Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 150

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::index() - APP/Controller/ArtileDetailController.php, line 150

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 97

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 151

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::index() - APP/Controller/ArtileDetailController.php, line 151

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 97

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Warning (512): Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853 [CORE/src/Http/ResponseEmitter.php, line 48]

if (Configure::read('debug')) {

trigger_error($message, E_USER_WARNING);

} else {

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html>

<!--[if lt IE 7 ]>

<html class="ie ie6" lang='en'> <![endif]-->

<!--[if IE 7 ]>

<html class="ie ie7" lang='en'> <![endif]-->

<!--[if IE 8 ]>

<html class="ie ie8" lang='en'> <![endif]-->

<!--[if (gte IE 9)|!(IE)]><!-->

<html lang='en'>

<!--<![endif]-->

<head><meta http-equiv="Content-Type" content="text/html; charset=utf-8">

<title>

NEWS ALERTS | Declining bank credit indicates poor economic performance </title>

<meta name="description" content="

Apart from gross domestic product (GDP) and gross value added (GVA), another indicator which shows whether an economy is thriving or stagnating is the growth in bank credit. Credit is a critical input in the production of goods and services...."/>

<meta name="keywords" content="Economic Growth,Gross Value Added (GVA),GDP estimates,GDP growth,GDP growth rate,Farm Loans,Rural Credit,Farm Credit"/>

<meta name="news_keywords" content="Economic Growth,Gross Value Added (GVA),GDP estimates,GDP growth,GDP growth rate,Farm Loans,Rural Credit,Farm Credit">

<link rel="alternate" type="application/rss+xml" title="ROR" href="/ror.xml"/>

<link rel="alternate" type="application/rss+xml" title="RSS 2.0" href="/feeds/"/>

<link rel="stylesheet" href="/css/bootstrap.min.css?1697864993"/> <link rel="stylesheet" href="/css/style.css?v=1.1.2"/> <link rel="stylesheet" href="/css/style-inner.css?1577045210"/> <link rel="stylesheet" id="Oswald-css"

href="https://fonts.googleapis.com/css?family=Oswald%3Aregular%2C700&ver=3.8.1" type="text/css"

media="all">

<link rel="stylesheet" href="/css/jquery.modal.min.css?1578285302"/> <script src="/js/jquery-1.10.2.js?1575549704"></script> <script src="/js/jquery-migrate.min.js?1575549704"></script> <link rel="shortcut icon" href="/favicon.ico" title="Favicon">

<link rel="stylesheet" href="/css/jquery-ui.css?1580720609"/> <script src="/js/jquery-ui.js?1575549704"></script> <link rel="preload" as="style" href="https://www.im4change.org/css/custom.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery.modal.min.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery-ui.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/li-scroller.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<!-- <link rel="preload" as="style" href="https://www.im4change.org/css/style.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous"> -->

<link rel="preload" as="style" href="https://www.im4change.org/css/style-inner.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel='dns-prefetch' href="//im4change.org/css/custom.css" crossorigin >

<link rel="preload" as="script" href="https://www.im4change.org/js/bootstrap.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.li-scroller.1.0.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.modal.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.ui.totop.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-1.10.2.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-migrate.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-ui.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/setting.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/tie-scripts.js">

<!--[if IE]>

<script type="text/javascript">jQuery(document).ready(function () {

jQuery(".menu-item").has("ul").children("a").attr("aria-haspopup", "true");

});</script>

<![endif]-->

<!--[if lt IE 9]>

<script src="/js/html5.js"></script>

<script src="/js/selectivizr-min.js"></script>

<![endif]-->

<!--[if IE 8]>

<link rel="stylesheet" type="text/css" media="all" href="/css/ie8.css"/>

<![endif]-->

<meta property="og:title" content="NEWS ALERTS | Declining bank credit indicates poor economic performance" />

<meta property="og:url" content="https://im4change.in/news-alerts-57/declining-bank-credit-indicates-poor-economic-performance-4682277.html" />

<meta property="og:type" content="article" />

<meta property="og:description" content="

Apart from gross domestic product (GDP) and gross value added (GVA), another indicator which shows whether an economy is thriving or stagnating is the growth in bank credit. Credit is a critical input in the production of goods and services...." />

<meta property="og:image" content="" />

<meta property="fb:app_id" content="0" />

<meta name="viewport" content="width=device-width, initial-scale=1, maximum-scale=1, user-scalable=no">

<link rel="apple-touch-icon-precomposed" sizes="144x144" href="https://im4change.in/images/apple1.png">

<link rel="apple-touch-icon-precomposed" sizes="120x120" href="https://im4change.in/images/apple2.png">

<link rel="apple-touch-icon-precomposed" sizes="72x72" href="https://im4change.in/images/apple3.png">

<link rel="apple-touch-icon-precomposed" href="https://im4change.in/images/apple4.png">

<style>

.gsc-results-wrapper-overlay{

top: 38% !important;

height: 50% !important;

}

.gsc-search-button-v2{

border-color: #035588 !important;

background-color: #035588 !important;

}

.gsib_a{

height: 30px !important;

padding: 2px 8px 1px 6px !important;

}

.gsc-search-button-v2{

height: 41px !important;

}

input.gsc-input{

background: none !important;

}

@media only screen and (max-width: 600px) {

.gsc-results-wrapper-overlay{

top: 11% !important;

width: 87% !important;

left: 9% !important;

height: 43% !important;

}

.gsc-search-button-v2{

padding: 10px 10px !important;

}

.gsc-input-box{

height: 28px !important;

}

/* .gsib_a {

padding: 0px 9px 4px 9px !important;

}*/

}

@media only screen and (min-width: 1200px) and (max-width: 1920px) {

table.gsc-search-box{

width: 15% !important;

float: right !important;

margin-top: -118px !important;

}

.gsc-search-button-v2 {

padding: 6px !important;

}

}

</style>

<script>

$(function () {

$("#accordion").accordion({

event: "click hoverintent"

});

});

/*

* hoverIntent | Copyright 2011 Brian Cherne

* http://cherne.net/brian/resources/jquery.hoverIntent.html

* modified by the jQuery UI team

*/

$.event.special.hoverintent = {

setup: function () {

$(this).bind("mouseover", jQuery.event.special.hoverintent.handler);

},

teardown: function () {

$(this).unbind("mouseover", jQuery.event.special.hoverintent.handler);

},

handler: function (event) {

var currentX, currentY, timeout,

args = arguments,

target = $(event.target),

previousX = event.pageX,

previousY = event.pageY;

function track(event) {

currentX = event.pageX;

currentY = event.pageY;

}

;

function clear() {

target

.unbind("mousemove", track)

.unbind("mouseout", clear);

clearTimeout(timeout);

}

function handler() {

var prop,

orig = event;

if ((Math.abs(previousX - currentX) +

Math.abs(previousY - currentY)) < 7) {

clear();

event = $.Event("hoverintent");

for (prop in orig) {

if (!(prop in event)) {

event[prop] = orig[prop];

}

}

// Prevent accessing the original event since the new event

// is fired asynchronously and the old event is no longer

// usable (#6028)

delete event.originalEvent;

target.trigger(event);

} else {

previousX = currentX;

previousY = currentY;

timeout = setTimeout(handler, 100);

}

}

timeout = setTimeout(handler, 100);

target.bind({

mousemove: track,

mouseout: clear

});

}

};

</script>

<script type="text/javascript">

var _gaq = _gaq || [];

_gaq.push(['_setAccount', 'UA-472075-3']);

_gaq.push(['_trackPageview']);

(function () {

var ga = document.createElement('script');

ga.type = 'text/javascript';

ga.async = true;

ga.src = ('https:' == document.location.protocol ? 'https://ssl' : 'http://www') + '.google-analytics.com/ga.js';

var s = document.getElementsByTagName('script')[0];

s.parentNode.insertBefore(ga, s);

})();

</script>

<link rel="stylesheet" href="/css/custom.css?v=1.16"/> <script src="/js/jquery.ui.totop.js?1575549704"></script> <script src="/js/setting.js?1575549704"></script> <link rel="manifest" href="/manifest.json">

<meta name="theme-color" content="#616163" />

<meta name="apple-mobile-web-app-capable" content="yes">

<meta name="apple-mobile-web-app-status-bar-style" content="black">

<meta name="apple-mobile-web-app-title" content="im4change">

<link rel="apple-touch-icon" href="/icons/logo-192x192.png">

</head>

<body id="top" class="home inner blog">

<div class="background-cover"></div>

<div class="wrapper animated">

<header id="theme-header" class="header_inner" style="position: relative;">

<div class="logo inner_logo" style="left:20px !important">

<a title="Home" href="https://im4change.in/">

<img src="https://im4change.in/images/logo2.jpg?1582080632" class="logo_image" alt="im4change"/> </a>

</div>

<div class="langhindi" style="color: #000;display:none;"

href="https://im4change.in/">

<a class="more-link" href="https://im4change.in/">Home</a>

<a href="https://im4change.in/hindi/" class="langbutton ">हिन्दी</a>

</div>

<nav class="fade-in animated2" id="main-nav">

<div class="container">

<div class="main-menu">

<ul class="menu" id="menu-main">

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children"

style="left: -40px;"><a

target="_blank" href="https://im4change.in/">Home</a>

</li>

<li class="menu-item mega-menu menu-item-type-taxonomy mega-menu menu-item-object-category mega-menu menu-item-has-children parent-list"

style=" margin-left: -40px;"><a href="#">KNOWLEDGE GATEWAY <span class="sub-indicator"></span>

</a>

<div class="mega-menu-block background_menu" style="padding-top:25px;">

<div class="container">

<div class="mega-menu-content">

<div class="mega-menu-item">

<h3><b>Farm Crisis</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/farmers039-suicides-14.html"

class="left postionrel">Farm Suicides </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/unemployment-30.html"

class="left postionrel">Unemployment </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/rural-distress-70.html"

class="left postionrel">Rural distress </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/migration-34.html"

class="left postionrel">Migration </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/key-facts-72.html"

class="left postionrel">Key Facts </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/debt-trap-15.html"

class="left postionrel">Debt Trap </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Empowerment</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/union-budget-73.html"

class="left postionrel">Union Budget And Other Economic Policies </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/forest-and-tribal-rights-61.html"

class="left postionrel">Forest and Tribal Rights </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-education-60.html"

class="left postionrel">Right to Education </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-food-59.html"

class="left postionrel">Right to Food </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/displacement-3279.html"

class="left postionrel">Displacement </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-work-mg-nrega-39.html"

class="left postionrel">Right to Work (MG-NREGA) </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/gender-3280.html"

class="left postionrel">GENDER </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-information-58.html"

class="left postionrel">Right to Information </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/social-audit-48.html"

class="left postionrel">Social Audit </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Hunger / HDI</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/poverty-and-inequality-20499.html"

class="left postionrel">Poverty and inequality </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/malnutrition-41.html"

class="left postionrel">Malnutrition </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/public-health-51.html"

class="left postionrel">Public Health </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/education-50.html"

class="left postionrel">Education </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/hunger-overview-40.html"

class="left postionrel">Hunger Overview </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/hdi-overview-45.html"

class="left postionrel">HDI Overview </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/pds-ration-food-security-42.html"

class="left postionrel">PDS/ Ration/ Food Security </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/sdgs-113.html"

class="left postionrel">SDGs </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/mid-day-meal-scheme-mdms-53.html"

class="left postionrel">Mid Day Meal Scheme (MDMS) </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Environment</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/time-bomb-ticking-52.html"

class="left postionrel">Time Bomb Ticking </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/water-and-sanitation-55.html"

class="left postionrel">Water and Sanitation </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/impact-on-agriculture-54.html"

class="left postionrel">Impact on Agriculture </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Law & Justice</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/social-justice-20500.html"

class="left postionrel">Social Justice </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/access-to-justice-47.html"

class="left postionrel">Access to Justice </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/human-rights-56.html"

class="left postionrel">Human Rights </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/corruption-35.html"

class="left postionrel">Corruption </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/general-insecurity-46.html"

class="left postionrel">General Insecurity </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/disaster-relief-49.html"

class="left postionrel">Disaster & Relief </a>

</p>

</div>

</div>

</div>

</div>

</li>

<li class="menu-item menu-item-type-post_type menu-item-object-page "><a target="_blank" href="https://im4change.in/nceus_reports.php">NCEUS reports</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children parent-list ">

<a target="_blank" href="https://im4change.in/about-us-9.html">About Us <span

class="sub-indicator"></span></a>

<ul class="sub-menu aboutmenu">

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/objectives-8.html">Objectives</a>

</li>

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/contactus.php">Contact

Us</a></li>

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/about-us-9.html">About

Us</a></li>

</ul>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children ">

<a target="_blank" href="https://im4change.in/fellowships.php" title="Fellowships">Fellowships</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/media-workshops.php">Workshops</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/research.php">Research</a></li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/links-64">Partners</a></li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children"

id="menu-item-539"><a target="_blank" href="https://im4change.in/hindi/"

class="langbutton langlinkfont17">हिन्दी</a></li>

</ul>

</div> </div>

<!-- <div style="float: right;">

<script async src="https://cse.google.com/cse.js?cx=18b4f2e0f11bed3dd"></script>

<div class="gcse-search"></div>

</div> -->

<div class="search-block" style=" margin-left: 8px; margin-right: 7px;">

<form method="get" id="searchform" name="searchform"

action="https://im4change.in/search"

onsubmit="return searchvalidate();">

<button class="search-button" type="submit" value="Search"></button>

<input type="text" id="s" name="qryStr" value=""

onfocus="if (this.value == 'Search...') {this.value = '';}"

onblur="if (this.value == '') {this.value = 'Search...';}">

</form>

</div>

</nav>

</header>

<div class="container">

<div id="main-content" class=" main1 container fade-in animated3 sidebar-narrow-left">

<div class="content-wrap">

<div class="content" style="width: 900px;min-height: 500px;">

<div class="background_inner innBack" align="center">

<img src="https://im4change.in/images/media/im4change_80Bank_credit_image.jpg"

alt="Declining bank credit indicates poor economic performance"

class="box_shadow mt5 imgRes" style="max-width:500px;"/>

</div>

<section class="cat-box recent-box innerCatRecent">

<h1 class="cat-box-title">Declining bank credit indicates poor economic performance</h1>

<a href="JavaScript:void(0);" onclick="return shareArticle(34174);">

<img src="https://im4change.in/images/email.png?1582080630" border="0" width="24" align="right" alt="Share this article"/> </a>

<a href="https://im4change.in/news-alerts-57/declining-bank-credit-indicates-poor-economic-performance-4682277/print"

rel="nofollow">

<img src="https://im4change.in/images/icon-print.png?1582080630" border="0" width="24" align="right" alt="Share this article"/>

</a>

</section>

<section class="recent-box innerCatRecent">

<small class="pb-1"><span class="dateIcn">

<img src="https://im4change.in/images/published.svg?1582080666" alt="published"/>

Published on</span><span class="text-date"> Jul 10, 2017</span>

<span

class="dateIcn">

<img src="https://im4change.in/images/modified.svg?1582080666" alt="modified"/> Modified on </span><span class="text-date"> Jul 10, 2017</span>

</small>

</section>

<div class="clear"></div>

<div style="padding-top: 10px;">

<div class="innerLineHeight">

<div class="middleContent innerInput news-alerts-57">

<table>

<tr>

<td>

<div>

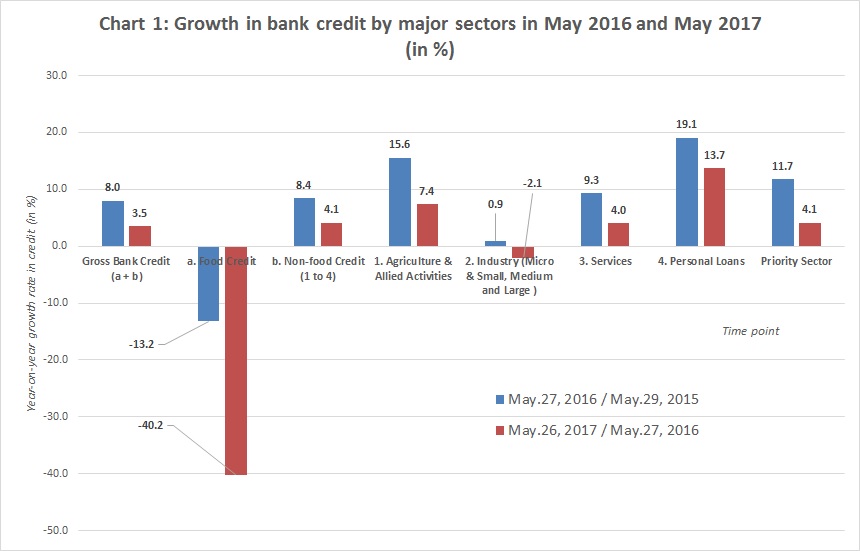

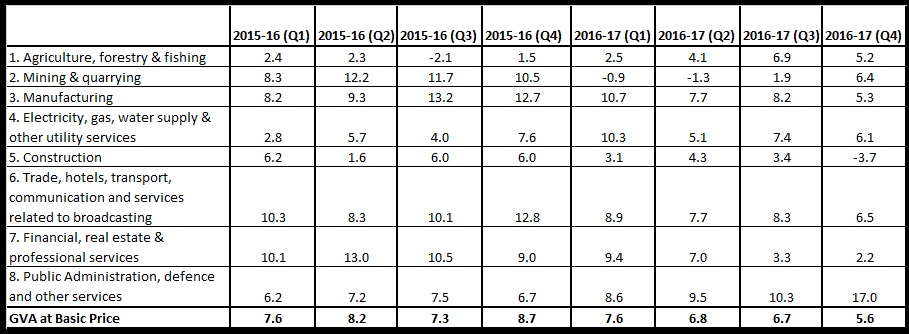

<br /><div align="justify">Apart from gross domestic product (GDP) and gross value added (GVA), another indicator which shows whether an economy is thriving or stagnating is the growth in bank credit. Credit is a critical input in the production of goods and services. It is generally the case that during prosperous times, economic actors, who are engaged in different sectors or in various industry, take up bank loans to invest. <br /><br />The <a href="http://rbidocs.rbi.org.in/rdocs/content/docs/PR3544SD30062017.xlsx" title="http://rbidocs.rbi.org.in/rdocs/content/docs/PR3544SD30062017.xlsx">provisional data</a> provided along with a <a href="https://im4change.in/siteadmin/tinymce/uploaded/Sectoral%20Deployment%20of%20Bank%20Credit.pdf" title="https://im4change.in/siteadmin/tinymce/uploaded/Sectoral%20Deployment%20of%20Bank%20Credit.pdf">press release</a> from the Reserve Bank of India (RBI) dated 30 June, 2017 reveals that in the fortnight ended 26 May, 2017, the year-on-year gross bank credit grew by just 3.5 percent. However, in the fortnight ended 27 May, 2016, the year-on-year growth rate in gross bank credit was at a much higher level i.e. 8.0 percent. Please see chart-1. <br /><br />Therefore, a falling growth in bank credit may imply that the Indian economy is not doing well in recent times. <br /><br /><img src="https://im4change.in/siteadmin/tinymce/uploaded/Chart%201%20Growth%20in%20bank%20credit%20by%20major%20sectors%20in%20May%202016%20&%20May%202017.jpg" alt="Chart 1 Growth in bank credit by major sectors in May 2016 & May 2017" width="349" height="223" /><br /><br /></div><div align="justify"><em><strong>Source: </strong>Deployment of gross bank credit by major sectors and major industries, dated 30 June, 2017, Reserve Bank of India, please <a href="http://rbidocs.rbi.org.in/rdocs/content/docs/PR3544SD30062017.xlsx" title="http://rbidocs.rbi.org.in/rdocs/content/docs/PR3544SD30062017.xlsx">click here</a> to access the data</em> </div><div align="justify"> </div><div align="justify">Interestingly, the Weekly Statistical Supplement - Extract (available at <a href="https://rbi.org.in/Scripts/BS_viewWssExtract.aspx" title="https://rbi.org.in/Scripts/BS_viewWssExtract.aspx">https://rbi.org.in/Scripts/BS_viewWssExtract.aspx</a>) from the Reserve Bank of India shows that in the fortnight ended 26 May, 2017, the year-on-year aggregate deposits increased by 10.9 percent. In the fortnight ended 27 May, 2016, the year-on-year growth rate in aggregate deposits was 8.9 percent.<br /><br />Based on the data provided by the Weekly Statistical Supplement – Extract, the Inclusive Media for Change team has calculated that the credit-to-deposit (CD) ratio of the banking system, or the proportion of deposits deployed as loans, fell from 75.83 percent in the fortnight ended 27 May, 2016 to 71.97 percent in the fortnight ended 26 May, 2017. The same source shows that the credit-to-deposit (CD) ratio of the banking system stood at 72.26 percent in the fortnight ended 23 June, 2017.<br /><br /><strong>Bank credit to agriculture</strong><br /><br />The <a href="https://im4change.in/siteadmin/tinymce/uploaded/Sectoral%20Deployment%20of%20Bank%20Credit.pdf" title="https://im4change.in/siteadmin/tinymce/uploaded/Sectoral%20Deployment%20of%20Bank%20Credit.pdf">press release</a> from the RBI dated 30 June, 2017, among other things, says the following:<br /><br />* Credit to agriculture and allied activities increased by 7.4 percent in May 2017, lower than the increase of 15.6 percent in May 2016.<br /><br />* Credit to industry contracted by 2.1 percent in May 2017 in contrast with an increase of 0.9 percent in May 2016.<br /><br />* Credit to the services sector increased by 4.0 percent in May 2017, lower than the increase of 9.3 percent in May 2016.<br /><br />* Personal loans increased by 13.7 percent in May 2017, lower than the increase of 19.1 percent in May 2016.<br /><br />When the Inclusive Media for Change sifted through the provisional RBI data, it was observed that the year-on-year growth rate in priority sector lending fell from 11.7 percent in the fortnight ended 27 May, 2016 to 4.1 percent in the fortnight ended 26 May, 2017. Please see chart-1. <br /><br />It needs to be mentioned here that the gross bank credit has two components: food credit and non-food credit. As compared to food credit, the share of non-food credit in gross bank credit is significantly higher. For example, in the fortnight ended 26 May, 2017, the share of non-food credit in gross bank credit was 99.22 percent, while that of food credit was just 0.78 percent.<br /><br />Credit to agriculture and allied activities, industry (micro & small, medium and large) and services along with personal loans add together to give total non-food credit. <br /><br />Priority sector lending, however, is different from non-food credit, under which loans are distributed to various sectors like agriculture & allied activities, micro & small enterprises, manufacturing, services, housing, micro-credit, education loans, state-sponsored organisations for SC/ ST, weaker sections and export credit. <br /><br />While the growth rate in credit to agriculture and allied activities (under non-food credit) fell from 15.6 percent to 7.4 percent between May 2016 and May 2017, growth rate in credit to agriculture and allied activities (under priority sector lending) reduced from 15.6 percent to 7.2 percent during the same period.<br /><br />The share of agriculture and allied activities in total non-food credit stood at 14.15 percent, whereas that of industry (micro & small, medium and large) remained at 38.2 percent in the fortnight ended 26 May, 2017. It shows that the credit flow to industrial sector is much higher as compared to the agrarian sector.<br /><br /><strong>Economic growth</strong> <br /><br />The <a href="https://im4change.in/siteadmin/tinymce/uploaded/Provisional%20estimates%20of%20annual%20national%20income%202016-17%20dated%2031%20May%202017.pdf" title="https://im4change.in/siteadmin/tinymce/uploaded/Provisional%20estimates%20of%20annual%20national%20income%202016-17%20dated%2031%20May%202017.pdf">provisional estimates</a> from the Central Statistics Office (CSO), which was released on 31 May, 2017, indicate that despite an increase in cash deposits with the banks due to the note ban that was imposed between November and December last year, the growth rate in real Gross Value Added (GVA) at basic price pertaining to the 'financial, real estate & professional services' sector is likely to reduce from 10.8 percent to 5.7 percent between 2015-16 and 2016-17. <br /><br />It is also estimated that in India the growth in real GVA at basic price <em>(i.e. increase in GVA after neutralizing the effect of price inflation)</em> will slow down from 7.9 percent to 6.6 percent between 2015-16 and 2016-17.<br /><br /><strong>Table 1: Growth in GVA at basic price (at 2011-12 prices) during various quarters of 2015-16 & 2016-17 (percentage change over previous year)</strong><br /><br /><img src="https://im4change.in/siteadmin/tinymce/uploaded/Table%201%20Real%20GVA%20growth%20in%20various%20quarters_1.jpg" alt="Table 1 Real GVA growth in various quarters" width="308" height="113" /><br /><br /><em><strong>Source: </strong>Press note on provisional estimates of annual national income 2016-17 and quarterly estimates of GDP for the fourth quarter (Q4) of 2016-17, Central Statistics Office, MoSPI, dated 31 May 2017, please <a href="https://im4change.in/siteadmin/tinymce/uploaded/Provisional%20estimates%20of%20annual%20national%20income%202016-17%20dated%2031%20May%202017.pdf" title="Press note on provisional estimates of annual national income 2016-17 and quarterly estimates of GDP for the fourth quarter of 2016-17" title="https://im4change.in/siteadmin/tinymce/uploaded/Provisional%20estimates%20of%20annual%20national%20income%202016-17%20dated%2031%20May%202017.pdf" title="Press note on provisional estimates of annual national income 2016-17 and quarterly estimates of GDP for the fourth quarter of 2016-17">click here</a> to access</em><br /><br />The growth rate in real GVA at basic price pertaining to the 'financial, real estate & professional services' sector, is expected to fall steadily over the four quarters of 2016-17 (i.e. from 9.4 percent in Q1 to 2.2 percent in Q4 of 2016-17). Please see table-1. <br /><br />Some economists believe that slackening of demand for bank loans and growing portfolio of bad loans with the banks, among other things, could have caused slow growth of the banking and finance sector. </div><div align="justify"> </div><div align="justify">There are others, however, who say that credit growth has not remained subdued <em>(since demonetisation) </em>because Indian firms now rely on other sources of funds like foreign direct investment (FDI), commercial papers, external commercial borrowings (ECBs), equity, non-bank financial institutions etc. <br /><br />It must be noted that GVA is the difference between GDP and net indirect taxes. In order to know more about the concept of GVA, please <a href="http://arthapedia.in/index.php?title=Gross_Value_Added_(GVA)_at_basic_prices_and_GVA_at_Factor_Costs" title="http://arthapedia.in/index.php?title=Gross_Value_Added_(GVA)_at_basic_prices_and_GVA_at_Factor_Costs">click here</a>.<br /></div><div align="justify"> </div><div align="justify"><br /><strong><em>References:</em></strong> <br /><br />Sectoral deployment of bank credit - May 2017, dated 30 June, 2017, Reserve Bank of India, please <a href="https://im4change.in/siteadmin/tinymce/uploaded/Sectoral%20Deployment%20of%20Bank%20Credit.pdf" title="Sectoral deployment of bank credit" title="https://im4change.in/siteadmin/tinymce/uploaded/Sectoral%20Deployment%20of%20Bank%20Credit.pdf" title="Sectoral deployment of bank credit">click here</a> to access <br /><br />Deployment of gross bank credit by major sectors and major industries, dated 30 June, 2017, Reserve Bank of India, please <a href="http://rbidocs.rbi.org.in/rdocs/content/docs/PR3544SD30062017.xlsx" title="http://rbidocs.rbi.org.in/rdocs/content/docs/PR3544SD30062017.xlsx">click here</a> to access the data<br /> <br />Press note on provisional estimates of annual national income 2016-17 and quarterly estimates of GDP for the fourth quarter (Q4) of 2016-17, Central Statistics Office, MoSPI, dated 31 May 2017, please <a href="https://im4change.in/siteadmin/tinymce/uploaded/Provisional%20estimates%20of%20annual%20national%20income%202016-17%20dated%2031%20May%202017.pdf" title="Press note on provisional estimates of annual national income 2016-17 and quarterly estimates of GDP for the fourth quarter of 2016-17" title="https://im4change.in/siteadmin/tinymce/uploaded/Provisional%20estimates%20of%20annual%20national%20income%202016-17%20dated%2031%20May%202017.pdf" title="Press note on provisional estimates of annual national income 2016-17 and quarterly estimates of GDP for the fourth quarter of 2016-17">click here</a> to access</div><div align="justify"><br />Bank credit grows at 6.02%, deposits at 11.19%: RBI data, PTI, Livemint.com, 21 June, 2017, please <a href="http://www.livemint.com/Industry/tuHMoPk14a2Su518sjY7DJ/Bank-credit-grows-at-602-deposits-at-1119-reveals-RBI.html" title="http://www.livemint.com/Industry/tuHMoPk14a2Su518sjY7DJ/Bank-credit-grows-at-602-deposits-at-1119-reveals-RBI.html">click here</a> to read more</div><div align="justify"> </div><div align="justify">The decline and fall of bank credit -Aparna Iyer, Livemint.com, 24 March, 2017, please <a href="http://www.livemint.com/Money/7pV8tTRGhNeXl5pIBeAdqN/The-decline-and-fall-of-bank-credit.html" title="http://www.livemint.com/Money/7pV8tTRGhNeXl5pIBeAdqN/The-decline-and-fall-of-bank-credit.html">click here</a> to access <br /></div><div align="justify"> </div><div align="justify">Is Credit Growth Really That Low In India? No, Says Nomura -Ira Dugal, BloombergQuint.com, 3 March, 2017, please <a href="https://www.bloombergquint.com/business/2017/03/03/is-credit-growth-really-that-low-in-india-no-says-nomura" title="https://www.bloombergquint.com/business/2017/03/03/is-credit-growth-really-that-low-in-india-no-says-nomura">click here</a> to access <br /></div><div align="justify"> </div><div align="justify"> </div><div align="justify"><strong>Image Courtesy: Inclusive Media for Change/ Shambhu Ghatak</strong> <br /></div>

</div>

</td>

</tr>

</table>

</div>

</div>

</div>

<div class="clear"></div>

<div style="padding-top: 18px;">

<p class="post-tag">Tagged with:

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Economic Growth"

title="Economic Growth">

Economic Growth </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Gross Value Added (GVA)"

title="Gross Value Added (GVA)">

Gross Value Added (GVA) </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=GDP estimates"

title="GDP estimates">

GDP estimates </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=GDP growth"

title="GDP growth">

GDP growth </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=GDP growth rate"

title="GDP growth rate">

GDP growth rate </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Farm Loans"

title="Farm Loans">

Farm Loans </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Rural Credit"

title="Rural Credit">

Rural Credit </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Farm Credit"

title="Farm Credit">

Farm Credit </a>

</p>

</div>

<div class="clear"></div>

<br><br>

<div class="widget-top">

<h4>Related Articles</h4>

<div class="stripe-line"></div>

</div>

<div class="widget-container">

<ul id="recentcomments">

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/oct-dec-quarter-gdp-slows-to-4-4-as-manufacturing-shrinks-tanya-krishna.html"

title="Oct-Dec Quarter GDP slows to 4.4% as manufacturing shrinks - Tanya Krishna ">

Oct-Dec Quarter GDP slows to 4.4% as manufacturing shrinks - Tanya Krishna </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/despite-insipid-manufacturing-show-india-s-gdp-to-grow-7-this-fiscal-nso-vikas-dhoot.html"

title="Despite insipid manufacturing show, India’s GDP to grow 7% this fiscal: NSO -Vikas Dhoot">

Despite insipid manufacturing show, India’s GDP to grow 7% this fiscal: NSO -Vikas Dhoot </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/can-india-s-production-incentive-scheme-transform-the-economy-as-the-sez-push-did-for-china-siddhant-bajpai.html"

title="Can India’s production incentive scheme transform the economy as the SEZ push did for China? -Siddhant Bajpai">

Can India’s production incentive scheme transform the economy as the SEZ push did for China? -Siddhant Bajpai </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/number-theory-four-key-questions-that-will-matter-for-the-economy-in-2023-pavitra-kanagaraj-and-abhishek-jha.html"

title="Number Theory: Four key questions that will matter for the economy in 2023 -Pavitra Kanagaraj and Abhishek Jha">

Number Theory: Four key questions that will matter for the economy in 2023 -Pavitra Kanagaraj and Abhishek Jha </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/rural-distress-increased-sharply-as-farm-wages-fell-santosh-mehrotra.html"

title="Rural distress increased sharply as farm wages fell - Santosh Mehrotra">

Rural distress increased sharply as farm wages fell - Santosh Mehrotra </a>

</li>

</ul>

</div>

<div class="comment-respond" id="respond">

<a name="commentbox"> </a>

<h3 class="comment-reply-title" id="reply-title">Write Comments</h3>

<form method="post" accept-charset="utf-8" role="form" action="/news-alerts-57/declining-bank-credit-indicates-poor-economic-performance-4682277.html"><div style="display:none;"><input type="hidden" name="_method" value="POST"/></div> <form class="comment-form" id="commentform" method="post" action="#commentbox" onSubmit="return validate()"

name="cmtform">

<input type="hidden" name="cmttype" value="articlecmt"/>

<input type="hidden" name="article_id" value="34174"/>

<p class="comment-notes">Your email address will not be published. Required fields are marked <span

class="required">*</span></p>

<p class="comment-form-author">

<label for="commenterName">Name</label>

<span class="required">*</span>

<input type="text" aria-required="true" size="30"

value=""

name="commenterName" id="commenterName" required="true">

</p>

<p class="comment-form-email">

<label for="commenterEmail">Email</label> <span class="required">*</span>

<input aria-required="true" size="30" name="commenterEmail" id="commenterEmail" type="email"

value=""

required="true">

</p>

<p class="comment-form-contact">

<label for="commenterPh">Contact No.</label>

<input type="text" size="30"

value=""

name="commenterPh" id="commenterPh">

</p>

<p class="comment-form-comment">

<label for="comment">Comment</label>

<textarea aria-required="true" required="true" rows="8" cols="45" name="comment"

id="comment"></textarea>

</p>

<p class="comment-form-comment">

<label for="comment">Type the characters you see in the image below <span class="required">*</span><br><img

class="captchaImg"

src="https://im4change.in/securimage_show_art.php?tk=1643554722" alt="captcha"/>

</label>

</p>

<input type="text" name="vrcode" required="true"/>

<p class="form-submit" style="width: 200px;">

<input type="submit" value="Post Comment" id="submit" name="submit">

</p></form>

</div>

<style>

.ui-widget-content {

height: auto !important;

}

</style>

<div id="share-modal"></div>

<style>

.middleContent a{

background-color: rgba(108,172,228,.2);

}

.middleContent a:hover{

background-color: #418fde;

border-color: #418fde;

color: #000;

}

</style>

<script>

function shareArticle(article_id) {

var options = {

modal: true,

height: 'auto',

width: 600 + 'px'

};

$('#share-modal').html("");

$('#share-modal').load('https://im4change.in/share_article?article_id=' + article_id).dialog(options).dialog('open');

}

function postShare() {

var param = 'article_id=' + $("#article_id").val();

param = param + '&y_name=' + $("#y_name").val();

param = param + '&y_email=' + $("#y_email").val();

param = param + '&f_name=' + $("#f_name").val();

param = param + '&f_email=' + $("#f_email").val();

param = param + '&y_msg=' + $("#y_msg").val();

$.ajax({

type: "POST",

url: 'https://im4change.in/post_share_article',

data: param,

success: function (response) {

$('#share-modal').html("Thank You, Your message posted to ");

}

});

return false;

}

</script> </div>

</div>

<!-- Right Side Section Start -->

<!-- MAP Section START -->

<aside class="sidebar indexMarg">

<div class="ad-cell">

<a href="https://im4change.in/statemap.php" title="">

<img src="https://im4change.in/images/map_new_version.png?1582080666" alt="India State Map" class="indiamap" width="232" height="252"/> </a>

<div class="rightmapbox">

<div id="sideOne" class="docltitle"><a href="https://im4change.in/state-report/india/36" target="_blank">DOCUMENTS/

REPORTS</a></div>

<div id="sideTwo" class="statetitle"><a href="https://im4change.in/states.php"target="_blank">STATE DATA/

HDRs.</a></div>

</div>

<div class="widget widgePadTop"></div>

</div>

</aside>

<!-- MAP Section END -->

<aside class="sidebar sidePadbottom">

<div class="rightsmlbox1" >

<a href="https://im4change.in/knowledge_gateway" target="_blank" style="color: #035588;

font-size: 17px;">

KNOWLEDGE GATEWAY

</a>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title">

<a href="https://im4change.in/newsletter" target="_blank">

NEWSLETTER

</a>

</p>

</div>

</div>

<div class="rightsmlbox1" style="height: 325px;">

<div>

<p class="rightsmlbox1_title">

Interview with Prof. Ravi Srivastava

</p>

<p class="rightsmlbox1_title">

<a href="https://im4change.in/video/interview-with-prof-ravi-srivastava-on-current-economic-crisis">

<img width="250" height="200" src="/images/interview_video_home.jpg" alt="Interview with Prof. Ravi Srivastava"/>

</a>

<!--

<iframe width="250" height="200" src="https://www.youtube.com/embed/MmaTlntk-wc" frameborder="0" allow="accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture" allowfullscreen=""></iframe>-->

</p>

<a href="https://im4change.in/videogallery" class="more-link CatArchalAnch1" target="_blank">

More videos

</a>

</div>

</div>

<div class="rightsmlbox1">

<div>

<!--div id="sstory" class="rightboxicons"></div--->

<p class="rightsmlbox1_title"><a href="https://im4change.in/list-success-stories" target="_blank">Success Stories</a></p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a

href="https://im4change.in/interviews" target="_blank">Interviews</a>

</p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a href="https://www.commoncause.in/page.php?id=10" >Donate</a></p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a

href="https://im4change.in/marquee"

class="isf_link more-link" title="India Focus?" style="border: 4px solid #fdd922;width: 90%;background-color: #fdd922;text-align: center;color: #000000;font-size:18px" target="_blank">India Focus</a></p> </div>

</div>

<div class="rightsmlbox1" style="height: 104px !important;">

<a href="https://im4change.in/quarterly_reports.php" target="_blank">

Quarterly Reports on Effect of Economic Slowdown on Employment in India (2008 - 2015)

</a>

</div>

<!-- <div class="rightsmlbox1">

<a href="https://play.google.com/store/apps/details?id=com.im4.im4change" target="_blank">

</a></div> -->

<!-- <section class="cat-box recent-box secMarg">

<h2 class="cat-box-title">Most Visited</h2>

</section> -->

<!-- accordion Starts here -->

<!-- <div id="accordion" class="accordMarg">

</div> -->

<!-- accordion ends here -->

<!-- Widget Tag Cloud Starts here -->

<div id="tag_cloud-2" class="widget widget_tag_cloud">

<section class="cat-box recent-box secMarg">

<h2 class="cat-box-title">MOST VISITED TAGS</h2>

</section>

<div class="widget-top wiPdTp">

<div class="stripe-line"></div>

</div>

<div class="widget-container">

<div class="tagcloud">

<a href="https://im4change.in/search?qryStr=Agriculture"

target="_blank" class="tag-link-4 font4">Agriculture</a>

<a href="https://im4change.in/search?qryStr=Food Security"

target="_blank" class="tag-link-4 font4">Food Security</a>

<a href="https://im4change.in/search?qryStr=Law and Justice"

target="_blank" class="tag-link-4 font4">Law and Justice</a>

<a href="https://im4change.in/search?qryStr=Health"

target="_blank" class="tag-link-4 font4">Health</a>

<a href="https://im4change.in/search?qryStr=Right to Food"

target="_blank" class="tag-link-4 font4">Right to Food</a>

<a href="https://im4change.in/search?qryStr=Corruption"

target="_blank" class="tag-link-4 font4">Corruption</a>

<a href="https://im4change.in/search?qryStr=farming"

target="_blank" class="tag-link-4 font4">farming</a>

<a href="https://im4change.in/search?qryStr=Environment"

target="_blank" class="tag-link-4 font4">Environment</a>

<a href="https://im4change.in/search?qryStr=Right to Information"

target="_blank" class="tag-link-4 font4">Right to Information</a>

<a href="https://im4change.in/search?qryStr=NREGS"

target="_blank" class="tag-link-4 font4">NREGS</a>

<a href="https://im4change.in/search?qryStr=Human Rights"

target="_blank" class="tag-link-4 font4">Human Rights</a>

<a href="https://im4change.in/search?qryStr=Governance"

target="_blank" class="tag-link-4 font4">Governance</a>

<a href="https://im4change.in/search?qryStr=PDS"

target="_blank" class="tag-link-4 font4">PDS</a>

<a href="https://im4change.in/search?qryStr=COVID-19"

target="_blank" class="tag-link-4 font4">COVID-19</a>

<a href="https://im4change.in/search?qryStr=Land Acquisition"

target="_blank" class="tag-link-4 font4">Land Acquisition</a>

<a href="https://im4change.in/search?qryStr=mgnrega"

target="_blank" class="tag-link-4 font4">mgnrega</a>

<a href="https://im4change.in/search?qryStr=Farmers"

target="_blank" class="tag-link-4 font4">Farmers</a>

<a href="https://im4change.in/search?qryStr=transparency"

target="_blank" class="tag-link-4 font4">transparency</a>

<a href="https://im4change.in/search?qryStr=Gender"

target="_blank" class="tag-link-4 font4">Gender</a>

<a href="https://im4change.in/search?qryStr=Poverty"

target="_blank" class="tag-link-4 font4">Poverty</a>

<a href="https://im4change.in/search?qryStr=Farm Laws" target="_blank" class="tag-link-4 font4">Farm Laws

</a>

<a href="https://im4change.in/search?qryStr=Citizenship Amendment Act" target="_blank" class="tag-link-4 font4">Citizenship Amendment Act

</a>

<a href="https://im4change.in/search?qryStr=CAA NPR NRIC" target="_blank" class="tag-link-4 font4">CAA NPR NRIC

</a>

<a href="https://im4change.in/search?qryStr=Job Losses" target="_blank" class="tag-link-4 font4">Job Losses

</a>

<a href="https://im4change.in/search?qryStr=Migrant Workers" target="_blank" class="tag-link-4 font4">Migrant Workers

</a>

<a href="https://im4change.in/search?qryStr=Unemployment" target="_blank" class="tag-link-4 font4">Unemployment

</a>

<a href="https://im4change.in/search?qryStr=PMGKAY" target="_blank" class="tag-link-4 font4">PMGKAY

</a>

<a href="https://im4change.in/search?qryStr=PM-KISAN" target="_blank" class="tag-link-4 font4">PM-KISAN

</a>

<a href="https://im4change.in/search?qryStr=PM-CARES" target="_blank" class="tag-link-4 font4">PM-CARES

</a>

<a href="https://im4change.in/search?qryStr=LFPR" target="_blank" class="tag-link-4 font4">LFPR

</a>

</div>

</div>

</div>

<!-- Widget Tag Cloud Ends here -->

</aside>

<!-- Right Side Section End -->

</div>

<section class="cat-box cats-review-box footerSec">

<h2 class="cat-box-title vSec CatArcha">Video

Archives</h2>

<h2 class="cat-box-title CatArchaTitle">Archives</h2>

<div class="cat-box-content">

<div class="reviews-cat">

<div class="CatArchaDiv1">

<div class="CatArchaDiv2">

<ul>

<li>

<a href="https://im4change.in/news-alerts-57/moving-upstream-luni-fellowship.html" target="_blank">

Moving Upstream: Luni – Fellowship </a>

</li>

<li>

<a href="https://im4change.in/news-alerts-57/135-million-indians-exited-multidimensional-poverty-as-per-government-figures-is-that-the-same-as-poverty-reduction.html" target="_blank">

135 Million Indians Exited “Multidimensional" Poverty as per Government... </a>

</li>

<li>

<a href="https://im4change.in/news-alerts-57/explainer-why-are-tomato-prices-on-fire.html" target="_blank">

Explainer: Why are Tomato Prices on Fire? </a>

</li>

<li>

<a href="https://im4change.in/news-alerts-57/nsso-survey-only-39-1-of-all-households-have-drinking-water-within-dwelling-46-7-of-rural-households-use-firewood-for-cooking.html" target="_blank">

NSSO Survey: Only 39.1% of all Households have Drinking... </a>

</li>

<li class="CatArchalLi1">

<a href="https://im4change.in/news-alerts-57"

class="more-link CatArchalAnch1" target="_blank">

More...

</a>

</li>

</ul>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/I51LYnP8BOk/1.jpg"

alt=" Im4Change.org हिंदी वेबसाइट का परिचय. Short Video on im4change.org...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Short-Video-on-im4change-Hindi-website-Inclusive-Media-for-Change" target="_blank">

Im4Change.org हिंदी वेबसाइट का परिचय. Short Video on im4change.org... </a>

</p>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/kNqha-SwfIY/1.jpg"

alt=" "Session 1: Scope of IDEA and AgriStack" in Exploring...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Session-1- Scope-of-IDEA-and-AgriStack-in-Exploring-Digitalisation-in-Agriculture-29-April-2022" target="_blank">

"Session 1: Scope of IDEA and AgriStack" in Exploring... </a>

</p>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/6kIVjlgZItk/1.jpg"

alt=" "Session 2: Farmer Centric Digitalisation in Agriculture" in Exploring...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Session-2-Farmer-Centric-Digitalisation-in-Agriculture-in-Exploring-Digitalisation-in-Agriculture-29-April-2022" target="_blank">

"Session 2: Farmer Centric Digitalisation in Agriculture" in Exploring... </a>

</p>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/2BeHTu0y7xc/1.jpg"

alt=" "Session 3: Future of Digitalisation in Agriculture" in Exploring...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Session-3-Future-of-Digitalisation-in-Agriculture-in-Exploring-Digitalisation-in-Agriculture-29-April-2022" target="_blank">

"Session 3: Future of Digitalisation in Agriculture" in Exploring... </a>

</p>

</div>

<div class="divWidth">

<ul class="divWidthMarg">

<li>

<a href="https://im4change.in/video/Public-Spending-on-Agriculture-in-India-Source-Foundation-for-Agrarian-Studies"

title="Public Spending on Agriculture in India (Source: Foundation for Agrarian Studies)" target="_blank">

Public Spending on Agriculture in India (Source: Foundation for...</a>

</li>

<li>

<a href="https://im4change.in/video/Agrarian-Change-Seminar-Protests-against-the-New-Farm-Laws-in-India-by-Prof-Vikas-Rawal-JNU-Source-Journal-Of-Agrarian-Change"

title="Agrarian Change Seminar: 'Protests against the New Farm Laws in India' by Prof. Vikas Rawal, JNU (Source: Journal Of Agrarian Change) " target="_blank">

Agrarian Change Seminar: 'Protests against the New Farm Laws...</a>

</li>

<li>

<a href="https://im4change.in/video/Webinar-Ramrao-The-Story-of-India-Farm-Crisis-Source-Azim-Premji-University"

title="Webinar: Ramrao - The Story of India's Farm Crisis (Source: Azim Premji University)" target="_blank">

Webinar: Ramrao - The Story of India's Farm Crisis...</a>

</li>

<li>

<a href="https://im4change.in/video/water-and-agricultural-transformation-in-India"

title="Water and Agricultural Transformation in India: A Symbiotic Relationship (Source: IGIDR)" target="_blank">

Water and Agricultural Transformation in India: A Symbiotic Relationship...</a>

</li>

<li class="CatArchalLi1">

<a href="https://im4change.in/videogallery"

class="more-link CatArchalAnch1" target="_blank">

More...

</a>

</li>

</ul>

</div>

</div>

</div>

</div>

</section> </div>

<div class="clear"></div>

<!-- Footer option Starts here -->

<div class="footer-bottom fade-in animated4">

<div class="container">

<div class="social-icons icon_flat">

<p class="SocialMargTop"> Website Developed by <a target="_blank" title="Web Development"

class="wot right"

href="http://www.ravinderkhurana.com/" rel="nofollow">

RAVINDErkHURANA.com</a></p>

</div>

<div class="alignleft">

<a

target="_blank" href="https://im4change.in/objectives-8.html"

class="link"

title="Objectives">Objectives</a> | <a

target="_blank" href="https://im4change.in/about-us-9.html"

class="link" title="About Us">About Us</a> | <a

target="_blank" href="https://im4change.in/media-workshops.php"

class="ucwords">Workshops</a> | <a

target="_blank" href="https://im4change.in/disclaimer/disclaimer-149.html"

title="Disclaimer">Disclaimer</a> </div>

</div>

</div>

<!-- Footer option ends here -->

</div>

<div id="connect">

<a target="_blank"

href="http://www.facebook.com/sharer.php?u=https://im4change.in/news-alerts-57/declining-bank-credit-indicates-poor-economic-performance-4682277.html"

title="Share on Facebook">

<img src="https://im4change.in/images/Facebook.png?1582080640" alt="share on Facebook" class="ImgBorder"/>

</a><br/>

<a target="_blank"

href="http://twitter.com/share?text=Im4change&url=https://im4change.in/news-alerts-57/declining-bank-credit-indicates-poor-economic-performance-4682277.html"

title="Share on Twitter">

<img src="https://im4change.in/images/twitter.png?1582080632" alt="Twitter" class="ImgBorder"/> </a>

<br/>

<a href="/feeds" title="RSS Feed" target="_blank">

<img src="https://im4change.in/images/rss.png?1582080632" alt="RSS" class="ImgBorder"/>

</a>

<br/>

<a class="feedback-link" id="feedbackFormLink" href="#">

<img src="https://im4change.in/images/feedback.png?1582080630" alt="Feedback" class="ImgBorder"/>

</a> <br/>

<a href="javascript:function iprl5(){var d=document,z=d.createElement('scr'+'ipt'),b=d.body,l=d.location;try{if(!b)throw(0);d.title='(Saving...) '+d.title;z.setAttribute('src',l.protocol+'//www.instapaper.com/j/WKrH3R7ORD5p?u='+encodeURIComponent(l.href)+'&t='+(new Date().getTime()));b.appendChild(z);}catch(e){alert('Please wait until the page has loaded.');}}iprl5();void(0)"

class="bookmarklet" onclick="return explain_bookmarklet();">

<img src="https://im4change.in/images/read-it-later.png?1582080632" alt="Read Later" class="ImgBorder"/> </a>

</div>

<!-- Feedback form Starts here -->

<div id="feedbackForm" class="overlay_form" class="ImgBorder">

<h2>Contact Form</h2>

<div id="contactform1">

<div id="formleft">

<form id="submitform" action="/contactus.php" method="post">

<input type="hidden" name="submitform" value="submitform"/>

<input type="hidden" name="salt_key" value="a0e0f2c6a0644a70e57ad2c96829709a"/>

<input type="hidden" name="ref" value="feedback"/>

<fieldset>

<label>Name :</label>

<input type="text" name="name" class="tbox" required/>

</fieldset>

<fieldset>

<label>Email :</label>

<input type="text" name="email" class="tbox" required/>

</fieldset>

<fieldset>

<label>Message :</label>

<textarea rows="5" cols="20" name="message" required></textarea>

</fieldset>

<fieldset>

Please enter security code

<div class="clear"></div>

<input type="text" name="vrcode" class="tbox"/>

</fieldset>

<fieldset>

<input type="submit" class="button" value="Submit"/>

<a href="#" id="closefeedbakcformLink">Close</a>

</fieldset>

</form>

</div>

<div class="clearfix"></div>

</div>

</div>

<div id="donate_popup" class="modal" style="max-width: 800px;">

<table width="100%" border="1">

<tr>

<td colspan="2" align="center">

<b>Support im4change</b>

</td>

</tr>

<tr>

<td width="25%" valign="middle">

<img src="https://im4change.in/images/logo2.jpg?1582080632" alt="" width="100%"/> </td>

<td style="padding-left:10px;padding-top:10px;">

<form action="https://im4change.in/donate" method="get">

<table width="100%" cellpadding="2" cellspacing="2">

<tr>

<td width="33%" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

10

</td>

<td width="33%" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

100

</td>

<td width="33%" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

1000

</td>

</tr>

<tr>

<td colspan="3">

</td>

</tr>

<tr>

<td style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

50

</td>

<td style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

500

</td>

<td style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

<input type="text" name="price" placeholder="?" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

</td>

</tr>

<tr>

<td colspan="3">

</td>

</tr>

<tr>

<td colspan="3" align="right">

<input type="button" name="Pay" value="Pay"

style="width: 200px;background-color: rgb(205, 35, 36);color: #ffffff;"/>

</td>

</tr>

</table>

</form>

</td>

</tr>

</table>

</div><script type='text/javascript'>

/* <![CDATA[ */

var tievar = {'go_to': 'Go to...'};

/* ]]> */

</script>

<script src="/js/tie-scripts.js?1575549704"></script><script src="/js/bootstrap.js?1575549704"></script><script src="/js/jquery.modal.min.js?1578284310"></script><script>

$(document).ready(function() {

// tell the autocomplete function to get its data from our php script

$('#s').autocomplete({

source: "/autocomplete"

});

});

</script>

<script src="/vj-main-sw-register.js" async></script>

<script>function init(){var imgDefer=document.getElementsByTagName('img');for(var i=0;i<imgDefer.length;i++){if(imgDefer[i].getAttribute('data-src')){imgDefer[i].setAttribute('src',imgDefer[i].getAttribute('data-src'))}}}

window.onload=init;</script>

</body>

</html>'

}

$maxBufferLength = (int) 8192

$file = '/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php'

$line = (int) 853

$message = 'Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853'

Cake\Http\ResponseEmitter::emit() - CORE/src/Http/ResponseEmitter.php, line 48

Cake\Http\Server::emit() - CORE/src/Http/Server.php, line 141

[main] - ROOT/webroot/index.php, line 39

Warning (2): Cannot modify header information - headers already sent by (output started at /home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php:853) [CORE/src/Http/ResponseEmitter.php, line 148]

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html>

<!--[if lt IE 7 ]>

<html class="ie ie6" lang='en'> <![endif]-->

<!--[if IE 7 ]>

<html class="ie ie7" lang='en'> <![endif]-->

<!--[if IE 8 ]>

<html class="ie ie8" lang='en'> <![endif]-->

<!--[if (gte IE 9)|!(IE)]><!-->

<html lang='en'>

<!--<![endif]-->

<head><meta http-equiv="Content-Type" content="text/html; charset=utf-8">

<title>

NEWS ALERTS | Declining bank credit indicates poor economic performance </title>

<meta name="description" content="

Apart from gross domestic product (GDP) and gross value added (GVA), another indicator which shows whether an economy is thriving or stagnating is the growth in bank credit. Credit is a critical input in the production of goods and services...."/>

<meta name="keywords" content="Economic Growth,Gross Value Added (GVA),GDP estimates,GDP growth,GDP growth rate,Farm Loans,Rural Credit,Farm Credit"/>

<meta name="news_keywords" content="Economic Growth,Gross Value Added (GVA),GDP estimates,GDP growth,GDP growth rate,Farm Loans,Rural Credit,Farm Credit">

<link rel="alternate" type="application/rss+xml" title="ROR" href="/ror.xml"/>

<link rel="alternate" type="application/rss+xml" title="RSS 2.0" href="/feeds/"/>

<link rel="stylesheet" href="/css/bootstrap.min.css?1697864993"/> <link rel="stylesheet" href="/css/style.css?v=1.1.2"/> <link rel="stylesheet" href="/css/style-inner.css?1577045210"/> <link rel="stylesheet" id="Oswald-css"

href="https://fonts.googleapis.com/css?family=Oswald%3Aregular%2C700&ver=3.8.1" type="text/css"

media="all">

<link rel="stylesheet" href="/css/jquery.modal.min.css?1578285302"/> <script src="/js/jquery-1.10.2.js?1575549704"></script> <script src="/js/jquery-migrate.min.js?1575549704"></script> <link rel="shortcut icon" href="/favicon.ico" title="Favicon">

<link rel="stylesheet" href="/css/jquery-ui.css?1580720609"/> <script src="/js/jquery-ui.js?1575549704"></script> <link rel="preload" as="style" href="https://www.im4change.org/css/custom.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery.modal.min.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery-ui.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/li-scroller.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<!-- <link rel="preload" as="style" href="https://www.im4change.org/css/style.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous"> -->

<link rel="preload" as="style" href="https://www.im4change.org/css/style-inner.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel='dns-prefetch' href="//im4change.org/css/custom.css" crossorigin >

<link rel="preload" as="script" href="https://www.im4change.org/js/bootstrap.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.li-scroller.1.0.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.modal.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.ui.totop.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-1.10.2.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-migrate.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-ui.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/setting.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/tie-scripts.js">

<!--[if IE]>

<script type="text/javascript">jQuery(document).ready(function () {

jQuery(".menu-item").has("ul").children("a").attr("aria-haspopup", "true");

});</script>

<![endif]-->

<!--[if lt IE 9]>

<script src="/js/html5.js"></script>

<script src="/js/selectivizr-min.js"></script>

<![endif]-->

<!--[if IE 8]>

<link rel="stylesheet" type="text/css" media="all" href="/css/ie8.css"/>

<![endif]-->

<meta property="og:title" content="NEWS ALERTS | Declining bank credit indicates poor economic performance" />

<meta property="og:url" content="https://im4change.in/news-alerts-57/declining-bank-credit-indicates-poor-economic-performance-4682277.html" />

<meta property="og:type" content="article" />

<meta property="og:description" content="

Apart from gross domestic product (GDP) and gross value added (GVA), another indicator which shows whether an economy is thriving or stagnating is the growth in bank credit. Credit is a critical input in the production of goods and services...." />

<meta property="og:image" content="" />

<meta property="fb:app_id" content="0" />

<meta name="viewport" content="width=device-width, initial-scale=1, maximum-scale=1, user-scalable=no">

<link rel="apple-touch-icon-precomposed" sizes="144x144" href="https://im4change.in/images/apple1.png">

<link rel="apple-touch-icon-precomposed" sizes="120x120" href="https://im4change.in/images/apple2.png">

<link rel="apple-touch-icon-precomposed" sizes="72x72" href="https://im4change.in/images/apple3.png">

<link rel="apple-touch-icon-precomposed" href="https://im4change.in/images/apple4.png">

<style>

.gsc-results-wrapper-overlay{

top: 38% !important;

height: 50% !important;

}

.gsc-search-button-v2{

border-color: #035588 !important;

background-color: #035588 !important;

}

.gsib_a{

height: 30px !important;

padding: 2px 8px 1px 6px !important;

}

.gsc-search-button-v2{

height: 41px !important;

}

input.gsc-input{

background: none !important;

}

@media only screen and (max-width: 600px) {

.gsc-results-wrapper-overlay{

top: 11% !important;

width: 87% !important;

left: 9% !important;

height: 43% !important;

}

.gsc-search-button-v2{

padding: 10px 10px !important;

}

.gsc-input-box{

height: 28px !important;

}

/* .gsib_a {

padding: 0px 9px 4px 9px !important;

}*/

}

@media only screen and (min-width: 1200px) and (max-width: 1920px) {

table.gsc-search-box{

width: 15% !important;

float: right !important;

margin-top: -118px !important;

}

.gsc-search-button-v2 {

padding: 6px !important;

}

}

</style>

<script>

$(function () {

$("#accordion").accordion({

event: "click hoverintent"

});

});

/*

* hoverIntent | Copyright 2011 Brian Cherne

* http://cherne.net/brian/resources/jquery.hoverIntent.html

* modified by the jQuery UI team

*/

$.event.special.hoverintent = {

setup: function () {

$(this).bind("mouseover", jQuery.event.special.hoverintent.handler);

},

teardown: function () {

$(this).unbind("mouseover", jQuery.event.special.hoverintent.handler);

},

handler: function (event) {

var currentX, currentY, timeout,

args = arguments,

target = $(event.target),

previousX = event.pageX,

previousY = event.pageY;

function track(event) {

currentX = event.pageX;

currentY = event.pageY;

}

;

function clear() {

target

.unbind("mousemove", track)

.unbind("mouseout", clear);

clearTimeout(timeout);

}

function handler() {

var prop,

orig = event;

if ((Math.abs(previousX - currentX) +

Math.abs(previousY - currentY)) < 7) {

clear();

event = $.Event("hoverintent");

for (prop in orig) {

if (!(prop in event)) {

event[prop] = orig[prop];

}

}

// Prevent accessing the original event since the new event

// is fired asynchronously and the old event is no longer

// usable (#6028)

delete event.originalEvent;

target.trigger(event);

} else {

previousX = currentX;

previousY = currentY;

timeout = setTimeout(handler, 100);

}

}

timeout = setTimeout(handler, 100);

target.bind({

mousemove: track,

mouseout: clear

});

}

};

</script>

<script type="text/javascript">

var _gaq = _gaq || [];

_gaq.push(['_setAccount', 'UA-472075-3']);

_gaq.push(['_trackPageview']);

(function () {

var ga = document.createElement('script');

ga.type = 'text/javascript';

ga.async = true;

ga.src = ('https:' == document.location.protocol ? 'https://ssl' : 'http://www') + '.google-analytics.com/ga.js';

var s = document.getElementsByTagName('script')[0];

s.parentNode.insertBefore(ga, s);

})();

</script>

<link rel="stylesheet" href="/css/custom.css?v=1.16"/> <script src="/js/jquery.ui.totop.js?1575549704"></script> <script src="/js/setting.js?1575549704"></script> <link rel="manifest" href="/manifest.json">

<meta name="theme-color" content="#616163" />

<meta name="apple-mobile-web-app-capable" content="yes">

<meta name="apple-mobile-web-app-status-bar-style" content="black">

<meta name="apple-mobile-web-app-title" content="im4change">

<link rel="apple-touch-icon" href="/icons/logo-192x192.png">

</head>

<body id="top" class="home inner blog">

<div class="background-cover"></div>

<div class="wrapper animated">

<header id="theme-header" class="header_inner" style="position: relative;">

<div class="logo inner_logo" style="left:20px !important">

<a title="Home" href="https://im4change.in/">

<img src="https://im4change.in/images/logo2.jpg?1582080632" class="logo_image" alt="im4change"/> </a>

</div>

<div class="langhindi" style="color: #000;display:none;"

href="https://im4change.in/">

<a class="more-link" href="https://im4change.in/">Home</a>

<a href="https://im4change.in/hindi/" class="langbutton ">हिन्दी</a>

</div>

<nav class="fade-in animated2" id="main-nav">

<div class="container">

<div class="main-menu">

<ul class="menu" id="menu-main">

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children"

style="left: -40px;"><a

target="_blank" href="https://im4change.in/">Home</a>

</li>

<li class="menu-item mega-menu menu-item-type-taxonomy mega-menu menu-item-object-category mega-menu menu-item-has-children parent-list"

style=" margin-left: -40px;"><a href="#">KNOWLEDGE GATEWAY <span class="sub-indicator"></span>

</a>

<div class="mega-menu-block background_menu" style="padding-top:25px;">

<div class="container">

<div class="mega-menu-content">

<div class="mega-menu-item">

<h3><b>Farm Crisis</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/farmers039-suicides-14.html"

class="left postionrel">Farm Suicides </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/unemployment-30.html"

class="left postionrel">Unemployment </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/rural-distress-70.html"

class="left postionrel">Rural distress </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/migration-34.html"

class="left postionrel">Migration </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/key-facts-72.html"

class="left postionrel">Key Facts </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/debt-trap-15.html"

class="left postionrel">Debt Trap </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Empowerment</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/union-budget-73.html"