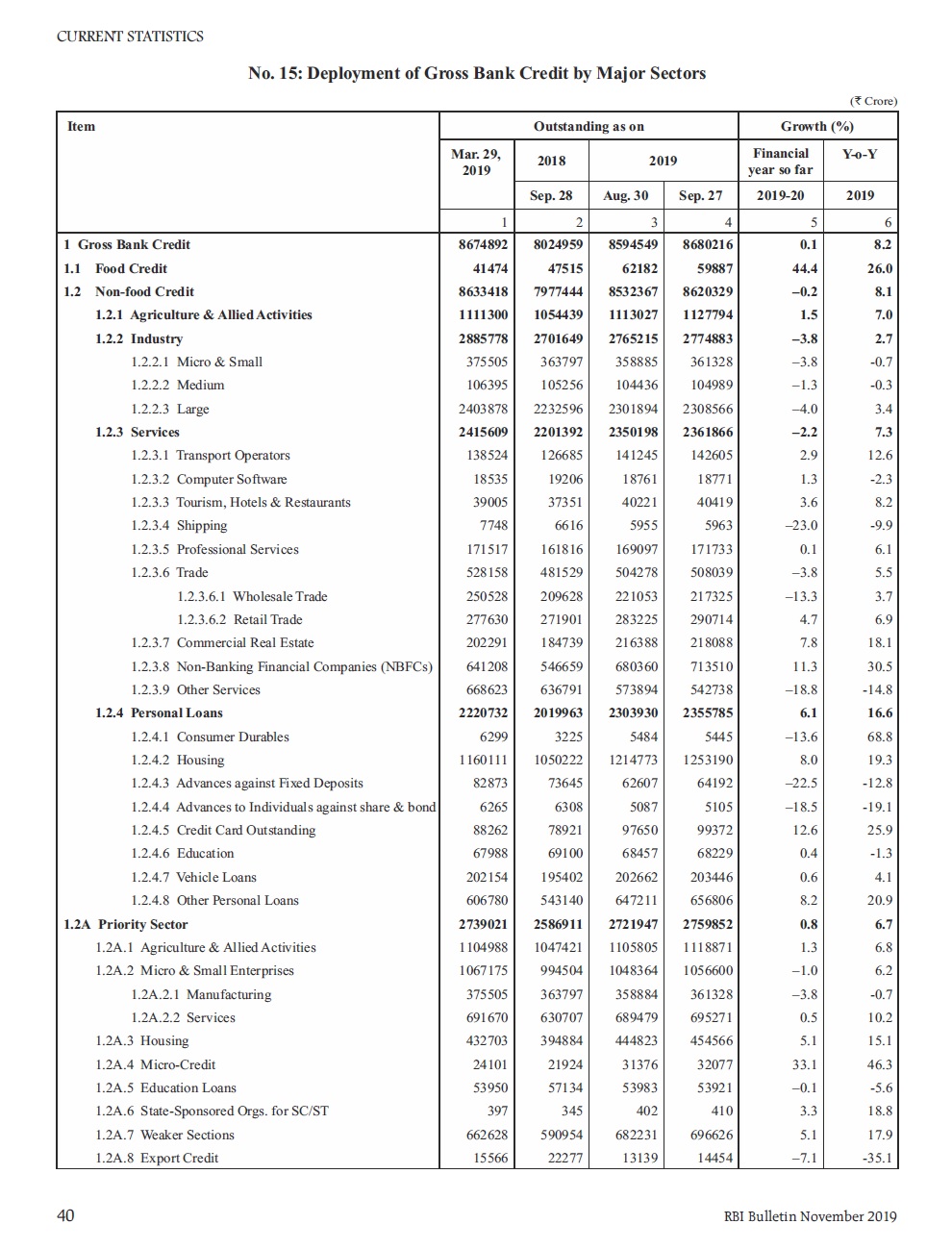

<p style="text-align:justify">Just before Dhanteras and Diwali this year, the Reserve Bank of India (RBI) released the <a href="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf" title="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf">November edition of its monthly bulletin</a>. The <a href="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf" title="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf">latest RBI Monthly Bulletin</a> says that the GDP has contracted by -8.6 percent in the second quarter of fiscal year 2020-21 <em>(i.e. July-September, 2020)</em> as compared to the gross domestic product (GDP) during the corresponding period last year. It may be noted that India’s GDP shrunk by -23.9 percent in the first quarter of the current fiscal year. According to the <a href="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf" title="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf">RBI Monthly Bulletin of November</a>, the country “has entered a technical recession in the first half of 2020-21 for the first time in its history with Q2:2020-21 likely to record the second successive quarter of GDP contraction.”</p><p style="text-align:justify">In the chapter "State of the Economy" of the <a href="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf" title="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf">RBI Monthly Bulletin of November</a>, it has been mentioned that "[i]ncoming data for the month of October 2020 have brightened prospects and stirred up consumer and business confidence. With the momentum of September having been sustained, there is optimism that the revival of economic activity is stronger than the mere satiation of pent-up demand released by unlocks and the rebuilding of inventories. If this upturn is sustained in the ensuing two months, there is a strong likelihood that the Indian economy will break out of contraction of the six months gone by and return to positive growth in Q3:2020-21, ahead by a quarter of the forecast provided in the resolution of the monetary policy committee on October 9, 2020." </p><p style="text-align:justify">Against the backdrop of COVID-19 pandemic when joblessness amidst the regular/ salaried individuals is high and incomes are low, it is difficult to predict whether people will splurge during the festive season. Traditionally, Indians spend more on buying personal/ commercial vehicles, residential/ commercial properties, gold/ silver, consumer durables, kitchenware and holidaying, among others, during the festive months.</p><p style="text-align:justify"><strong>Personal loans</strong></p><p style="text-align:justify">Latest data available from the <a href="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf" title="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf">RBI Bulletin</a> <em>(released in November)</em> indicates that in the <a href="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202020%281%29.jpg" title="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202020%281%29.jpg">fortnight ended 25th September, 2020</a> <em>(i.e. between 27th September, 2019 and 25th September, 2020)</em>, the year-on-year (y-o-y) growth in outstanding credit to the housing sector was 8.5 percent. However, in the <a href="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202019.jpg" title="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202019.jpg">fortnight ended 27th September, 2019</a> <em>(i.e. between 28th September, 2018 and 27 September, 2019), </em>outstanding credit to the housing sector had y-o-y grown by 19.3 percent. There are reasons behind the slowing down in growth for house loans, which we will discuss in the next section. Kindly check chart-1.</p><p style="text-align:justify"><img alt="" src="/upload/images/Chart%201%20Growth%20in%20bank%20credit%20by%20various%20types%20of%20personal%20loans%20in%20September%202020%20and%20September%202019%281%29.jpg" style="height:871px; width:925px" /></p><p style="text-align:justify"><em><strong>Source: </strong><a href="/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf" title="/upload/files/RBI%20Bulletin%20November%202020%282%29.pdf">RBI Monthly Bulletin November 2020</a> and <a href="/upload/files/RBI%20Bulletin%20November%202019%282%29.pdf" title="/upload/files/RBI%20Bulletin%20November%202019%282%29.pdf">RBI Monthly Bulletin November 2019</a></em><br /><em><strong>---</strong></em></p><p style="text-align:justify">As opposed to personal loans for housing, a different trend in case of vehicle loans is noticed. In <a href="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202020%282%29.jpg" title="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202020%282%29.jpg">the fortnight ended 25th September, 2020</a>, the y-o-y growth in outstanding credit to vehicle loans was found to be 8.8 percent, whereas in the <a href="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202019%281%29.jpg" title="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202019%281%29.jpg">fortnight ended 27th September, 2019,</a> the y-o-y growth rate in vehicle credit was at a much lower level i.e. 4.1 percent. This may have happened because the pandemic has forced people to travel in their own vehicles <em>(for reasons like safety and physical distancing) </em>instead of relying on public transport. Unavailability of public transport during the time of phase-wise unlocking of the economy may have compelled many consumers to purchase their own vehicles backed by bank loans.</p><p style="text-align:justify">Growth in personal loans <em>(on y-o-y basis) </em>for consumer durables and credit card outstanding have exhibited a declining trend in the <a href="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202020%283%29.jpg" title="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202020%283%29.jpg">fortnight ended 25th September, 2020</a> vis-à-vis the <a href="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202019%282%29.jpg" title="/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202019%282%29.jpg">fortnight ended 27th September, 2019</a>.</p><p style="text-align:justify">In the <a href="https://www.im4change.org/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202020%283%29.jpg" title="https://www.im4change.org/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202020%283%29.jpg">fortnight ended 25th September, 2020</a>, gross personal loans grew y-o-y by just 9.2 percent. However, in the <a href="https://www.im4change.org/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202019%282%29.jpg" title="https://www.im4change.org/upload/files/Deployment%20of%20Gross%20Bank%20Credit%20by%20Major%20Sectors%20November%202019%282%29.jpg">fortnight ended 27th September, 2019</a>, the y-o-y growth rate in total personal loans was at a much higher level i.e. 16.6 percent. Please consult chart-1.</p><p style="text-align:justify">In her <a href="/upload/files/Presentation%20on%20Atmanirbhar%20Bharat%20Package%203.0%20dated%2012%20November%202020%281%29.pdf" title="/upload/files/Presentation%20on%20Atmanirbhar%20Bharat%20Package%203.0%20dated%2012%20November%202020%281%29.pdf">presentation on Atmanirbhar Bharat Package 3.0</a> on 12th November, 2020, Finance Minister Smt. Nirmala Sitharaman has stated that "RBI predicts a strong likelihood of Indian economy returning to positive growth in Q3:2020-21, ahead by a quarter of the earlier forecast." She also added that "[p]rominent economists have suggested that the rebound is not only due to pent up demand, but also strong economic growth."</p><p style="text-align:justify">Latest data available from the Weekly Statistical Supplement - Extract <em>(URL is <a href="https://rbi.org.in/Scripts/BS_viewWssExtract.aspx" title="https://rbi.org.in/Scripts/BS_viewWssExtract.aspx">https://rbi.org.in/Scripts/BS_viewWssExtract.aspx</a>)</em> of the RBI, however, shows that the growth in non-food credit <em>(of which, personal loans is a part) </em>fell to 5.15 percent y-o-y during the fortnight ended October 23rd, 2020 from 5.68 percent growth seen in the previous fortnight. Most <a href="https://www.financialexpress.com/economy/non-food-credit-growth-slips-to-5-15-during-fortnight-ended-october-23/2124798/" title="https://www.financialexpress.com/economy/non-food-credit-growth-slips-to-5-15-during-fortnight-ended-october-23/2124798/">Indian banks are hopeful</a> about a rise in credit offtake <a href="https://www.financialexpress.com/economy/non-food-credit-growth-slips-to-5-15-during-fortnight-ended-october-23/2124798/" title="https://www.financialexpress.com/economy/non-food-credit-growth-slips-to-5-15-during-fortnight-ended-october-23/2124798/">in the second half of fiscal year</a> 2020-21.</p><p style="text-align:justify">The Weekly Statistical Supplement - Extract <em>(available at <a href="https://rbi.org.in/Scripts/BS_viewWssExtract.aspx" title="https://rbi.org.in/Scripts/BS_viewWssExtract.aspx">https://rbi.org.in/Scripts/BS_viewWssExtract.aspx</a>)</em> of the RBI indicates that in the <a href="https://www.im4change.org/upload/files/Fortnight%20ended%2023rd%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf" title="https://www.im4change.org/upload/files/Fortnight%20ended%2023rd%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf">fortnight ended 23rd October, 2020</a>, aggregate deposits grew y-o-y by <a href="/upload/files/Fortnight%20ended%2023rd%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf" title="/upload/files/Fortnight%20ended%2023rd%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf">10.1 percent</a>. In the <a href="https://www.im4change.org/upload/files/Fortnight%20ended%209th%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf" title="https://www.im4change.org/upload/files/Fortnight%20ended%209th%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf">fortnight ended 9th October, 2020</a>, the y-o-y growth rate in aggregate deposits was <a href="/upload/files/Fortnight%20ended%209th%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf" title="/upload/files/Fortnight%20ended%209th%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf">10.5 percent</a>.</p><p style="text-align:justify">Based on the data provided by the Weekly Statistical Supplement – Extract, the Inclusive Media for Change team has calculated that the credit-to-deposit (CD) ratio of the banking system, or the proportion of deposits deployed as loans, was <a href="https://www.im4change.org/upload/files/Fortnight%20ended%209th%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf" title="https://www.im4change.org/upload/files/Fortnight%20ended%209th%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf">72.32 percent</a> in the <a href="https://www.im4change.org/upload/files/Fortnight%20ended%209th%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf" title="https://www.im4change.org/upload/files/Fortnight%20ended%209th%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf">fortnight ended 9th October, 2020</a> and <a href="https://www.im4change.org/upload/files/Fortnight%20ended%2023rd%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf" title="https://www.im4change.org/upload/files/Fortnight%20ended%2023rd%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf">72.34 percent</a> in the <a href="https://www.im4change.org/upload/files/Fortnight%20ended%2023rd%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf" title="https://www.im4change.org/upload/files/Fortnight%20ended%2023rd%20October%202020%20Bulletin%20Weekly%20Statistical%20Supplement.pdf">fortnight ended 23rd October, 2020</a>.</p><p style="text-align:justify">In the meanwhile, we will have to wait to get the personal loans data and trends during the festive season, particularly in and around Dhanteras.</p><p style="text-align:justify">In the following two sections, we will discuss the broad trends in housing prices and registration of vehicles in the country.</p><p style="text-align:justify"><strong>Housing prices</strong></p><p style="text-align:justify">Against the backdrop of pandemic and economic recession, many financial consultants would have asked their clients to invest in real estate. This is because payment of rents has become a financial burden for many consumers due to falling incomes and a rise in joblessness. Besides, one could have availed the EMI moratorium of the RBI, thus making home loans a preferred option in comparison to paying rents in India. Nevertheless, a rational consumer has to keep in mind that <a href="https://www.financialexpress.com/money/why-youll-never-go-wrong-with-real-estate-investment/2114640/" title="https://www.financialexpress.com/money/why-youll-never-go-wrong-with-real-estate-investment/2114640/">not all properties in all the locations</a> would <a href="https://www.financialexpress.com/money/why-youll-never-go-wrong-with-real-estate-investment/2114640/" title="https://www.financialexpress.com/money/why-youll-never-go-wrong-with-real-estate-investment/2114640/">fetch similar returns</a> on the investment made.</p><p style="text-align:justify">A person who is buying a residential property has to also keep in mind that <a href="https://www.livemint.com/money/personal-finance/how-much-does-a-house-cost-in-hyderabad-11597312816838.html" title="https://www.livemint.com/money/personal-finance/how-much-does-a-house-cost-in-hyderabad-11597312816838.html">its price depends on several factors</a>, including location <em>(proximity to facilities like schools, hospitals, workplaces and markets, distance from public transport, quality of roads, etc.)</em>, neighbourhood and safety, quality of construction, amenities <em>(like electricity, water supply, house cleaning services, etc.)</em> and age of building, among other things.</p><p style="text-align:justify"><em>RBI’s House Price Index</em></p><p style="text-align:justify">The housing sector of the country suffers from large inventory overhang, tapering of incomes and hence, EMI-servicing capacity, and high stress in the balance sheets of non-banking finance companies (NBFCs) and housing finance companies (HFCs), according to the <a href="/upload/files/RBI%20Bulletin%20October%202020%281%29.pdf" title="/upload/files/RBI%20Bulletin%20October%202020%281%29.pdf">RBI Monthly Bulletin of October</a> this year. Both sales and new launches pertaining to residential real estate contracted in the first quarter of the current fiscal year, mainly on account of the lockdown and sluggish consumer sentiment, leading to rise in inventory overhang <em>(see chart-2a)</em>.</p><p style="text-align:justify"><strong>Chart 2: Housing Sector - Launches, Sales and Prices</strong></p><p style="text-align:justify"><img alt="" src="/upload/images/Chart%202%20Housing%20Sector%20-%20Launches%2C%20Sales%20and%20Prices.jpg" style="height:372px; width:956px" /></p><p style="text-align:justify"><em><strong>Source: </strong><a href="/upload/files/RBI%20Bulletin%20October%202020%282%29.pdf" title="/upload/files/RBI%20Bulletin%20October%202020%282%29.pdf">RBI Bulletin October 2020</a></em><br /><em><strong>---</strong></em></p><p style="text-align:justify">The national-level housing price index of RBI decelerated during the first quarter of fiscal year 2020-21. In her <a href="https://www.im4change.org/upload/files/Presentation%20on%20Atmanirbhar%20Bharat%20Package%203.0%20dated%2012%20November%202020%281%29.pdf" title="https://www.im4change.org/upload/files/Presentation%20on%20Atmanirbhar%20Bharat%20Package%203.0%20dated%2012%20November%202020%281%29.pdf">presentation on Atmanirbhar Bharat Package 3.0</a> on 12th November, 2020, the Finance Minister has acknowledged that "economic slowdown has led to decline in prices of residential unit."</p><p style="text-align:justify">Although the sub-indices for Bengaluru registered a substantial growth, the same for Delhi contracted substantially from the previous quarter. Please consult chart-2b.</p><p style="text-align:justify"><br /><strong>Table 1: RBI’s House Price Index in 10 cities and all-India level (Base year: 2010-11 = 100)</strong></p><p style="text-align:justify"><img alt="" src="/upload/images/Table%201%20RBIs%20House%20Price%20Index%20in%2010%20cities%20and%20all-India%20level.jpg" style="height:641px; width:1000px" /></p><p style="text-align:justify"><em><strong>Source: </strong>RBI's Database of Indian Economy (DBIE) portal, </em><a href="https://dbie.rbi.org.in/DBIE/dbie.rbi?site=statistics" title="https://dbie.rbi.org.in/DBIE/dbie.rbi?site=statistics">https://dbie.rbi.org.in/DBIE/dbie.rbi?site=statistics</a></p><p style="text-align:justify"><em><strong>Note: </strong>*Chennai index is based on both residential and commercial properties.</em></p><p style="text-align:justify"><em>All India index is a weighted average of city indices, weights based on population proportion.</em></p><p style="text-align:justify"><em>**(P) Provisional indexes which will be finalized by next quarter.</em></p><p style="text-align:justify"><em>Kindly <a href="https://docs.google.com/spreadsheets/d/1qqmr2PCviB5_ALZ0wUqxSMKw8J0NKte25A2bCdHTMCw/edit?usp=sharing" title="https://docs.google.com/spreadsheets/d/1qqmr2PCviB5_ALZ0wUqxSMKw8J0NKte25A2bCdHTMCw/edit?usp=sharing">click here</a> to access the HPI data in spreadsheet</em><br /><em><strong>---</strong></em></p><p style="text-align:justify"><span style="background-color:#ffff00">Between 2010-11 (Q1) and 2020-21 (Q1), the average y-o-y growth of RBI's House Price Index for the cities of Delhi </span><em><span style="background-color:#ffff00">(14.7 percent)</span></em><span style="background-color:#ffff00">, Bangalore </span><em><span style="background-color:#ffff00">(12.3 percent)</span></em><span style="background-color:#ffff00">, Lucknow </span><em><span style="background-color:#ffff00">(16.2 percent)</span></em><span style="background-color:#ffff00">, Kolkata </span><em><span style="background-color:#ffff00">(12.5 percent)</span></em><span style="background-color:#ffff00">, Chennai </span><em><span style="background-color:#ffff00">(12.0 percent)</span></em><span style="background-color:#ffff00"> and Kochi </span><em><span style="background-color:#ffff00">(12.8 percent) </span></em><span style="background-color:#ffff00">exceeded the average y-o-y growth of HPI prevailing at the national-level </span><em><span style="background-color:#ffff00">(11.9 percent)</span></em><span style="background-color:#ffff00">.</span> Please check table-1.</p><p style="text-align:justify"><span style="background-color:#ffff00">Between 2018-19 (Q1) and 2020-21 (Q1), the average y-o-y growth of RBI's HPI for Mumbai was 1.5 percent, Delhi was -0.9 percent, Bangalore was 10.7 percent, Ahmedabad was 4.9 percent, Lucknow was 4.8 percent, Kolkata was 3.4 percent, Chennai was 11.2 percent, Jaipur was 8.6 percent, Kanpur was 7.7 percent, Kochi was 10.5 percent and for India was 4.0 percent.</span> Kindly consult table-1 for details.</p><p style="text-align:justify">The <a href="/upload/files/BUL10102014_FL.pdf" title="/upload/files/BUL10102014_FL.pdf">RBI Monthly Bulletin of October 2014</a> carries a <a href="/upload/files/HPI%20methodology%20RBI%20Monthly%20Bulletin%20October%202014%281%29.pdf" title="/upload/files/HPI%20methodology%20RBI%20Monthly%20Bulletin%20October%202014%281%29.pdf">chapter on the methodology to calculate HPI</a>. Beginning with Mumbai city, the RBI initiated the work of compiling a HPI in 2007 and brought out a quarterly HPI for Mumbai city <em>(base: 2002-03=100)</em>. Over the quarters, the coverage has been extended by incorporating 9 more major cities, viz., Delhi, Chennai, Kolkata, Bengaluru, Lucknow, Ahmedabad, Jaipur Kanpur and Kochi and the base is shifted to 2010-11=100. Besides separate HPI for individual cities, an average HPI representing all-India house price movement is also compiled.</p><p style="text-align:justify">Kindly note that the aggregate HPI is a weighted average price index using Laspeyres’ method with 2010-11 as the base year. First, the simple average of price (per square meter) of houses in each category, classified by small, medium and large for each ward/ administrative zone in each quarter based on floor space area (FSA) is calculated. Second, the proportion of number of houses transacted in the three categories of FSA within a ward/zone during the period April 2010 – March 2011 is taken as the weights. Then, based on an average per square meter price for three FSA category houses in each ward/ zone, price-relatives are calculated for each quarter. The price relative is nothing but a ratio of current period price to the base period price. The quarterly ward/ zone weighted average price relatives are calculated next. These weighted relative prices are again averaged, using the proportion of number of houses transacted in each ward to the total number of houses transacted in the city during the period April 2010 – March 2011 as the weights. The city-wise price indices are averaged using the population proportion <em>(based on 2011 census)</em> of the ten cities to its total to obtain the all-India index.</p><p style="text-align:justify"><em>Real residential property prices of BIS</em></p><p style="text-align:justify">The index of real residential property prices <em>(CPI-deflated; Index, 2010 = 100) </em>has been developed by the Bank for International Settlements <em>(available at <a href="https://stats.bis.org/statx/srs/table/h2" title="https://stats.bis.org/statx/srs/table/h2">https://stats.bis.org/statx/srs/table/h2</a>)</em>.</p><p style="text-align:justify"><strong>Table 2: Index of real residential property prices (CPI-deflated; Index, 2010 = 100)</strong></p><p style="text-align:justify"><img alt="" src="/upload/images/Table%202%20Index%20of%20real%20residential%20property%20prices.jpg" style="height:209px; width:896px" /></p><p style="text-align:justify"><em><strong>Source: </strong>Bank for International Settlements, available at <a href="https://stats.bis.org/statx/srs/table/h2" title="https://stats.bis.org/statx/srs/table/h2">https://stats.bis.org/statx/srs/table/h2</a></em></p><p style="text-align:justify"><strong><em>---</em></strong></p><p style="text-align:justify">For India the index has dipped in the first quarter of 2020 <em>(i.e. 171.1) </em>in comparison to not only the last quarter of 2019 <em>(i.e. 172.2)</em>, but also the first quarter of 2019 <em>(i.e. 175.7)</em>. A similar trend has been noticed for China. However, for the United States and for the United Kingdom, one finds that the pessimism arising out of global economic slowdown did not affect the index in the first quarter of 2020. Please see table-2.</p><p style="text-align:justify">For India, it can also be observed that the index has been going down since 2019.</p><p style="text-align:justify"><em>Atmanirbhar Bharat Package 3.0 for housing</em></p><p style="text-align:justify">It should be noted by the readers that under the <a href="/upload/files/Presentation%20on%20Atmanirbhar%20Bharat%20Package%203.0%20dated%2012%20November%202020%282%29.pdf" title="/upload/files/Presentation%20on%20Atmanirbhar%20Bharat%20Package%203.0%20dated%2012%20November%202020%282%29.pdf">Atmanirbhar Bharat Package 3.0</a>, announced on 12th November, 2020, first-time purchasers of residential houses/ flats costing up to Rs. 2 crore will get income tax relief of up to 20 percent <em>(under section 56(2)(x) of Income Tax Act) </em>and this will be available till June 30, 2021. Apart from that, the differential between circle rate <em>(stamp duty value) </em>and agreement value <em>(purchase value) </em>for primary sale of residential units of up to Rs. 2 crore, has been doubled from 10 percent to 20 percent <em>(under section 43CA of Income Tax Act) </em>till June 30th next year. The <a href="https://www.ndtv.com/business/nirmala-sitharaman-announces-income-tax-relief-for-developers-and-home-buyers-to-boost-demand-for-residential-real-estate-2324290" title="https://www.ndtv.com/business/nirmala-sitharaman-announces-income-tax-relief-for-developers-and-home-buyers-to-boost-demand-for-residential-real-estate-2324290">tax relief</a>, which has been provided to the <a href="https://www.ndtv.com/business/nirmala-sitharaman-announces-income-tax-relief-for-developers-and-home-buyers-to-boost-demand-for-residential-real-estate-2324290" title="https://www.ndtv.com/business/nirmala-sitharaman-announces-income-tax-relief-for-developers-and-home-buyers-to-boost-demand-for-residential-real-estate-2324290">middle class as incentives</a>, is expected to <a href="https://www.ndtv.com/business/nirmala-sitharaman-announces-income-tax-relief-for-developers-and-home-buyers-to-boost-demand-for-residential-real-estate-2324290" title="https://www.ndtv.com/business/nirmala-sitharaman-announces-income-tax-relief-for-developers-and-home-buyers-to-boost-demand-for-residential-real-estate-2324290">boost demand for residential properties</a> and to <a href="https://www.ndtv.com/business/nirmala-sitharaman-announces-income-tax-relief-for-developers-and-home-buyers-to-boost-demand-for-residential-real-estate-2324290" title="https://www.ndtv.com/business/nirmala-sitharaman-announces-income-tax-relief-for-developers-and-home-buyers-to-boost-demand-for-residential-real-estate-2324290">clear the existing inventories</a>.</p><p style="text-align:justify">According to <a href="https://theprint.in/economy/tax-sop-to-homebuyers-is-unlikely-to-make-a-dent-in-metro-cities-due-to-caps/543274/" title="https://theprint.in/economy/tax-sop-to-homebuyers-is-unlikely-to-make-a-dent-in-metro-cities-due-to-caps/543274/">developers and property dealers</a>, although property prices in most metro cities have corrected in the midst of economic slowdown <em>(that has been happening since the last few years)</em>, the circle rates <em>(i.e. ready reckoner rates)</em> have gone up. The circle rates are not linked to actual prices. However, circle rates have been raised in the recent years by the states to increase their revenue despite a fall in prices. <a href="https://theprint.in/economy/tax-sop-to-homebuyers-is-unlikely-to-make-a-dent-in-metro-cities-due-to-caps/543274/" title="https://theprint.in/economy/tax-sop-to-homebuyers-is-unlikely-to-make-a-dent-in-metro-cities-due-to-caps/543274/">Most developers and property dealers</a> think that the recently announced relaxations by the government could have been extended for commercial real estate, besides property worth more than Rs. 2 crore. </p><p style="text-align:justify"><strong>Registration of vehicles</strong></p><p style="text-align:justify">The <a href="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%281%29.pdf" title="https://www.im4change.org/upload/files/RBI%20Bulletin%20November%202020%281%29.pdf">latest RBI Monthly Bulletin</a> has mentioned that "[c]ar manufacturing majors are reporting double digit growth in response to festival demand and restocking as well as shift in preferences towards owned vehicles over public transportation. The ebullience is not, however, shared by dealerships. According to the Federation of Automobile Dealers Associations (FADA), sales of two-wheelers and passenger vehicles declined by 27 percent and 9 percent, respectively, in October 2020. The decline was sharper in the case of commercial vehicles and three-wheelers, which registered a contraction of 30 percent and 65 percent, respectively."</p><p style="text-align:justify">The total number of vehicles registered in the country was 1.92 crore in 2016, 2.09 crore in 2017 <em>(8.63 percent growth over previous year)</em>, 2.27 crore in 2018 <em>(8.87 percent growth over previous year)</em>, 2.15 crore in 2019 <em>(-5.52 percent growth over previous year)</em> and 1.34 crore in 2020 <em>(as on 16th November, 2020)</em>.</p><p style="text-align:justify"><strong>Table 3: Monthwise number of vehicles registered (in lakhs) in India and their y-o-y growth (in %)</strong></p><p style="text-align:justify"><img alt="" src="/upload/images/Table%203%20Monthwise%20number%20of%20vehicles%20registered%20in%20lakhs%20and%20their%20y-o-y%20growth.jpg" style="height:354px; width:626px" /></p><p style="text-align:justify"><em><strong>Source: </strong>Vahan dashboard of Parivahan Sewa portal of MoRTH, </em><a href="https://vahan.parivahan.gov.in/vahan4dashboard/" title="https://vahan.parivahan.gov.in/vahan4dashboard/">https://vahan.parivahan.gov.in/vahan4dashboard/</a><em>, accessed on 16th November, 2020</em></p><p style="text-align:justify"><strong><em>---</em></strong></p><p style="text-align:justify">In order to understand the gravity of the problem experienced by the automobile sector, it is important to look at the recent figures related to registration of vehicles. Latest data available from the Parivahan Sewa portal <em>(<a href="https://vahan.parivahan.gov.in/vahan4dashboard/" title="https://vahan.parivahan.gov.in/vahan4dashboard/">https://vahan.parivahan.gov.in/vahan4dashboard/</a>)</em> of the Ministry of Road Transport & Highways (MoRTH) indicates that in 2019, the y-o-y growth in vehicle registration was negative in most months with the exception of January, October and November. In 2020, although the y-o-y growth in vehicle registration became positive in February and March, since the imposition of lockdown <em>(and subsequently unlockdown)</em> the y-o-y growth in vehicle registration has remained in negative territory. Please see table-3.</p><p style="text-align:justify"><span style="background-color:#ffff00">Despite a far greater decline in vehicle registration in 2020 as compared to 2019 <em>(as stated earlier in this section)</em>, we have witnessed a rising trend for growth in vehicle loans in the fortnight ended 25th September, 2020 vis-à-vis the fortnight ended 27th September, 2019 </span><em><span style="background-color:#ffff00">(please consult chart-1)</span></em><span style="background-color:#ffff00">. This contradiction needs to be explained by the official economists.</span></p><p style="text-align:justify"><strong><em>References</em></strong></p><p style="text-align:justify">RBI Monthly Bulletin November 2020, please <a href="/upload/files/RBI%20Bulletin%20November%202020%281%29.pdf" title="/upload/files/RBI%20Bulletin%20November%202020%281%29.pdf">click here</a> to read more</p><p style="text-align:justify">RBI Monthly Bulletin October 2020, please <a href="/upload/files/RBI%20Bulletin%20October%202020.pdf" title="/upload/files/RBI%20Bulletin%20October%202020.pdf">click here</a> to read more</p><p style="text-align:justify">RBI Monthly Bulletin November 2019, please <a href="/upload/files/RBI%20Bulletin%20November%202019%281%29.pdf" title="/upload/files/RBI%20Bulletin%20November%202019%281%29.pdf">click here</a> to read more</p><p style="text-align:justify">Methodology on House Price Index, RBI Monthly Bulletin October 2014, please <a href="/upload/files/HPI%20methodology%20RBI%20Monthly%20Bulletin%20October%202014.pdf" title="/upload/files/HPI%20methodology%20RBI%20Monthly%20Bulletin%20October%202014.pdf">click here</a> to read more</p><p style="text-align:justify">Residential property prices: selected series (nominal and real), Bank for International Settlements, please <a href="https://www.bis.org/statistics/pp_selected.htm?m=6%7C288%7C596" title="https://www.bis.org/statistics/pp_selected.htm?m=6%7C288%7C596">click here</a> to access</p><p style="text-align:justify">Press release: Income Tax relief for Real-estate Developers and Home Buyers, Press Information Bureau, Ministry of Finance, 13 November, 2020, please <a href="/upload/files/PIB%20release%20Income%20Tax%20relief%20for%20Real-estate%20Developers%20and%20Home%20Buyers%2013%20Nov%202020.pdf" title="/upload/files/PIB%20release%20Income%20Tax%20relief%20for%20Real-estate%20Developers%20and%20Home%20Buyers%2013%20Nov%202020.pdf">click here</a> to access</p><p style="text-align:justify">Presentation on Atmanirbhar Bharat Package 3.0 dated 12 November 2020, Ministry of Finance, please <a href="/upload/files/Presentation%20on%20Atmanirbhar%20Bharat%20Package%203.0%20dated%2012%20November%202020.pdf" title="/upload/files/Presentation%20on%20Atmanirbhar%20Bharat%20Package%203.0%20dated%2012%20November%202020.pdf">click here</a> to read more</p><p style="text-align:justify">News alert: Declining bank credit indicates poor economic performance, Published on July 10, 2017, Inclusive Media for Change, please <a href="https://www.im4change.org/news-alerts-57/declining-bank-credit-indicates-poor-economic-performance-4682277.html" title="https://www.im4change.org/news-alerts-57/declining-bank-credit-indicates-poor-economic-performance-4682277.html">click here</a> to read more</p><p style="text-align:justify">The Hindu Explains: What is technical recession, and what does it mean for the Indian economy? -Suresh Seshadri, The Hindu, 15 November, 2020, please <a href="https://www.im4change.org/latest-news-updates/the-hindu-explains-what-is-technical-recession-and-what-does-it-mean-for-the-indian-economy-suresh-seshadri.html" title="https://www.im4change.org/latest-news-updates/the-hindu-explains-what-is-technical-recession-and-what-does-it-mean-for-the-indian-economy-suresh-seshadri.html">click here</a> to read more</p><p style="text-align:justify">Explained: What is a technical recession? -Udit Misra, The Indian Express, 13 November, 2020, please <a href="https://www.im4change.org/latest-news-updates/explained-what-is-a-technical-recession-udit-misra.html" title="https://www.im4change.org/latest-news-updates/explained-what-is-a-technical-recession-udit-misra.html">click here</a> to read more</p><p style="text-align:justify">Realty tax sop is unlikely to make a dent in metro cities due to caps -Manojit Saha, ThePrint.in, 13 November, 2020, please <a href="https://theprint.in/economy/tax-sop-to-homebuyers-is-unlikely-to-make-a-dent-in-metro-cities-due-to-caps/543274/" title="https://theprint.in/economy/tax-sop-to-homebuyers-is-unlikely-to-make-a-dent-in-metro-cities-due-to-caps/543274/">click here</a> to read more</p><p style="text-align:justify">Income Tax Relief For Developers, Home-Buyers To Boost Real Estate Demand, NDTV, 12 November, 2020, please <a href="https://www.ndtv.com/business/nirmala-sitharaman-announces-income-tax-relief-for-developers-and-home-buyers-to-boost-demand-for-residential-real-estate-2324290" title="https://www.ndtv.com/business/nirmala-sitharaman-announces-income-tax-relief-for-developers-and-home-buyers-to-boost-demand-for-residential-real-estate-2324290">click here</a> to read more</p><p style="text-align:justify">Non-food credit growth slips to 5.15% during fortnight ended October 23, Financial Express, 10 November, 2020, please <a href="https://www.financialexpress.com/economy/non-food-credit-growth-slips-to-5-15-during-fortnight-ended-october-23/2124798/" title="https://www.financialexpress.com/economy/non-food-credit-growth-slips-to-5-15-during-fortnight-ended-october-23/2124798/">click here</a> to read more</p><p style="text-align:justify">Why you’ll never go wrong with real estate investment, Financial Express, 27 October, 2020, please <a href="https://www.financialexpress.com/money/why-youll-never-go-wrong-with-real-estate-investment/2114640/" title="https://www.financialexpress.com/money/why-youll-never-go-wrong-with-real-estate-investment/2114640/">click here</a> to read more</p><p style="text-align:justify">How much does a house cost in Hyderabad? Livemint.com, 13 August, 2020, please <a href="https://www.livemint.com/money/personal-finance/how-much-does-a-house-cost-in-hyderabad-11597312816838.html" title="https://www.livemint.com/money/personal-finance/how-much-does-a-house-cost-in-hyderabad-11597312816838.html">click here</a> to read more</p><p style="text-align:justify"> </p><p style="text-align:justify"><strong>Image Courtesy: Inclusive Media for Change/ Himanshu Joshi</strong></p>

</div>

</td>

</tr>

</table>

</div>

</div>

</div>

<div class="clear"></div>

<div style="padding-top: 18px;">

<p class="post-tag">Tagged with:

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Atmanirbhar Bharat"

title="Atmanirbhar Bharat">

Atmanirbhar Bharat </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Atmanirbhar Bharat Package 3.0"

title="Atmanirbhar Bharat Package 3.0">

Atmanirbhar Bharat Package 3.0 </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Bank for International Settlements"

title="Bank for International Settlements">

Bank for International Settlements </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=BIS"

title="BIS">

BIS </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Dhanteras"

title="Dhanteras">

Dhanteras </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=House Price Index"

title="House Price Index">

House Price Index </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Housing Loans"

title="Housing Loans">

Housing Loans </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Housing Prices"

title="Housing Prices">

Housing Prices </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Ministry of Road Transport & Highways"

title="Ministry of Road Transport & Highways">

Ministry of Road Transport & Highways </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Parivahan Sewa"

title="Parivahan Sewa">

Parivahan Sewa </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Personal Loans"

title="Personal Loans">

Personal Loans </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=RBI"

title="RBI">

RBI </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=RBI Monthly Bulletin"

title="RBI Monthly Bulletin">

RBI Monthly Bulletin </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Real Residential Property Prices"

title="Real Residential Property Prices">

Real Residential Property Prices </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Reserve Bank of India"

title="Reserve Bank of India">

Reserve Bank of India </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Vehicle Loans"

title="Vehicle Loans">

Vehicle Loans </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Ministry of Road Transport & Highways"

title="Ministry of Road Transport & Highways">

Ministry of Road Transport & Highways </a>

</p>

</div>

<div class="clear"></div>

<br><br>

<div class="widget-top">

<h4>Related Articles</h4>

<div class="stripe-line"></div>

</div>

<div class="widget-container">

<ul id="recentcomments">

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/milk-prices-to-remain-firm-this-summer-rbi-governor-economic-times.html"

title="Milk Prices to Remain Firm this Summer, RBI Governor - Economic Times">

Milk Prices to Remain Firm this Summer, RBI Governor - Economic Times </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/government-sells-rs-900-crore-of-wheat-to-counter-food-price-spike-ravi-dutta-mishra.html"

title="Government sells Rs. 900 crore of wheat to counter food price spike - Ravi Dutta Mishra">

Government sells Rs. 900 crore of wheat to counter food price spike - Ravi Dutta Mishra </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/can-india-s-production-incentive-scheme-transform-the-economy-as-the-sez-push-did-for-china-siddhant-bajpai.html"

title="Can India’s production incentive scheme transform the economy as the SEZ push did for China? -Siddhant Bajpai">

Can India’s production incentive scheme transform the economy as the SEZ push did for China? -Siddhant Bajpai </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/demonetisation-not-bad-in-law-says-supreme-court-in-4-1-verdict.html"

title="Demonetisation: Not bad in law, says Supreme Court in 4:1 verdict">

Demonetisation: Not bad in law, says Supreme Court in 4:1 verdict </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/credit-growth-spurs-public-lenders-balance-sheets-to-10-year-high-in-first-half-of-fy23-rbi-report.html"

title="Credit growth spurs public lenders’ balance sheets to 10-year high in first half of FY23: RBI report">

Credit growth spurs public lenders’ balance sheets to 10-year high in first half of FY23: RBI report </a>

</li>

</ul>

</div>

<div class="comment-respond" id="respond">

<a name="commentbox"> </a>

<h3 class="comment-reply-title" id="reply-title">Write Comments</h3>

<form method="post" accept-charset="utf-8" role="form" action="/news-alerts-57/has-personal-loans-seen-a-rebound-ahead-of-the-festive-season-the-answer-is-in-the-negative.html"><div style="display:none;"><input type="hidden" name="_method" value="POST"/></div> <form class="comment-form" id="commentform" method="post" action="#commentbox" onSubmit="return validate()"

name="cmtform">

<input type="hidden" name="cmttype" value="articlecmt"/>

<input type="hidden" name="article_id" value="57611"/>

<p class="comment-notes">Your email address will not be published. Required fields are marked <span

class="required">*</span></p>

<p class="comment-form-author">

<label for="commenterName">Name</label>

<span class="required">*</span>

<input type="text" aria-required="true" size="30"

value=""

name="commenterName" id="commenterName" required="true">

</p>

<p class="comment-form-email">

<label for="commenterEmail">Email</label> <span class="required">*</span>

<input aria-required="true" size="30" name="commenterEmail" id="commenterEmail" type="email"

value=""

required="true">

</p>

<p class="comment-form-contact">

<label for="commenterPh">Contact No.</label>

<input type="text" size="30"

value=""

name="commenterPh" id="commenterPh">

</p>

<p class="comment-form-comment">

<label for="comment">Comment</label>

<textarea aria-required="true" required="true" rows="8" cols="45" name="comment"

id="comment"></textarea>

</p>

<p class="comment-form-comment">

<label for="comment">Type the characters you see in the image below <span class="required">*</span><br><img

class="captchaImg"

src="https://im4change.in/securimage_show_art.php?tk=1162083253" alt="captcha"/>

</label>

</p>

<input type="text" name="vrcode" required="true"/>

<p class="form-submit" style="width: 200px;">

<input type="submit" value="Post Comment" id="submit" name="submit">

</p></form>

</div>

<style>

.ui-widget-content {

height: auto !important;

}

</style>

<div id="share-modal"></div>

<style>

.middleContent a{

background-color: rgba(108,172,228,.2);

}

.middleContent a:hover{

background-color: #418fde;

border-color: #418fde;

color: #000;

}

</style>

<script>

function shareArticle(article_id) {

var options = {

modal: true,

height: 'auto',

width: 600 + 'px'

};

$('#share-modal').html("");

$('#share-modal').load('https://im4change.in/share_article?article_id=' + article_id).dialog(options).dialog('open');

}

function postShare() {

var param = 'article_id=' + $("#article_id").val();

param = param + '&y_name=' + $("#y_name").val();

param = param + '&y_email=' + $("#y_email").val();

param = param + '&f_name=' + $("#f_name").val();

param = param + '&f_email=' + $("#f_email").val();

param = param + '&y_msg=' + $("#y_msg").val();

$.ajax({

type: "POST",

url: 'https://im4change.in/post_share_article',

data: param,

success: function (response) {

$('#share-modal').html("Thank You, Your message posted to ");

}

});

return false;

}

</script> </div>

</div>

<!-- Right Side Section Start -->

<!-- MAP Section START -->

<aside class="sidebar indexMarg">

<div class="ad-cell">

<a href="https://im4change.in/statemap.php" title="">

<img src="https://im4change.in/images/map_new_version.png?1582080666" alt="India State Map" class="indiamap" width="232" height="252"/> </a>

<div class="rightmapbox">

<div id="sideOne" class="docltitle"><a href="https://im4change.in/state-report/india/36" target="_blank">DOCUMENTS/

REPORTS</a></div>

<div id="sideTwo" class="statetitle"><a href="https://im4change.in/states.php"target="_blank">STATE DATA/

HDRs.</a></div>

</div>

<div class="widget widgePadTop"></div>

</div>

</aside>

<!-- MAP Section END -->

<aside class="sidebar sidePadbottom">

<div class="rightsmlbox1" >

<a href="https://im4change.in/knowledge_gateway" target="_blank" style="color: #035588;

font-size: 17px;">

KNOWLEDGE GATEWAY

</a>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title">

<a href="https://im4change.in/newsletter" target="_blank">

NEWSLETTER

</a>

</p>

</div>

</div>

<div class="rightsmlbox1" style="height: 325px;">

<div>

<p class="rightsmlbox1_title">

Interview with Prof. Ravi Srivastava

</p>

<p class="rightsmlbox1_title">

<a href="https://im4change.in/video/interview-with-prof-ravi-srivastava-on-current-economic-crisis">

<img width="250" height="200" src="/images/interview_video_home.jpg" alt="Interview with Prof. Ravi Srivastava"/>

</a>

<!--

<iframe width="250" height="200" src="https://www.youtube.com/embed/MmaTlntk-wc" frameborder="0" allow="accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture" allowfullscreen=""></iframe>-->

</p>

<a href="https://im4change.in/videogallery" class="more-link CatArchalAnch1" target="_blank">

More videos

</a>

</div>

</div>

<div class="rightsmlbox1">

<div>

<!--div id="sstory" class="rightboxicons"></div--->

<p class="rightsmlbox1_title"><a href="https://im4change.in/list-success-stories" target="_blank">Success Stories</a></p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a

href="https://im4change.in/interviews" target="_blank">Interviews</a>

</p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a href="https://www.commoncause.in/page.php?id=10" >Donate</a></p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a

href="https://im4change.in/marquee"

class="isf_link more-link" title="India Focus?" style="border: 4px solid #fdd922;width: 90%;background-color: #fdd922;text-align: center;color: #000000;font-size:18px" target="_blank">India Focus</a></p> </div>

</div>

<div class="rightsmlbox1" style="height: 104px !important;">

<a href="https://im4change.in/quarterly_reports.php" target="_blank">

Quarterly Reports on Effect of Economic Slowdown on Employment in India (2008 - 2015)

</a>

</div>

<!-- <div class="rightsmlbox1">

<a href="https://play.google.com/store/apps/details?id=com.im4.im4change" target="_blank">

</a></div> -->

<!-- <section class="cat-box recent-box secMarg">

<h2 class="cat-box-title">Most Visited</h2>

</section> -->

<!-- accordion Starts here -->

<!-- <div id="accordion" class="accordMarg">

</div> -->

<!-- accordion ends here -->

<!-- Widget Tag Cloud Starts here -->

<div id="tag_cloud-2" class="widget widget_tag_cloud">

<section class="cat-box recent-box secMarg">

<h2 class="cat-box-title">MOST VISITED TAGS</h2>

</section>

<div class="widget-top wiPdTp">

<div class="stripe-line"></div>

</div>

<div class="widget-container">

<div class="tagcloud">

<a href="https://im4change.in/search?qryStr=Agriculture"

target="_blank" class="tag-link-4 font4">Agriculture</a>

<a href="https://im4change.in/search?qryStr=Food Security"

target="_blank" class="tag-link-4 font4">Food Security</a>

<a href="https://im4change.in/search?qryStr=Law and Justice"

target="_blank" class="tag-link-4 font4">Law and Justice</a>

<a href="https://im4change.in/search?qryStr=Health"

target="_blank" class="tag-link-4 font4">Health</a>

<a href="https://im4change.in/search?qryStr=Right to Food"

target="_blank" class="tag-link-4 font4">Right to Food</a>

<a href="https://im4change.in/search?qryStr=Corruption"

target="_blank" class="tag-link-4 font4">Corruption</a>

<a href="https://im4change.in/search?qryStr=farming"

target="_blank" class="tag-link-4 font4">farming</a>

<a href="https://im4change.in/search?qryStr=Environment"

target="_blank" class="tag-link-4 font4">Environment</a>

<a href="https://im4change.in/search?qryStr=Right to Information"

target="_blank" class="tag-link-4 font4">Right to Information</a>

<a href="https://im4change.in/search?qryStr=NREGS"

target="_blank" class="tag-link-4 font4">NREGS</a>

<a href="https://im4change.in/search?qryStr=Human Rights"

target="_blank" class="tag-link-4 font4">Human Rights</a>

<a href="https://im4change.in/search?qryStr=Governance"

target="_blank" class="tag-link-4 font4">Governance</a>

<a href="https://im4change.in/search?qryStr=PDS"

target="_blank" class="tag-link-4 font4">PDS</a>

<a href="https://im4change.in/search?qryStr=COVID-19"

target="_blank" class="tag-link-4 font4">COVID-19</a>

<a href="https://im4change.in/search?qryStr=Land Acquisition"

target="_blank" class="tag-link-4 font4">Land Acquisition</a>

<a href="https://im4change.in/search?qryStr=mgnrega"

target="_blank" class="tag-link-4 font4">mgnrega</a>

<a href="https://im4change.in/search?qryStr=Farmers"

target="_blank" class="tag-link-4 font4">Farmers</a>

<a href="https://im4change.in/search?qryStr=transparency"

target="_blank" class="tag-link-4 font4">transparency</a>

<a href="https://im4change.in/search?qryStr=Gender"

target="_blank" class="tag-link-4 font4">Gender</a>

<a href="https://im4change.in/search?qryStr=Poverty"

target="_blank" class="tag-link-4 font4">Poverty</a>

<a href="https://im4change.in/search?qryStr=Farm Laws" target="_blank" class="tag-link-4 font4">Farm Laws

</a>

<a href="https://im4change.in/search?qryStr=Citizenship Amendment Act" target="_blank" class="tag-link-4 font4">Citizenship Amendment Act

</a>

<a href="https://im4change.in/search?qryStr=CAA NPR NRIC" target="_blank" class="tag-link-4 font4">CAA NPR NRIC

</a>

<a href="https://im4change.in/search?qryStr=Job Losses" target="_blank" class="tag-link-4 font4">Job Losses