Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 150

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::index() - APP/Controller/ArtileDetailController.php, line 150

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 97

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 151

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::index() - APP/Controller/ArtileDetailController.php, line 151

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 97

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Warning (512): Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853 [CORE/src/Http/ResponseEmitter.php, line 48]

if (Configure::read('debug')) {

trigger_error($message, E_USER_WARNING);

} else {

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html>

<!--[if lt IE 7 ]>

<html class="ie ie6" lang='en'> <![endif]-->

<!--[if IE 7 ]>

<html class="ie ie7" lang='en'> <![endif]-->

<!--[if IE 8 ]>

<html class="ie ie8" lang='en'> <![endif]-->

<!--[if (gte IE 9)|!(IE)]><!-->

<html lang='en'>

<!--<![endif]-->

<head><meta http-equiv="Content-Type" content="text/html; charset=utf-8">

<title>

LATEST NEWS UPDATES | Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi & Surabhi Agarwal </title>

<meta name="description" content="

-The Business Standard

Against NDA's 75 million target, UPA added 61 million in 2013-14

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank..."/>

<meta name="keywords" content="Below Poverty Line,Jan Dhan Yojana,Financial Inclusion,banking,Poverty"/>

<meta name="news_keywords" content="Below Poverty Line,Jan Dhan Yojana,Financial Inclusion,banking,Poverty">

<link rel="alternate" type="application/rss+xml" title="ROR" href="/ror.xml"/>

<link rel="alternate" type="application/rss+xml" title="RSS 2.0" href="/feeds/"/>

<link rel="stylesheet" href="/css/bootstrap.min.css?1697864993"/> <link rel="stylesheet" href="/css/style.css?v=1.1.2"/> <link rel="stylesheet" href="/css/style-inner.css?1577045210"/> <link rel="stylesheet" id="Oswald-css"

href="https://fonts.googleapis.com/css?family=Oswald%3Aregular%2C700&ver=3.8.1" type="text/css"

media="all">

<link rel="stylesheet" href="/css/jquery.modal.min.css?1578285302"/> <script src="/js/jquery-1.10.2.js?1575549704"></script> <script src="/js/jquery-migrate.min.js?1575549704"></script> <link rel="shortcut icon" href="/favicon.ico" title="Favicon">

<link rel="stylesheet" href="/css/jquery-ui.css?1580720609"/> <script src="/js/jquery-ui.js?1575549704"></script> <link rel="preload" as="style" href="https://www.im4change.org/css/custom.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery.modal.min.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery-ui.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/li-scroller.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<!-- <link rel="preload" as="style" href="https://www.im4change.org/css/style.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous"> -->

<link rel="preload" as="style" href="https://www.im4change.org/css/style-inner.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel='dns-prefetch' href="//im4change.org/css/custom.css" crossorigin >

<link rel="preload" as="script" href="https://www.im4change.org/js/bootstrap.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.li-scroller.1.0.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.modal.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.ui.totop.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-1.10.2.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-migrate.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-ui.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/setting.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/tie-scripts.js">

<!--[if IE]>

<script type="text/javascript">jQuery(document).ready(function () {

jQuery(".menu-item").has("ul").children("a").attr("aria-haspopup", "true");

});</script>

<![endif]-->

<!--[if lt IE 9]>

<script src="/js/html5.js"></script>

<script src="/js/selectivizr-min.js"></script>

<![endif]-->

<!--[if IE 8]>

<link rel="stylesheet" type="text/css" media="all" href="/css/ie8.css"/>

<![endif]-->

<meta property="og:title" content="LATEST NEWS UPDATES | Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi & Surabhi Agarwal" />

<meta property="og:url" content="https://im4change.in/latest-news-updates/jan-dhan-yojana-many-questions-remain-ishan-bakshi-nitin-sethi-surabhi-agarwal-4673846.html" />

<meta property="og:type" content="article" />

<meta property="og:description" content="

-The Business Standard

Against NDA's 75 million target, UPA added 61 million in 2013-14

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank..." />

<meta property="og:image" content="" />

<meta property="fb:app_id" content="0" />

<meta name="viewport" content="width=device-width, initial-scale=1, maximum-scale=1, user-scalable=no">

<link rel="apple-touch-icon-precomposed" sizes="144x144" href="https://im4change.in/images/apple1.png">

<link rel="apple-touch-icon-precomposed" sizes="120x120" href="https://im4change.in/images/apple2.png">

<link rel="apple-touch-icon-precomposed" sizes="72x72" href="https://im4change.in/images/apple3.png">

<link rel="apple-touch-icon-precomposed" href="https://im4change.in/images/apple4.png">

<style>

.gsc-results-wrapper-overlay{

top: 38% !important;

height: 50% !important;

}

.gsc-search-button-v2{

border-color: #035588 !important;

background-color: #035588 !important;

}

.gsib_a{

height: 30px !important;

padding: 2px 8px 1px 6px !important;

}

.gsc-search-button-v2{

height: 41px !important;

}

input.gsc-input{

background: none !important;

}

@media only screen and (max-width: 600px) {

.gsc-results-wrapper-overlay{

top: 11% !important;

width: 87% !important;

left: 9% !important;

height: 43% !important;

}

.gsc-search-button-v2{

padding: 10px 10px !important;

}

.gsc-input-box{

height: 28px !important;

}

/* .gsib_a {

padding: 0px 9px 4px 9px !important;

}*/

}

@media only screen and (min-width: 1200px) and (max-width: 1920px) {

table.gsc-search-box{

width: 15% !important;

float: right !important;

margin-top: -118px !important;

}

.gsc-search-button-v2 {

padding: 6px !important;

}

}

</style>

<script>

$(function () {

$("#accordion").accordion({

event: "click hoverintent"

});

});

/*

* hoverIntent | Copyright 2011 Brian Cherne

* http://cherne.net/brian/resources/jquery.hoverIntent.html

* modified by the jQuery UI team

*/

$.event.special.hoverintent = {

setup: function () {

$(this).bind("mouseover", jQuery.event.special.hoverintent.handler);

},

teardown: function () {

$(this).unbind("mouseover", jQuery.event.special.hoverintent.handler);

},

handler: function (event) {

var currentX, currentY, timeout,

args = arguments,

target = $(event.target),

previousX = event.pageX,

previousY = event.pageY;

function track(event) {

currentX = event.pageX;

currentY = event.pageY;

}

;

function clear() {

target

.unbind("mousemove", track)

.unbind("mouseout", clear);

clearTimeout(timeout);

}

function handler() {

var prop,

orig = event;

if ((Math.abs(previousX - currentX) +

Math.abs(previousY - currentY)) < 7) {

clear();

event = $.Event("hoverintent");

for (prop in orig) {

if (!(prop in event)) {

event[prop] = orig[prop];

}

}

// Prevent accessing the original event since the new event

// is fired asynchronously and the old event is no longer

// usable (#6028)

delete event.originalEvent;

target.trigger(event);

} else {

previousX = currentX;

previousY = currentY;

timeout = setTimeout(handler, 100);

}

}

timeout = setTimeout(handler, 100);

target.bind({

mousemove: track,

mouseout: clear

});

}

};

</script>

<script type="text/javascript">

var _gaq = _gaq || [];

_gaq.push(['_setAccount', 'UA-472075-3']);

_gaq.push(['_trackPageview']);

(function () {

var ga = document.createElement('script');

ga.type = 'text/javascript';

ga.async = true;

ga.src = ('https:' == document.location.protocol ? 'https://ssl' : 'http://www') + '.google-analytics.com/ga.js';

var s = document.getElementsByTagName('script')[0];

s.parentNode.insertBefore(ga, s);

})();

</script>

<link rel="stylesheet" href="/css/custom.css?v=1.16"/> <script src="/js/jquery.ui.totop.js?1575549704"></script> <script src="/js/setting.js?1575549704"></script> <link rel="manifest" href="/manifest.json">

<meta name="theme-color" content="#616163" />

<meta name="apple-mobile-web-app-capable" content="yes">

<meta name="apple-mobile-web-app-status-bar-style" content="black">

<meta name="apple-mobile-web-app-title" content="im4change">

<link rel="apple-touch-icon" href="/icons/logo-192x192.png">

</head>

<body id="top" class="home inner blog">

<div class="background-cover"></div>

<div class="wrapper animated">

<header id="theme-header" class="header_inner" style="position: relative;">

<div class="logo inner_logo" style="left:20px !important">

<a title="Home" href="https://im4change.in/">

<img src="https://im4change.in/images/logo2.jpg?1582080632" class="logo_image" alt="im4change"/> </a>

</div>

<div class="langhindi" style="color: #000;display:none;"

href="https://im4change.in/">

<a class="more-link" href="https://im4change.in/">Home</a>

<a href="https://im4change.in/hindi/" class="langbutton ">हिन्दी</a>

</div>

<nav class="fade-in animated2" id="main-nav">

<div class="container">

<div class="main-menu">

<ul class="menu" id="menu-main">

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children"

style="left: -40px;"><a

target="_blank" href="https://im4change.in/">Home</a>

</li>

<li class="menu-item mega-menu menu-item-type-taxonomy mega-menu menu-item-object-category mega-menu menu-item-has-children parent-list"

style=" margin-left: -40px;"><a href="#">KNOWLEDGE GATEWAY <span class="sub-indicator"></span>

</a>

<div class="mega-menu-block background_menu" style="padding-top:25px;">

<div class="container">

<div class="mega-menu-content">

<div class="mega-menu-item">

<h3><b>Farm Crisis</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/farmers039-suicides-14.html"

class="left postionrel">Farm Suicides </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/unemployment-30.html"

class="left postionrel">Unemployment </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/rural-distress-70.html"

class="left postionrel">Rural distress </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/migration-34.html"

class="left postionrel">Migration </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/key-facts-72.html"

class="left postionrel">Key Facts </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/debt-trap-15.html"

class="left postionrel">Debt Trap </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Empowerment</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/union-budget-73.html"

class="left postionrel">Union Budget And Other Economic Policies </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/forest-and-tribal-rights-61.html"

class="left postionrel">Forest and Tribal Rights </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-education-60.html"

class="left postionrel">Right to Education </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-food-59.html"

class="left postionrel">Right to Food </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/displacement-3279.html"

class="left postionrel">Displacement </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-work-mg-nrega-39.html"

class="left postionrel">Right to Work (MG-NREGA) </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/gender-3280.html"

class="left postionrel">GENDER </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-information-58.html"

class="left postionrel">Right to Information </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/social-audit-48.html"

class="left postionrel">Social Audit </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Hunger / HDI</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/poverty-and-inequality-20499.html"

class="left postionrel">Poverty and inequality </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/malnutrition-41.html"

class="left postionrel">Malnutrition </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/public-health-51.html"

class="left postionrel">Public Health </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/education-50.html"

class="left postionrel">Education </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/hunger-overview-40.html"

class="left postionrel">Hunger Overview </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/hdi-overview-45.html"

class="left postionrel">HDI Overview </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/pds-ration-food-security-42.html"

class="left postionrel">PDS/ Ration/ Food Security </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/sdgs-113.html"

class="left postionrel">SDGs </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/mid-day-meal-scheme-mdms-53.html"

class="left postionrel">Mid Day Meal Scheme (MDMS) </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Environment</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/time-bomb-ticking-52.html"

class="left postionrel">Time Bomb Ticking </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/water-and-sanitation-55.html"

class="left postionrel">Water and Sanitation </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/impact-on-agriculture-54.html"

class="left postionrel">Impact on Agriculture </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Law & Justice</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/social-justice-20500.html"

class="left postionrel">Social Justice </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/access-to-justice-47.html"

class="left postionrel">Access to Justice </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/human-rights-56.html"

class="left postionrel">Human Rights </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/corruption-35.html"

class="left postionrel">Corruption </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/general-insecurity-46.html"

class="left postionrel">General Insecurity </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/disaster-relief-49.html"

class="left postionrel">Disaster & Relief </a>

</p>

</div>

</div>

</div>

</div>

</li>

<li class="menu-item menu-item-type-post_type menu-item-object-page "><a target="_blank" href="https://im4change.in/nceus_reports.php">NCEUS reports</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children parent-list ">

<a target="_blank" href="https://im4change.in/about-us-9.html">About Us <span

class="sub-indicator"></span></a>

<ul class="sub-menu aboutmenu">

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/objectives-8.html">Objectives</a>

</li>

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/contactus.php">Contact

Us</a></li>

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/about-us-9.html">About

Us</a></li>

</ul>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children ">

<a target="_blank" href="https://im4change.in/fellowships.php" title="Fellowships">Fellowships</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/media-workshops.php">Workshops</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/research.php">Research</a></li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/links-64">Partners</a></li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children"

id="menu-item-539"><a target="_blank" href="https://im4change.in/hindi/"

class="langbutton langlinkfont17">हिन्दी</a></li>

</ul>

</div> </div>

<!-- <div style="float: right;">

<script async src="https://cse.google.com/cse.js?cx=18b4f2e0f11bed3dd"></script>

<div class="gcse-search"></div>

</div> -->

<div class="search-block" style=" margin-left: 8px; margin-right: 7px;">

<form method="get" id="searchform" name="searchform"

action="https://im4change.in/search"

onsubmit="return searchvalidate();">

<button class="search-button" type="submit" value="Search"></button>

<input type="text" id="s" name="qryStr" value=""

onfocus="if (this.value == 'Search...') {this.value = '';}"

onblur="if (this.value == '') {this.value = 'Search...';}">

</form>

</div>

</nav>

</header>

<div class="container">

<div id="main-content" class=" main1 container fade-in animated3 sidebar-narrow-left">

<div class="content-wrap">

<div class="content" style="width: 900px;min-height: 500px;">

<section class="cat-box recent-box innerCatRecent">

<h1 class="cat-box-title">Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi & Surabhi Agarwal</h1>

<a href="JavaScript:void(0);" onclick="return shareArticle(25809);">

<img src="https://im4change.in/images/email.png?1582080630" border="0" width="24" align="right" alt="Share this article"/> </a>

<a href="https://im4change.in/latest-news-updates/jan-dhan-yojana-many-questions-remain-ishan-bakshi-nitin-sethi-surabhi-agarwal-4673846/print"

rel="nofollow">

<img src="https://im4change.in/images/icon-print.png?1582080630" border="0" width="24" align="right" alt="Share this article"/>

</a>

</section>

<section class="recent-box innerCatRecent">

<small class="pb-1"><span class="dateIcn">

<img src="https://im4change.in/images/published.svg?1582080666" alt="published"/>

Published on</span><span class="text-date"> Aug 30, 2014</span>

<span

class="dateIcn">

<img src="https://im4change.in/images/modified.svg?1582080666" alt="modified"/> Modified on </span><span class="text-date"> Aug 30, 2014</span>

</small>

</section>

<div class="clear"></div>

<div style="padding-top: 10px;">

<div class="innerLineHeight">

<div class="middleContent innerInput latest-news-updates">

<table>

<tr>

<td>

<div>

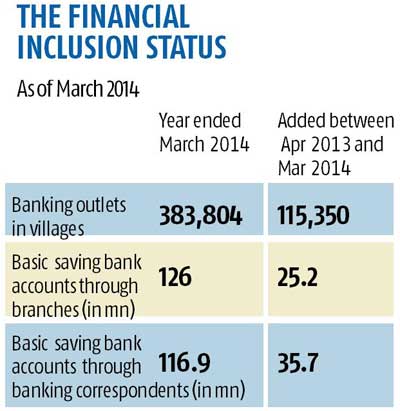

<div align="justify">-The Business Standard</div><p align="justify"><em>Against NDA's 75 million target, UPA added 61 million in 2013-14</em></p><p align="justify">The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank accounts under the scheme by Thursday and looked ahead to the target of achieving 75 million accounts by January 2015.</p><p align="justify"><img src="https://im4change.in/siteadmin/tinymce/uploaded/Financial Inclusion.jpg" alt="Financial Inclusion" width="400" height="411" /></p><p align="justify">In fact, given that the UPA government added an additional 60.9 million accounts in 2013-14, the target is an easy one. The real challenge is of keeping the accounts alive, funding the overdraft mechanism and ensuring confusion over the insurance cover is resolved.</p><p align="justify">A meeting on Monday in the finance ministry could resolve some of the make-or-break problems of the grand scheme. The finance ministry will try to resolve the confusion created over the account-linked accident insurance the government has already announced. Other components of the Jan Dhan scheme too are yet to be fleshed out. Each of the new bank accounts is to come with a RuPay debit card, a Rs 5,000 overdraft facility, a Rs 1 lakh accident insurance and Rs 30,000 life insurance. Keeping these accounts running, the insurance-claim system functional, funnelling money through cash transfer mechanisms and making the overdraft facilities financially viable will imply costs for different financial sector actors. Or, more likely, for these costs to be subsidised by the government.</p><p align="justify">"We know the costs involved from work done earlier for the direct benefit transfer and financial inclusion schemes. But this is really several schemes rolled into one over phases and we will have to sort the fine details," said a senior official in the government.</p><p align="justify">The immediate challenge for the government will be to figure out the financial viability of maintaining the accounts and the linked insurance schemes. The RBI-promoted National Payments Corporation of India (NPCI) which offers the RuPay card, had already given the contract for accident insurance to HDFC Ergo for a period of three years. But this insurance was linked to the transaction history of the accountholder. The industry was led to believe there would be an insurance top-up by the government on this of Rs 1 lakh, costing NPCI Rs 1 per customer every year.</p><p align="justify">NPCI plans the insurance cost from the income generated out of transaction on the RuPay platform.</p><p align="justify">For every ATM transaction the issuing bank pays NPCI 40 paise. For every point of sale or ecommerce transaction NPCI gets 60 paise from the issuing bank and 30 paise from the accepting bank. All existing RuPay debit card holders would be able to avail of this facility, sources told Business Standard but not those holding saving accounts without the RuPay card. The card itself will cost about Rs 50 each roughly, though the scale could bring down costs marginally, sources said.</p><p align="justify">A former banker also noted that the financial viability of running these millions of accounts would depend on the minimum balances maintained and the number of transactions carried out in a year. A source in the government said earlier assessments suggested that out of the 180 million bank accounts opened under the financial inclusion scheme so far, a vast majority sat dormant or unused once they were opened. The RBI also noted that even as the volume of accounts had increased substantially keeping the transactions flowing remained a challenge. In other words, the banking inclusion system generated empty accounts to meet set targets.</p><p align="justify">Back-of-the envelope calculations suggest that for public sector banks an average monthly balance of Rs 50,000 is essential to meet the costs of operating an account. But another expert who has worked on the banking correspondent model economics said a much lower average balance of Rs 15,000-12,000 could help banks meet costs. But for millions of poor who could finally have an account number, this is likely to be only a dream.</p><p align="justify">The overdraft facility that the Jan Dhan scheme commits could be valuable for the poor but clarity has still not emerged on where the funds would be diverted from to finance it. Some news reports suggest that the overdraft facility will be guaranteed by an Rs 1,000 crore fund from NABARD. But this may not be sufficient if the overdraft facility really takes off. Assuming one account each for 75 million households, an overdraft facility of Rs 5,000 each amounts to Rs 37,500 crore. Even if one is to assume a risk proportion of 20-25 per cent, it would imply a minimum of Rs 7,000 crore loss to the banking sector.</p><p align="justify">A more fundamental question that the scheme has not yet resolved is the last-mile connectivity essential for financial inclusion. The government says it would be based on banking correspondents, which are not brick and mortar banks but private companies. It's cheaper than running branches but still requiring a substantial flow of money to and from the accounts to generate commission for the agents involved. The last government was unable to ensure that flow in the absence of the fertiliser, food and kerosene subsidy being turned into cash-based ones. The previous government had assessed in its internal discussions that a robust and competitive banking correspondent model required at least 200,000 working sub-agents. If one was to expect these individuals to earn even Rs 1,000 a month from acting as the last-mile connector, the previous government had assessed it would require moving the entire social sector subsidy bill through the banking correspondent funnel, including MNREGA, food, fertiliser and kerosene subsidies. This has not happened and while India already has 248,000 sub-agents most of them do not really work. Hiring an additional 50,000 sub-agents that get paid Rs 5,000 a month is bound to not be productive either.</p><p align="justify">The costs of running this banking correspondent model will be tested even more as the financial inclusion scheme reaches deeper into rural India, sources admit. "If one wants these accounts to be functional and not remain dormant then the density of banking correspondent has to be increased. But that also increases the cost of delivery," explained an official who had worked on this scheme in the previous government.</p><p align="justify">Additionally, the economics of the cash transfer schemes for the banks would be dependent on what kind of float period is allowed by the government and not just the volume of funds involved.</p><p align="justify">--</p><p align="justify"><strong>PROBLEM AREAS</strong></p><p align="justify"><strong> </strong>Accident insurance cover Meeting on Monday to resolve confusion<br /> Funding the banking correspondent model finance unclear. 248,000 correspondent agents in country<br /> Cost of overdraft facility No clarity on who shall bear the cost<br /> Existing saving accounts without RuPay card not to get other benefits<br /> Creating new accounts not a challenge, increasing transaction per account is</p>

</div>

</td>

</tr>

</table>

</div>

</div>

</div>

<div class="clear"></div>

<br><a href="http://wap.business-standard.com/article/economy-policy/jan-dhan-yojana-many-questions-remain-114083000024_1.html" class="re" target="_blank">The Business Standard, 30 August, 2014, http://wap.business-standard.com/article/economy-policy/jan-dhan-yojana-many-questions-remain-114083000024_1.html</a><div class="clear"></div>

<div style="padding-top: 18px;">

<p class="post-tag">Tagged with:

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Below Poverty Line"

title="Below Poverty Line">

Below Poverty Line </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Jan Dhan Yojana"

title="Jan Dhan Yojana">

Jan Dhan Yojana </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Financial Inclusion"

title="Financial Inclusion">

Financial Inclusion </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=banking"

title="banking">

banking </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Poverty"

title="Poverty">

Poverty </a>

</p>

</div>

<div class="clear"></div>

<br><br>

<div class="widget-top">

<h4>Related Articles</h4>

<div class="stripe-line"></div>

</div>

<div class="widget-container">

<ul id="recentcomments">

<li class="recentcomments">

<a href="https://im4change.in/news-alerts-57/135-million-indians-exited-multidimensional-poverty-as-per-government-figures-is-that-the-same-as-poverty-reduction.html"

title="135 Million Indians Exited “Multidimensional" Poverty as per Government Figures. Is that the same as Poverty Reduction?">

135 Million Indians Exited “Multidimensional" Poverty as per Government Figures. Is that the same as Poverty Reduction? </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/india-may-have-seen-steepest-dip-in-multidimensional-poverty-among-110-nations-as-per-undp-data-nikhil-rampal.html"

title="India may have seen steepest dip in multidimensional poverty among 110 nations as per UNDP data - Nikhil Rampal">

India may have seen steepest dip in multidimensional poverty among 110 nations as per UNDP data - Nikhil Rampal </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/india-s-stretched-health-care-system-fails-millions-in-rural-areas-battling-sickle-cell-disease-abc.html"

title="India's stretched health care system fails millions in rural areas battling sickle cell disease - ABC">

India's stretched health care system fails millions in rural areas battling sickle cell disease - ABC </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/34-million-or-373-million-do-we-know-how-many-in-india-are-poor-nushaiba-iqbal.html"

title="34 Million or 373 Million: Do We Know How Many In India Are Poor? - Nushaiba Iqbal">

34 Million or 373 Million: Do We Know How Many In India Are Poor? - Nushaiba Iqbal </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/news-alerts-57/nsso-survey-only-39-1-of-all-households-have-drinking-water-within-dwelling-46-7-of-rural-households-use-firewood-for-cooking.html"

title="NSSO Survey: Only 39.1% of all Households have Drinking Water Within Dwelling, 46.7% of Rural Households use Firewood for Cooking">

NSSO Survey: Only 39.1% of all Households have Drinking Water Within Dwelling, 46.7% of Rural Households use Firewood for Cooking </a>

</li>

</ul>

</div>

<div class="comment-respond" id="respond">

<a name="commentbox"> </a>

<h3 class="comment-reply-title" id="reply-title">Write Comments</h3>

<form method="post" accept-charset="utf-8" role="form" action="/latest-news-updates/jan-dhan-yojana-many-questions-remain-ishan-bakshi-nitin-sethi-surabhi-agarwal-4673846.html"><div style="display:none;"><input type="hidden" name="_method" value="POST"/></div> <form class="comment-form" id="commentform" method="post" action="#commentbox" onSubmit="return validate()"

name="cmtform">

<input type="hidden" name="cmttype" value="articlecmt"/>

<input type="hidden" name="article_id" value="25809"/>

<p class="comment-notes">Your email address will not be published. Required fields are marked <span

class="required">*</span></p>

<p class="comment-form-author">

<label for="commenterName">Name</label>

<span class="required">*</span>

<input type="text" aria-required="true" size="30"

value=""

name="commenterName" id="commenterName" required="true">

</p>

<p class="comment-form-email">

<label for="commenterEmail">Email</label> <span class="required">*</span>

<input aria-required="true" size="30" name="commenterEmail" id="commenterEmail" type="email"

value=""

required="true">

</p>

<p class="comment-form-contact">

<label for="commenterPh">Contact No.</label>

<input type="text" size="30"

value=""

name="commenterPh" id="commenterPh">

</p>

<p class="comment-form-comment">

<label for="comment">Comment</label>

<textarea aria-required="true" required="true" rows="8" cols="45" name="comment"

id="comment"></textarea>

</p>

<p class="comment-form-comment">

<label for="comment">Type the characters you see in the image below <span class="required">*</span><br><img

class="captchaImg"

src="https://im4change.in/securimage_show_art.php?tk=543836997" alt="captcha"/>

</label>

</p>

<input type="text" name="vrcode" required="true"/>

<p class="form-submit" style="width: 200px;">

<input type="submit" value="Post Comment" id="submit" name="submit">

</p></form>

</div>

<style>

.ui-widget-content {

height: auto !important;

}

</style>

<div id="share-modal"></div>

<style>

.middleContent a{

background-color: rgba(108,172,228,.2);

}

.middleContent a:hover{

background-color: #418fde;

border-color: #418fde;

color: #000;

}

</style>

<script>

function shareArticle(article_id) {

var options = {

modal: true,

height: 'auto',

width: 600 + 'px'

};

$('#share-modal').html("");

$('#share-modal').load('https://im4change.in/share_article?article_id=' + article_id).dialog(options).dialog('open');

}

function postShare() {

var param = 'article_id=' + $("#article_id").val();

param = param + '&y_name=' + $("#y_name").val();

param = param + '&y_email=' + $("#y_email").val();

param = param + '&f_name=' + $("#f_name").val();

param = param + '&f_email=' + $("#f_email").val();

param = param + '&y_msg=' + $("#y_msg").val();

$.ajax({

type: "POST",

url: 'https://im4change.in/post_share_article',

data: param,

success: function (response) {

$('#share-modal').html("Thank You, Your message posted to ");

}

});

return false;

}

</script> </div>

</div>

<!-- Right Side Section Start -->

<!-- MAP Section START -->

<aside class="sidebar indexMarg">

<div class="ad-cell">

<a href="https://im4change.in/statemap.php" title="">

<img src="https://im4change.in/images/map_new_version.png?1582080666" alt="India State Map" class="indiamap" width="232" height="252"/> </a>

<div class="rightmapbox">

<div id="sideOne" class="docltitle"><a href="https://im4change.in/state-report/india/36" target="_blank">DOCUMENTS/

REPORTS</a></div>

<div id="sideTwo" class="statetitle"><a href="https://im4change.in/states.php"target="_blank">STATE DATA/

HDRs.</a></div>

</div>

<div class="widget widgePadTop"></div>

</div>

</aside>

<!-- MAP Section END -->

<aside class="sidebar sidePadbottom">

<div class="rightsmlbox1" >

<a href="https://im4change.in/knowledge_gateway" target="_blank" style="color: #035588;

font-size: 17px;">

KNOWLEDGE GATEWAY

</a>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title">

<a href="https://im4change.in/newsletter" target="_blank">

NEWSLETTER

</a>

</p>

</div>

</div>

<div class="rightsmlbox1" style="height: 325px;">

<div>

<p class="rightsmlbox1_title">

Interview with Prof. Ravi Srivastava

</p>

<p class="rightsmlbox1_title">

<a href="https://im4change.in/video/interview-with-prof-ravi-srivastava-on-current-economic-crisis">

<img width="250" height="200" src="/images/interview_video_home.jpg" alt="Interview with Prof. Ravi Srivastava"/>

</a>

<!--

<iframe width="250" height="200" src="https://www.youtube.com/embed/MmaTlntk-wc" frameborder="0" allow="accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture" allowfullscreen=""></iframe>-->

</p>

<a href="https://im4change.in/videogallery" class="more-link CatArchalAnch1" target="_blank">

More videos

</a>

</div>

</div>

<div class="rightsmlbox1">

<div>

<!--div id="sstory" class="rightboxicons"></div--->

<p class="rightsmlbox1_title"><a href="https://im4change.in/list-success-stories" target="_blank">Success Stories</a></p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a

href="https://im4change.in/interviews" target="_blank">Interviews</a>

</p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a href="https://www.commoncause.in/page.php?id=10" >Donate</a></p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a

href="https://im4change.in/marquee"

class="isf_link more-link" title="India Focus?" style="border: 4px solid #fdd922;width: 90%;background-color: #fdd922;text-align: center;color: #000000;font-size:18px" target="_blank">India Focus</a></p> </div>

</div>

<div class="rightsmlbox1" style="height: 104px !important;">

<a href="https://im4change.in/quarterly_reports.php" target="_blank">

Quarterly Reports on Effect of Economic Slowdown on Employment in India (2008 - 2015)

</a>

</div>

<!-- <div class="rightsmlbox1">

<a href="https://play.google.com/store/apps/details?id=com.im4.im4change" target="_blank">

</a></div> -->

<!-- <section class="cat-box recent-box secMarg">

<h2 class="cat-box-title">Most Visited</h2>

</section> -->

<!-- accordion Starts here -->

<!-- <div id="accordion" class="accordMarg">

</div> -->

<!-- accordion ends here -->

<!-- Widget Tag Cloud Starts here -->

<div id="tag_cloud-2" class="widget widget_tag_cloud">

<section class="cat-box recent-box secMarg">

<h2 class="cat-box-title">MOST VISITED TAGS</h2>

</section>

<div class="widget-top wiPdTp">

<div class="stripe-line"></div>

</div>

<div class="widget-container">

<div class="tagcloud">

<a href="https://im4change.in/search?qryStr=Agriculture"

target="_blank" class="tag-link-4 font4">Agriculture</a>

<a href="https://im4change.in/search?qryStr=Food Security"

target="_blank" class="tag-link-4 font4">Food Security</a>

<a href="https://im4change.in/search?qryStr=Law and Justice"

target="_blank" class="tag-link-4 font4">Law and Justice</a>

<a href="https://im4change.in/search?qryStr=Health"

target="_blank" class="tag-link-4 font4">Health</a>

<a href="https://im4change.in/search?qryStr=Right to Food"

target="_blank" class="tag-link-4 font4">Right to Food</a>

<a href="https://im4change.in/search?qryStr=Corruption"

target="_blank" class="tag-link-4 font4">Corruption</a>

<a href="https://im4change.in/search?qryStr=farming"

target="_blank" class="tag-link-4 font4">farming</a>

<a href="https://im4change.in/search?qryStr=Environment"

target="_blank" class="tag-link-4 font4">Environment</a>

<a href="https://im4change.in/search?qryStr=Right to Information"

target="_blank" class="tag-link-4 font4">Right to Information</a>

<a href="https://im4change.in/search?qryStr=NREGS"

target="_blank" class="tag-link-4 font4">NREGS</a>

<a href="https://im4change.in/search?qryStr=Human Rights"

target="_blank" class="tag-link-4 font4">Human Rights</a>

<a href="https://im4change.in/search?qryStr=Governance"

target="_blank" class="tag-link-4 font4">Governance</a>

<a href="https://im4change.in/search?qryStr=PDS"

target="_blank" class="tag-link-4 font4">PDS</a>

<a href="https://im4change.in/search?qryStr=COVID-19"

target="_blank" class="tag-link-4 font4">COVID-19</a>

<a href="https://im4change.in/search?qryStr=Land Acquisition"

target="_blank" class="tag-link-4 font4">Land Acquisition</a>

<a href="https://im4change.in/search?qryStr=mgnrega"

target="_blank" class="tag-link-4 font4">mgnrega</a>

<a href="https://im4change.in/search?qryStr=Farmers"

target="_blank" class="tag-link-4 font4">Farmers</a>

<a href="https://im4change.in/search?qryStr=transparency"

target="_blank" class="tag-link-4 font4">transparency</a>

<a href="https://im4change.in/search?qryStr=Gender"

target="_blank" class="tag-link-4 font4">Gender</a>

<a href="https://im4change.in/search?qryStr=Poverty"

target="_blank" class="tag-link-4 font4">Poverty</a>

<a href="https://im4change.in/search?qryStr=Farm Laws" target="_blank" class="tag-link-4 font4">Farm Laws

</a>

<a href="https://im4change.in/search?qryStr=Citizenship Amendment Act" target="_blank" class="tag-link-4 font4">Citizenship Amendment Act

</a>

<a href="https://im4change.in/search?qryStr=CAA NPR NRIC" target="_blank" class="tag-link-4 font4">CAA NPR NRIC

</a>

<a href="https://im4change.in/search?qryStr=Job Losses" target="_blank" class="tag-link-4 font4">Job Losses

</a>

<a href="https://im4change.in/search?qryStr=Migrant Workers" target="_blank" class="tag-link-4 font4">Migrant Workers

</a>

<a href="https://im4change.in/search?qryStr=Unemployment" target="_blank" class="tag-link-4 font4">Unemployment

</a>

<a href="https://im4change.in/search?qryStr=PMGKAY" target="_blank" class="tag-link-4 font4">PMGKAY

</a>

<a href="https://im4change.in/search?qryStr=PM-KISAN" target="_blank" class="tag-link-4 font4">PM-KISAN

</a>

<a href="https://im4change.in/search?qryStr=PM-CARES" target="_blank" class="tag-link-4 font4">PM-CARES

</a>

<a href="https://im4change.in/search?qryStr=LFPR" target="_blank" class="tag-link-4 font4">LFPR

</a>

</div>

</div>

</div>

<!-- Widget Tag Cloud Ends here -->

</aside>

<!-- Right Side Section End -->

</div>

<section class="cat-box cats-review-box footerSec">

<h2 class="cat-box-title vSec CatArcha">Video

Archives</h2>

<h2 class="cat-box-title CatArchaTitle">Archives</h2>

<div class="cat-box-content">

<div class="reviews-cat">

<div class="CatArchaDiv1">

<div class="CatArchaDiv2">

<ul>

<li>

<a href="https://im4change.in/news-alerts-57/moving-upstream-luni-fellowship.html" target="_blank">

Moving Upstream: Luni – Fellowship </a>

</li>

<li>

<a href="https://im4change.in/news-alerts-57/135-million-indians-exited-multidimensional-poverty-as-per-government-figures-is-that-the-same-as-poverty-reduction.html" target="_blank">

135 Million Indians Exited “Multidimensional" Poverty as per Government... </a>

</li>

<li>

<a href="https://im4change.in/news-alerts-57/explainer-why-are-tomato-prices-on-fire.html" target="_blank">

Explainer: Why are Tomato Prices on Fire? </a>

</li>

<li>

<a href="https://im4change.in/news-alerts-57/nsso-survey-only-39-1-of-all-households-have-drinking-water-within-dwelling-46-7-of-rural-households-use-firewood-for-cooking.html" target="_blank">

NSSO Survey: Only 39.1% of all Households have Drinking... </a>

</li>

<li class="CatArchalLi1">

<a href="https://im4change.in/news-alerts-57"

class="more-link CatArchalAnch1" target="_blank">

More...

</a>

</li>

</ul>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/I51LYnP8BOk/1.jpg"

alt=" Im4Change.org हिंदी वेबसाइट का परिचय. Short Video on im4change.org...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Short-Video-on-im4change-Hindi-website-Inclusive-Media-for-Change" target="_blank">

Im4Change.org हिंदी वेबसाइट का परिचय. Short Video on im4change.org... </a>

</p>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/kNqha-SwfIY/1.jpg"

alt=" "Session 1: Scope of IDEA and AgriStack" in Exploring...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Session-1- Scope-of-IDEA-and-AgriStack-in-Exploring-Digitalisation-in-Agriculture-29-April-2022" target="_blank">

"Session 1: Scope of IDEA and AgriStack" in Exploring... </a>

</p>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/6kIVjlgZItk/1.jpg"

alt=" "Session 2: Farmer Centric Digitalisation in Agriculture" in Exploring...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Session-2-Farmer-Centric-Digitalisation-in-Agriculture-in-Exploring-Digitalisation-in-Agriculture-29-April-2022" target="_blank">

"Session 2: Farmer Centric Digitalisation in Agriculture" in Exploring... </a>

</p>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/2BeHTu0y7xc/1.jpg"

alt=" "Session 3: Future of Digitalisation in Agriculture" in Exploring...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Session-3-Future-of-Digitalisation-in-Agriculture-in-Exploring-Digitalisation-in-Agriculture-29-April-2022" target="_blank">

"Session 3: Future of Digitalisation in Agriculture" in Exploring... </a>

</p>

</div>

<div class="divWidth">

<ul class="divWidthMarg">

<li>

<a href="https://im4change.in/video/Public-Spending-on-Agriculture-in-India-Source-Foundation-for-Agrarian-Studies"

title="Public Spending on Agriculture in India (Source: Foundation for Agrarian Studies)" target="_blank">

Public Spending on Agriculture in India (Source: Foundation for...</a>

</li>

<li>

<a href="https://im4change.in/video/Agrarian-Change-Seminar-Protests-against-the-New-Farm-Laws-in-India-by-Prof-Vikas-Rawal-JNU-Source-Journal-Of-Agrarian-Change"

title="Agrarian Change Seminar: 'Protests against the New Farm Laws in India' by Prof. Vikas Rawal, JNU (Source: Journal Of Agrarian Change) " target="_blank">

Agrarian Change Seminar: 'Protests against the New Farm Laws...</a>

</li>

<li>

<a href="https://im4change.in/video/Webinar-Ramrao-The-Story-of-India-Farm-Crisis-Source-Azim-Premji-University"

title="Webinar: Ramrao - The Story of India's Farm Crisis (Source: Azim Premji University)" target="_blank">

Webinar: Ramrao - The Story of India's Farm Crisis...</a>

</li>

<li>

<a href="https://im4change.in/video/water-and-agricultural-transformation-in-India"

title="Water and Agricultural Transformation in India: A Symbiotic Relationship (Source: IGIDR)" target="_blank">

Water and Agricultural Transformation in India: A Symbiotic Relationship...</a>

</li>

<li class="CatArchalLi1">

<a href="https://im4change.in/videogallery"

class="more-link CatArchalAnch1" target="_blank">

More...

</a>

</li>

</ul>

</div>

</div>

</div>

</div>

</section> </div>

<div class="clear"></div>

<!-- Footer option Starts here -->

<div class="footer-bottom fade-in animated4">

<div class="container">

<div class="social-icons icon_flat">

<p class="SocialMargTop"> Website Developed by <a target="_blank" title="Web Development"

class="wot right"

href="http://www.ravinderkhurana.com/" rel="nofollow">

RAVINDErkHURANA.com</a></p>

</div>

<div class="alignleft">

<a

target="_blank" href="https://im4change.in/objectives-8.html"

class="link"

title="Objectives">Objectives</a> | <a

target="_blank" href="https://im4change.in/about-us-9.html"

class="link" title="About Us">About Us</a> | <a

target="_blank" href="https://im4change.in/media-workshops.php"

class="ucwords">Workshops</a> | <a

target="_blank" href="https://im4change.in/disclaimer/disclaimer-149.html"

title="Disclaimer">Disclaimer</a> </div>

</div>

</div>

<!-- Footer option ends here -->

</div>

<div id="connect">

<a target="_blank"

href="http://www.facebook.com/sharer.php?u=https://im4change.in/latest-news-updates/jan-dhan-yojana-many-questions-remain-ishan-bakshi-nitin-sethi-surabhi-agarwal-4673846.html"

title="Share on Facebook">

<img src="https://im4change.in/images/Facebook.png?1582080640" alt="share on Facebook" class="ImgBorder"/>

</a><br/>

<a target="_blank"

href="http://twitter.com/share?text=Im4change&url=https://im4change.in/latest-news-updates/jan-dhan-yojana-many-questions-remain-ishan-bakshi-nitin-sethi-surabhi-agarwal-4673846.html"

title="Share on Twitter">

<img src="https://im4change.in/images/twitter.png?1582080632" alt="Twitter" class="ImgBorder"/> </a>

<br/>

<a href="/feeds" title="RSS Feed" target="_blank">

<img src="https://im4change.in/images/rss.png?1582080632" alt="RSS" class="ImgBorder"/>

</a>

<br/>

<a class="feedback-link" id="feedbackFormLink" href="#">

<img src="https://im4change.in/images/feedback.png?1582080630" alt="Feedback" class="ImgBorder"/>

</a> <br/>

<a href="javascript:function iprl5(){var d=document,z=d.createElement('scr'+'ipt'),b=d.body,l=d.location;try{if(!b)throw(0);d.title='(Saving...) '+d.title;z.setAttribute('src',l.protocol+'//www.instapaper.com/j/WKrH3R7ORD5p?u='+encodeURIComponent(l.href)+'&t='+(new Date().getTime()));b.appendChild(z);}catch(e){alert('Please wait until the page has loaded.');}}iprl5();void(0)"

class="bookmarklet" onclick="return explain_bookmarklet();">

<img src="https://im4change.in/images/read-it-later.png?1582080632" alt="Read Later" class="ImgBorder"/> </a>

</div>

<!-- Feedback form Starts here -->

<div id="feedbackForm" class="overlay_form" class="ImgBorder">

<h2>Contact Form</h2>

<div id="contactform1">

<div id="formleft">

<form id="submitform" action="/contactus.php" method="post">

<input type="hidden" name="submitform" value="submitform"/>

<input type="hidden" name="salt_key" value="a0e0f2c6a0644a70e57ad2c96829709a"/>

<input type="hidden" name="ref" value="feedback"/>

<fieldset>

<label>Name :</label>

<input type="text" name="name" class="tbox" required/>

</fieldset>

<fieldset>

<label>Email :</label>

<input type="text" name="email" class="tbox" required/>

</fieldset>

<fieldset>

<label>Message :</label>

<textarea rows="5" cols="20" name="message" required></textarea>

</fieldset>

<fieldset>

Please enter security code

<div class="clear"></div>

<input type="text" name="vrcode" class="tbox"/>

</fieldset>

<fieldset>

<input type="submit" class="button" value="Submit"/>

<a href="#" id="closefeedbakcformLink">Close</a>

</fieldset>

</form>

</div>

<div class="clearfix"></div>

</div>

</div>

<div id="donate_popup" class="modal" style="max-width: 800px;">

<table width="100%" border="1">

<tr>

<td colspan="2" align="center">

<b>Support im4change</b>

</td>

</tr>

<tr>

<td width="25%" valign="middle">

<img src="https://im4change.in/images/logo2.jpg?1582080632" alt="" width="100%"/> </td>

<td style="padding-left:10px;padding-top:10px;">

<form action="https://im4change.in/donate" method="get">

<table width="100%" cellpadding="2" cellspacing="2">

<tr>

<td width="33%" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

10

</td>

<td width="33%" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

100

</td>

<td width="33%" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

1000

</td>

</tr>

<tr>

<td colspan="3">

</td>

</tr>

<tr>

<td style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

50

</td>

<td style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

500

</td>

<td style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

<input type="text" name="price" placeholder="?" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

</td>

</tr>

<tr>

<td colspan="3">

</td>

</tr>

<tr>

<td colspan="3" align="right">

<input type="button" name="Pay" value="Pay"

style="width: 200px;background-color: rgb(205, 35, 36);color: #ffffff;"/>

</td>

</tr>

</table>

</form>

</td>

</tr>

</table>

</div><script type='text/javascript'>

/* <![CDATA[ */

var tievar = {'go_to': 'Go to...'};

/* ]]> */

</script>

<script src="/js/tie-scripts.js?1575549704"></script><script src="/js/bootstrap.js?1575549704"></script><script src="/js/jquery.modal.min.js?1578284310"></script><script>

$(document).ready(function() {

// tell the autocomplete function to get its data from our php script

$('#s').autocomplete({

source: "/autocomplete"

});

});

</script>

<script src="/vj-main-sw-register.js" async></script>

<script>function init(){var imgDefer=document.getElementsByTagName('img');for(var i=0;i<imgDefer.length;i++){if(imgDefer[i].getAttribute('data-src')){imgDefer[i].setAttribute('src',imgDefer[i].getAttribute('data-src'))}}}

window.onload=init;</script>

</body>

</html>'

}

$maxBufferLength = (int) 8192

$file = '/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php'

$line = (int) 853

$message = 'Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853'

Cake\Http\ResponseEmitter::emit() - CORE/src/Http/ResponseEmitter.php, line 48

Cake\Http\Server::emit() - CORE/src/Http/Server.php, line 141

[main] - ROOT/webroot/index.php, line 39

Warning (2): Cannot modify header information - headers already sent by (output started at /home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php:853) [CORE/src/Http/ResponseEmitter.php, line 148]

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html>

<!--[if lt IE 7 ]>

<html class="ie ie6" lang='en'> <![endif]-->

<!--[if IE 7 ]>

<html class="ie ie7" lang='en'> <![endif]-->

<!--[if IE 8 ]>

<html class="ie ie8" lang='en'> <![endif]-->

<!--[if (gte IE 9)|!(IE)]><!-->

<html lang='en'>

<!--<![endif]-->

<head><meta http-equiv="Content-Type" content="text/html; charset=utf-8">

<title>

LATEST NEWS UPDATES | Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi & Surabhi Agarwal </title>

<meta name="description" content="

-The Business Standard

Against NDA's 75 million target, UPA added 61 million in 2013-14

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank..."/>

<meta name="keywords" content="Below Poverty Line,Jan Dhan Yojana,Financial Inclusion,banking,Poverty"/>

<meta name="news_keywords" content="Below Poverty Line,Jan Dhan Yojana,Financial Inclusion,banking,Poverty">

<link rel="alternate" type="application/rss+xml" title="ROR" href="/ror.xml"/>

<link rel="alternate" type="application/rss+xml" title="RSS 2.0" href="/feeds/"/>

<link rel="stylesheet" href="/css/bootstrap.min.css?1697864993"/> <link rel="stylesheet" href="/css/style.css?v=1.1.2"/> <link rel="stylesheet" href="/css/style-inner.css?1577045210"/> <link rel="stylesheet" id="Oswald-css"

href="https://fonts.googleapis.com/css?family=Oswald%3Aregular%2C700&ver=3.8.1" type="text/css"

media="all">

<link rel="stylesheet" href="/css/jquery.modal.min.css?1578285302"/> <script src="/js/jquery-1.10.2.js?1575549704"></script> <script src="/js/jquery-migrate.min.js?1575549704"></script> <link rel="shortcut icon" href="/favicon.ico" title="Favicon">

<link rel="stylesheet" href="/css/jquery-ui.css?1580720609"/> <script src="/js/jquery-ui.js?1575549704"></script> <link rel="preload" as="style" href="https://www.im4change.org/css/custom.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery.modal.min.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery-ui.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/li-scroller.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<!-- <link rel="preload" as="style" href="https://www.im4change.org/css/style.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous"> -->

<link rel="preload" as="style" href="https://www.im4change.org/css/style-inner.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel='dns-prefetch' href="//im4change.org/css/custom.css" crossorigin >

<link rel="preload" as="script" href="https://www.im4change.org/js/bootstrap.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.li-scroller.1.0.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.modal.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.ui.totop.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-1.10.2.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-migrate.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-ui.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/setting.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/tie-scripts.js">

<!--[if IE]>

<script type="text/javascript">jQuery(document).ready(function () {

jQuery(".menu-item").has("ul").children("a").attr("aria-haspopup", "true");

});</script>

<![endif]-->

<!--[if lt IE 9]>

<script src="/js/html5.js"></script>

<script src="/js/selectivizr-min.js"></script>

<![endif]-->

<!--[if IE 8]>

<link rel="stylesheet" type="text/css" media="all" href="/css/ie8.css"/>

<![endif]-->

<meta property="og:title" content="LATEST NEWS UPDATES | Jan Dhan Yojana: Many questions remain -Ishan Bakshi, Nitin Sethi & Surabhi Agarwal" />

<meta property="og:url" content="https://im4change.in/latest-news-updates/jan-dhan-yojana-many-questions-remain-ishan-bakshi-nitin-sethi-surabhi-agarwal-4673846.html" />

<meta property="og:type" content="article" />

<meta property="og:description" content="

-The Business Standard

Against NDA's 75 million target, UPA added 61 million in 2013-14

The government's financial inclusion scheme, Pradhan Mantri Jan Dhan Yojana, is an empty shell at the moment. The government heralded its achievement of clocking 15 million new bank..." />

<meta property="og:image" content="" />

<meta property="fb:app_id" content="0" />

<meta name="viewport" content="width=device-width, initial-scale=1, maximum-scale=1, user-scalable=no">

<link rel="apple-touch-icon-precomposed" sizes="144x144" href="https://im4change.in/images/apple1.png">

<link rel="apple-touch-icon-precomposed" sizes="120x120" href="https://im4change.in/images/apple2.png">

<link rel="apple-touch-icon-precomposed" sizes="72x72" href="https://im4change.in/images/apple3.png">

<link rel="apple-touch-icon-precomposed" href="https://im4change.in/images/apple4.png">

<style>

.gsc-results-wrapper-overlay{

top: 38% !important;

height: 50% !important;

}

.gsc-search-button-v2{

border-color: #035588 !important;

background-color: #035588 !important;

}

.gsib_a{

height: 30px !important;

padding: 2px 8px 1px 6px !important;

}

.gsc-search-button-v2{

height: 41px !important;

}

input.gsc-input{

background: none !important;

}

@media only screen and (max-width: 600px) {

.gsc-results-wrapper-overlay{

top: 11% !important;

width: 87% !important;

left: 9% !important;

height: 43% !important;

}

.gsc-search-button-v2{

padding: 10px 10px !important;

}

.gsc-input-box{

height: 28px !important;

}

/* .gsib_a {

padding: 0px 9px 4px 9px !important;

}*/

}

@media only screen and (min-width: 1200px) and (max-width: 1920px) {

table.gsc-search-box{

width: 15% !important;

float: right !important;

margin-top: -118px !important;

}

.gsc-search-button-v2 {

padding: 6px !important;

}

}

</style>

<script>

$(function () {

$("#accordion").accordion({

event: "click hoverintent"

});

});

/*

* hoverIntent | Copyright 2011 Brian Cherne

* http://cherne.net/brian/resources/jquery.hoverIntent.html

* modified by the jQuery UI team

*/

$.event.special.hoverintent = {

setup: function () {

$(this).bind("mouseover", jQuery.event.special.hoverintent.handler);

},

teardown: function () {

$(this).unbind("mouseover", jQuery.event.special.hoverintent.handler);

},

handler: function (event) {

var currentX, currentY, timeout,

args = arguments,

target = $(event.target),

previousX = event.pageX,

previousY = event.pageY;

function track(event) {

currentX = event.pageX;

currentY = event.pageY;

}

;

function clear() {

target

.unbind("mousemove", track)

.unbind("mouseout", clear);

clearTimeout(timeout);

}

function handler() {

var prop,

orig = event;

if ((Math.abs(previousX - currentX) +

Math.abs(previousY - currentY)) < 7) {

clear();

event = $.Event("hoverintent");

for (prop in orig) {

if (!(prop in event)) {

event[prop] = orig[prop];

}

}

// Prevent accessing the original event since the new event

// is fired asynchronously and the old event is no longer

// usable (#6028)

delete event.originalEvent;

target.trigger(event);

} else {

previousX = currentX;

previousY = currentY;

timeout = setTimeout(handler, 100);

}

}

timeout = setTimeout(handler, 100);

target.bind({

mousemove: track,

mouseout: clear

});

}

};

</script>

<script type="text/javascript">

var _gaq = _gaq || [];

_gaq.push(['_setAccount', 'UA-472075-3']);

_gaq.push(['_trackPageview']);

(function () {

var ga = document.createElement('script');

ga.type = 'text/javascript';

ga.async = true;

ga.src = ('https:' == document.location.protocol ? 'https://ssl' : 'http://www') + '.google-analytics.com/ga.js';

var s = document.getElementsByTagName('script')[0];

s.parentNode.insertBefore(ga, s);

})();

</script>

<link rel="stylesheet" href="/css/custom.css?v=1.16"/> <script src="/js/jquery.ui.totop.js?1575549704"></script> <script src="/js/setting.js?1575549704"></script> <link rel="manifest" href="/manifest.json">

<meta name="theme-color" content="#616163" />

<meta name="apple-mobile-web-app-capable" content="yes">

<meta name="apple-mobile-web-app-status-bar-style" content="black">

<meta name="apple-mobile-web-app-title" content="im4change">

<link rel="apple-touch-icon" href="/icons/logo-192x192.png">

</head>

<body id="top" class="home inner blog">

<div class="background-cover"></div>

<div class="wrapper animated">

<header id="theme-header" class="header_inner" style="position: relative;">

<div class="logo inner_logo" style="left:20px !important">

<a title="Home" href="https://im4change.in/">

<img src="https://im4change.in/images/logo2.jpg?1582080632" class="logo_image" alt="im4change"/> </a>

</div>

<div class="langhindi" style="color: #000;display:none;"

href="https://im4change.in/">

<a class="more-link" href="https://im4change.in/">Home</a>

<a href="https://im4change.in/hindi/" class="langbutton ">हिन्दी</a>

</div>

<nav class="fade-in animated2" id="main-nav">

<div class="container">

<div class="main-menu">

<ul class="menu" id="menu-main">

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children"

style="left: -40px;"><a

target="_blank" href="https://im4change.in/">Home</a>

</li>

<li class="menu-item mega-menu menu-item-type-taxonomy mega-menu menu-item-object-category mega-menu menu-item-has-children parent-list"

style=" margin-left: -40px;"><a href="#">KNOWLEDGE GATEWAY <span class="sub-indicator"></span>

</a>

<div class="mega-menu-block background_menu" style="padding-top:25px;">

<div class="container">

<div class="mega-menu-content">

<div class="mega-menu-item">

<h3><b>Farm Crisis</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/farmers039-suicides-14.html"

class="left postionrel">Farm Suicides </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/unemployment-30.html"

class="left postionrel">Unemployment </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/rural-distress-70.html"

class="left postionrel">Rural distress </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/migration-34.html"

class="left postionrel">Migration </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/key-facts-72.html"

class="left postionrel">Key Facts </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/debt-trap-15.html"

class="left postionrel">Debt Trap </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Empowerment</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/union-budget-73.html"

class="left postionrel">Union Budget And Other Economic Policies </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/forest-and-tribal-rights-61.html"

class="left postionrel">Forest and Tribal Rights </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-education-60.html"

class="left postionrel">Right to Education </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-food-59.html"

class="left postionrel">Right to Food </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/displacement-3279.html"

class="left postionrel">Displacement </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-work-mg-nrega-39.html"

class="left postionrel">Right to Work (MG-NREGA) </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/gender-3280.html"

class="left postionrel">GENDER </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-information-58.html"

class="left postionrel">Right to Information </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/social-audit-48.html"

class="left postionrel">Social Audit </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Hunger / HDI</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/poverty-and-inequality-20499.html"

class="left postionrel">Poverty and inequality </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/malnutrition-41.html"

class="left postionrel">Malnutrition </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/public-health-51.html"

class="left postionrel">Public Health </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/education-50.html"

class="left postionrel">Education </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/hunger-overview-40.html"

class="left postionrel">Hunger Overview </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/hdi-overview-45.html"

class="left postionrel">HDI Overview </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/pds-ration-food-security-42.html"

class="left postionrel">PDS/ Ration/ Food Security </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/sdgs-113.html"

class="left postionrel">SDGs </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/mid-day-meal-scheme-mdms-53.html"

class="left postionrel">Mid Day Meal Scheme (MDMS) </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Environment</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/time-bomb-ticking-52.html"

class="left postionrel">Time Bomb Ticking </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/water-and-sanitation-55.html"

class="left postionrel">Water and Sanitation </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/impact-on-agriculture-54.html"

class="left postionrel">Impact on Agriculture </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Law & Justice</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/social-justice-20500.html"

class="left postionrel">Social Justice </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/access-to-justice-47.html"

class="left postionrel">Access to Justice </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/human-rights-56.html"

class="left postionrel">Human Rights </a>

</p>

<p style="padding-left:5px;">