Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 150

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::index() - APP/Controller/ArtileDetailController.php, line 150

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 97

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Deprecated (16384): The ArrayAccess methods will be removed in 4.0.0.Use getParam(), getData() and getQuery() instead. - /home/brlfuser/public_html/src/Controller/ArtileDetailController.php, line: 151

You can disable deprecation warnings by setting `Error.errorLevel` to `E_ALL & ~E_USER_DEPRECATED` in your config/app.php. [CORE/src/Core/functions.php, line 311]

deprecationWarning - CORE/src/Core/functions.php, line 311

Cake\Http\ServerRequest::offsetGet() - CORE/src/Http/ServerRequest.php, line 2421

App\Controller\ArtileDetailController::index() - APP/Controller/ArtileDetailController.php, line 151

Cake\Controller\Controller::invokeAction() - CORE/src/Controller/Controller.php, line 610

Cake\Http\ActionDispatcher::_invoke() - CORE/src/Http/ActionDispatcher.php, line 120

Cake\Http\ActionDispatcher::dispatch() - CORE/src/Http/ActionDispatcher.php, line 94

Cake\Http\BaseApplication::__invoke() - CORE/src/Http/BaseApplication.php, line 235

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\RoutingMiddleware::__invoke() - CORE/src/Routing/Middleware/RoutingMiddleware.php, line 162

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Routing\Middleware\AssetMiddleware::__invoke() - CORE/src/Routing/Middleware/AssetMiddleware.php, line 97

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Error\Middleware\ErrorHandlerMiddleware::__invoke() - CORE/src/Error/Middleware/ErrorHandlerMiddleware.php, line 96

Cake\Http\Runner::__invoke() - CORE/src/Http/Runner.php, line 65

Cake\Http\Runner::run() - CORE/src/Http/Runner.php, line 51

Cake\Http\Server::run() - CORE/src/Http/Server.php, line 98

Warning (512): Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853 [CORE/src/Http/ResponseEmitter.php, line 48]

if (Configure::read('debug')) {

trigger_error($message, E_USER_WARNING);

} else {

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html>

<!--[if lt IE 7 ]>

<html class="ie ie6" lang='en'> <![endif]-->

<!--[if IE 7 ]>

<html class="ie ie7" lang='en'> <![endif]-->

<!--[if IE 8 ]>

<html class="ie ie8" lang='en'> <![endif]-->

<!--[if (gte IE 9)|!(IE)]><!-->

<html lang='en'>

<!--<![endif]-->

<head><meta http-equiv="Content-Type" content="text/html; charset=utf-8">

<title>

NEWS ALERTS | No clear-cut trend in economy going cashless </title>

<meta name="description" content="

Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens’ Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being..."/>

<meta name="keywords" content="Digital Wallets,Digital India,Digital Payments,Electronic Banking Transactions,Electronic payment,Electronic payments,Cashless Economy,Mobile Banking"/>

<meta name="news_keywords" content="Digital Wallets,Digital India,Digital Payments,Electronic Banking Transactions,Electronic payment,Electronic payments,Cashless Economy,Mobile Banking">

<link rel="alternate" type="application/rss+xml" title="ROR" href="/ror.xml"/>

<link rel="alternate" type="application/rss+xml" title="RSS 2.0" href="/feeds/"/>

<link rel="stylesheet" href="/css/bootstrap.min.css?1697864993"/> <link rel="stylesheet" href="/css/style.css?v=1.1.2"/> <link rel="stylesheet" href="/css/style-inner.css?1577045210"/> <link rel="stylesheet" id="Oswald-css"

href="https://fonts.googleapis.com/css?family=Oswald%3Aregular%2C700&ver=3.8.1" type="text/css"

media="all">

<link rel="stylesheet" href="/css/jquery.modal.min.css?1578285302"/> <script src="/js/jquery-1.10.2.js?1575549704"></script> <script src="/js/jquery-migrate.min.js?1575549704"></script> <link rel="shortcut icon" href="/favicon.ico" title="Favicon">

<link rel="stylesheet" href="/css/jquery-ui.css?1580720609"/> <script src="/js/jquery-ui.js?1575549704"></script> <link rel="preload" as="style" href="https://www.im4change.org/css/custom.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery.modal.min.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery-ui.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/li-scroller.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<!-- <link rel="preload" as="style" href="https://www.im4change.org/css/style.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous"> -->

<link rel="preload" as="style" href="https://www.im4change.org/css/style-inner.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel='dns-prefetch' href="//im4change.org/css/custom.css" crossorigin >

<link rel="preload" as="script" href="https://www.im4change.org/js/bootstrap.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.li-scroller.1.0.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.modal.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.ui.totop.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-1.10.2.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-migrate.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-ui.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/setting.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/tie-scripts.js">

<!--[if IE]>

<script type="text/javascript">jQuery(document).ready(function () {

jQuery(".menu-item").has("ul").children("a").attr("aria-haspopup", "true");

});</script>

<![endif]-->

<!--[if lt IE 9]>

<script src="/js/html5.js"></script>

<script src="/js/selectivizr-min.js"></script>

<![endif]-->

<!--[if IE 8]>

<link rel="stylesheet" type="text/css" media="all" href="/css/ie8.css"/>

<![endif]-->

<meta property="og:title" content="NEWS ALERTS | No clear-cut trend in economy going cashless" />

<meta property="og:url" content="https://im4change.in/news-alerts-57/no-clear-cut-trend-in-economy-going-cashless-4682083.html" />

<meta property="og:type" content="article" />

<meta property="og:description" content="

Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens’ Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being..." />

<meta property="og:image" content="" />

<meta property="fb:app_id" content="0" />

<meta name="viewport" content="width=device-width, initial-scale=1, maximum-scale=1, user-scalable=no">

<link rel="apple-touch-icon-precomposed" sizes="144x144" href="https://im4change.in/images/apple1.png">

<link rel="apple-touch-icon-precomposed" sizes="120x120" href="https://im4change.in/images/apple2.png">

<link rel="apple-touch-icon-precomposed" sizes="72x72" href="https://im4change.in/images/apple3.png">

<link rel="apple-touch-icon-precomposed" href="https://im4change.in/images/apple4.png">

<style>

.gsc-results-wrapper-overlay{

top: 38% !important;

height: 50% !important;

}

.gsc-search-button-v2{

border-color: #035588 !important;

background-color: #035588 !important;

}

.gsib_a{

height: 30px !important;

padding: 2px 8px 1px 6px !important;

}

.gsc-search-button-v2{

height: 41px !important;

}

input.gsc-input{

background: none !important;

}

@media only screen and (max-width: 600px) {

.gsc-results-wrapper-overlay{

top: 11% !important;

width: 87% !important;

left: 9% !important;

height: 43% !important;

}

.gsc-search-button-v2{

padding: 10px 10px !important;

}

.gsc-input-box{

height: 28px !important;

}

/* .gsib_a {

padding: 0px 9px 4px 9px !important;

}*/

}

@media only screen and (min-width: 1200px) and (max-width: 1920px) {

table.gsc-search-box{

width: 15% !important;

float: right !important;

margin-top: -118px !important;

}

.gsc-search-button-v2 {

padding: 6px !important;

}

}

</style>

<script>

$(function () {

$("#accordion").accordion({

event: "click hoverintent"

});

});

/*

* hoverIntent | Copyright 2011 Brian Cherne

* http://cherne.net/brian/resources/jquery.hoverIntent.html

* modified by the jQuery UI team

*/

$.event.special.hoverintent = {

setup: function () {

$(this).bind("mouseover", jQuery.event.special.hoverintent.handler);

},

teardown: function () {

$(this).unbind("mouseover", jQuery.event.special.hoverintent.handler);

},

handler: function (event) {

var currentX, currentY, timeout,

args = arguments,

target = $(event.target),

previousX = event.pageX,

previousY = event.pageY;

function track(event) {

currentX = event.pageX;

currentY = event.pageY;

}

;

function clear() {

target

.unbind("mousemove", track)

.unbind("mouseout", clear);

clearTimeout(timeout);

}

function handler() {

var prop,

orig = event;

if ((Math.abs(previousX - currentX) +

Math.abs(previousY - currentY)) < 7) {

clear();

event = $.Event("hoverintent");

for (prop in orig) {

if (!(prop in event)) {

event[prop] = orig[prop];

}

}

// Prevent accessing the original event since the new event

// is fired asynchronously and the old event is no longer

// usable (#6028)

delete event.originalEvent;

target.trigger(event);

} else {

previousX = currentX;

previousY = currentY;

timeout = setTimeout(handler, 100);

}

}

timeout = setTimeout(handler, 100);

target.bind({

mousemove: track,

mouseout: clear

});

}

};

</script>

<script type="text/javascript">

var _gaq = _gaq || [];

_gaq.push(['_setAccount', 'UA-472075-3']);

_gaq.push(['_trackPageview']);

(function () {

var ga = document.createElement('script');

ga.type = 'text/javascript';

ga.async = true;

ga.src = ('https:' == document.location.protocol ? 'https://ssl' : 'http://www') + '.google-analytics.com/ga.js';

var s = document.getElementsByTagName('script')[0];

s.parentNode.insertBefore(ga, s);

})();

</script>

<link rel="stylesheet" href="/css/custom.css?v=1.16"/> <script src="/js/jquery.ui.totop.js?1575549704"></script> <script src="/js/setting.js?1575549704"></script> <link rel="manifest" href="/manifest.json">

<meta name="theme-color" content="#616163" />

<meta name="apple-mobile-web-app-capable" content="yes">

<meta name="apple-mobile-web-app-status-bar-style" content="black">

<meta name="apple-mobile-web-app-title" content="im4change">

<link rel="apple-touch-icon" href="/icons/logo-192x192.png">

</head>

<body id="top" class="home inner blog">

<div class="background-cover"></div>

<div class="wrapper animated">

<header id="theme-header" class="header_inner" style="position: relative;">

<div class="logo inner_logo" style="left:20px !important">

<a title="Home" href="https://im4change.in/">

<img src="https://im4change.in/images/logo2.jpg?1582080632" class="logo_image" alt="im4change"/> </a>

</div>

<div class="langhindi" style="color: #000;display:none;"

href="https://im4change.in/">

<a class="more-link" href="https://im4change.in/">Home</a>

<a href="https://im4change.in/hindi/" class="langbutton ">हिन्दी</a>

</div>

<nav class="fade-in animated2" id="main-nav">

<div class="container">

<div class="main-menu">

<ul class="menu" id="menu-main">

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children"

style="left: -40px;"><a

target="_blank" href="https://im4change.in/">Home</a>

</li>

<li class="menu-item mega-menu menu-item-type-taxonomy mega-menu menu-item-object-category mega-menu menu-item-has-children parent-list"

style=" margin-left: -40px;"><a href="#">KNOWLEDGE GATEWAY <span class="sub-indicator"></span>

</a>

<div class="mega-menu-block background_menu" style="padding-top:25px;">

<div class="container">

<div class="mega-menu-content">

<div class="mega-menu-item">

<h3><b>Farm Crisis</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/farmers039-suicides-14.html"

class="left postionrel">Farm Suicides </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/unemployment-30.html"

class="left postionrel">Unemployment </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/rural-distress-70.html"

class="left postionrel">Rural distress </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/migration-34.html"

class="left postionrel">Migration </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/key-facts-72.html"

class="left postionrel">Key Facts </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/debt-trap-15.html"

class="left postionrel">Debt Trap </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Empowerment</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/union-budget-73.html"

class="left postionrel">Union Budget And Other Economic Policies </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/forest-and-tribal-rights-61.html"

class="left postionrel">Forest and Tribal Rights </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-education-60.html"

class="left postionrel">Right to Education </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-food-59.html"

class="left postionrel">Right to Food </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/displacement-3279.html"

class="left postionrel">Displacement </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-work-mg-nrega-39.html"

class="left postionrel">Right to Work (MG-NREGA) </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/gender-3280.html"

class="left postionrel">GENDER </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/right-to-information-58.html"

class="left postionrel">Right to Information </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/empowerment/social-audit-48.html"

class="left postionrel">Social Audit </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Hunger / HDI</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/poverty-and-inequality-20499.html"

class="left postionrel">Poverty and inequality </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/malnutrition-41.html"

class="left postionrel">Malnutrition </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/public-health-51.html"

class="left postionrel">Public Health </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/education-50.html"

class="left postionrel">Education </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/hunger-overview-40.html"

class="left postionrel">Hunger Overview </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/hdi-overview-45.html"

class="left postionrel">HDI Overview </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/pds-ration-food-security-42.html"

class="left postionrel">PDS/ Ration/ Food Security </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/sdgs-113.html"

class="left postionrel">SDGs </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/hunger-hdi/mid-day-meal-scheme-mdms-53.html"

class="left postionrel">Mid Day Meal Scheme (MDMS) </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Environment</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/time-bomb-ticking-52.html"

class="left postionrel">Time Bomb Ticking </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/water-and-sanitation-55.html"

class="left postionrel">Water and Sanitation </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/environment/impact-on-agriculture-54.html"

class="left postionrel">Impact on Agriculture </a>

</p>

</div>

<div class="mega-menu-item">

<h3><b>Law & Justice</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/social-justice-20500.html"

class="left postionrel">Social Justice </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/access-to-justice-47.html"

class="left postionrel">Access to Justice </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/human-rights-56.html"

class="left postionrel">Human Rights </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/corruption-35.html"

class="left postionrel">Corruption </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/general-insecurity-46.html"

class="left postionrel">General Insecurity </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/law-justice/disaster-relief-49.html"

class="left postionrel">Disaster & Relief </a>

</p>

</div>

</div>

</div>

</div>

</li>

<li class="menu-item menu-item-type-post_type menu-item-object-page "><a target="_blank" href="https://im4change.in/nceus_reports.php">NCEUS reports</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children parent-list ">

<a target="_blank" href="https://im4change.in/about-us-9.html">About Us <span

class="sub-indicator"></span></a>

<ul class="sub-menu aboutmenu">

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/objectives-8.html">Objectives</a>

</li>

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/contactus.php">Contact

Us</a></li>

<li class="menu-item menu-item-type-post_type menu-item-object-page"><a

target="_blank" href="https://im4change.in/about-us-9.html">About

Us</a></li>

</ul>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children ">

<a target="_blank" href="https://im4change.in/fellowships.php" title="Fellowships">Fellowships</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/media-workshops.php">Workshops</a>

</li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/research.php">Research</a></li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children "><a

target="_blank" href="https://im4change.in/links-64">Partners</a></li>

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children"

id="menu-item-539"><a target="_blank" href="https://im4change.in/hindi/"

class="langbutton langlinkfont17">हिन्दी</a></li>

</ul>

</div> </div>

<!-- <div style="float: right;">

<script async src="https://cse.google.com/cse.js?cx=18b4f2e0f11bed3dd"></script>

<div class="gcse-search"></div>

</div> -->

<div class="search-block" style=" margin-left: 8px; margin-right: 7px;">

<form method="get" id="searchform" name="searchform"

action="https://im4change.in/search"

onsubmit="return searchvalidate();">

<button class="search-button" type="submit" value="Search"></button>

<input type="text" id="s" name="qryStr" value=""

onfocus="if (this.value == 'Search...') {this.value = '';}"

onblur="if (this.value == '') {this.value = 'Search...';}">

</form>

</div>

</nav>

</header>

<div class="container">

<div id="main-content" class=" main1 container fade-in animated3 sidebar-narrow-left">

<div class="content-wrap">

<div class="content" style="width: 900px;min-height: 500px;">

<div class="background_inner innBack" align="center">

<img src="https://im4change.in/images/media/im4change_20Cashless_transaction_image.jpg"

alt="No clear-cut trend in economy going cashless"

class="box_shadow mt5 imgRes" style="max-width:500px;"/>

</div>

<section class="cat-box recent-box innerCatRecent">

<h1 class="cat-box-title">No clear-cut trend in economy going cashless</h1>

<a href="JavaScript:void(0);" onclick="return shareArticle(33984);">

<img src="https://im4change.in/images/email.png?1582080630" border="0" width="24" align="right" alt="Share this article"/> </a>

<a href="https://im4change.in/news-alerts-57/no-clear-cut-trend-in-economy-going-cashless-4682083/print"

rel="nofollow">

<img src="https://im4change.in/images/icon-print.png?1582080630" border="0" width="24" align="right" alt="Share this article"/>

</a>

</section>

<section class="recent-box innerCatRecent">

<small class="pb-1"><span class="dateIcn">

<img src="https://im4change.in/images/published.svg?1582080666" alt="published"/>

Published on</span><span class="text-date"> Jun 16, 2017</span>

<span

class="dateIcn">

<img src="https://im4change.in/images/modified.svg?1582080666" alt="modified"/> Modified on </span><span class="text-date"> Jun 20, 2017</span>

</small>

</section>

<div class="clear"></div>

<div style="padding-top: 10px;">

<div class="innerLineHeight">

<div class="middleContent innerInput news-alerts-57">

<table>

<tr>

<td>

<div>

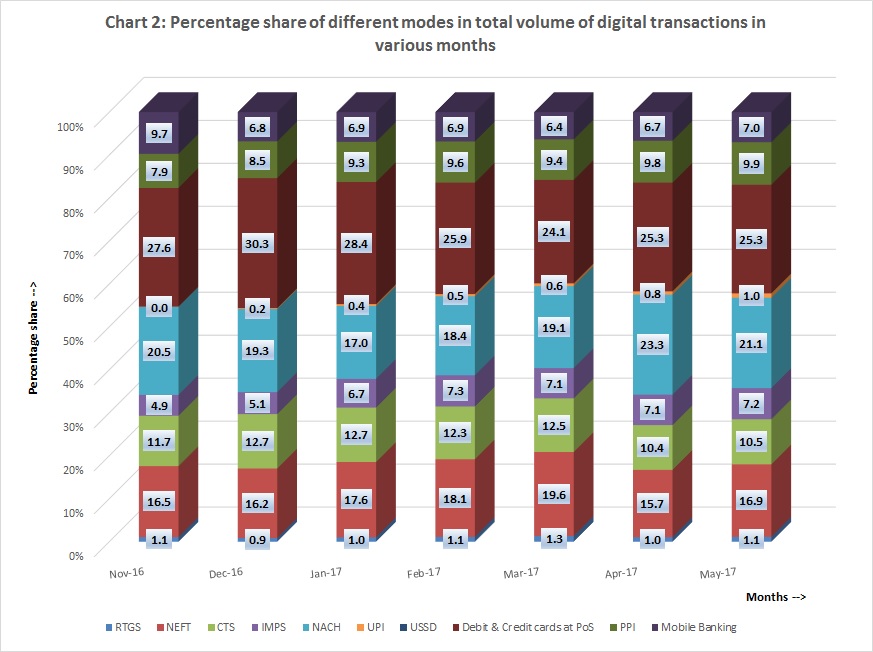

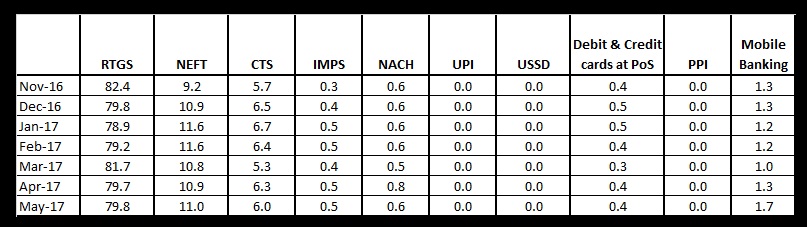

<br /><div align="justify">Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens’ Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being used by over 220 million users across the country. Although Paytm was launched in 2010, the popularity of its mobile wallet services and payment gateway among the ordinary citizens grew several folds only after 8 November, 2016 i.e. when the government banned currency notes of denomination Rs. 500/- and Rs. 1000/-.<br /><br />Following demonetisation, there has been a push on the part of the officialdom to move towards a digital economy, from the existing cash-based economy. A look at the data pertaining to electronic payments <em>(through various modes)</em>, which is provided by the Reserve Bank of India, would reveal the following facts:<br /><br />* The total volume of digital transactions in the economy reached a peak of 957.5 million in December, 2016, but it did not reach such a high level in the subsequent months. It means that the ordinary citizens moved towards cashless transactions out of compulsion <em>(following demonetisation of Rs. 500/- and Rs. 1000/- notes)</em>, and not out of choice. That is why the initial enthusiasm for cashless transactions petered out later on.<br /></div><div align="justify"> </div><div align="justify"><iframe src="http://plot.ly/~ShambhuGhatakb01c/25.embed" width="900" height="800"></iframe> <br /></div><div align="justify"><em><strong>Source: </strong>Electronic Payment Systems – Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br /><br /><strong>Notes: <br /><br /></strong>The growth rates in volume and value of cashless transactions (over previous months) have been calculated by the Inclusive Media for Change team.<br /><br />The data provided by RBI is provisional.<br /> <br />The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br /><br />NACH figures are for approved transactions only <br /><br />The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br /><br />The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br /><br />Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br /><br />Mobile Banking figures are taken from 5 banks.<br /><br /></em>* Although the growth rate in total volume of digital transactions (over previous month) touched 42.6 percent in December last year, it did not reach such a high level afterwards. It indicates that the initial excitement among the users pertaining to cashless transactions tapered off once the demonetisation period got over. Please check chart-1. <br /><br />* The growth in total volume of digital transactions (over previous month) turned negative in the months of January, February and April. The growth in total volume of digital transactions (over previous month) was negligible in May, 2017. Kindly see chart-1.<br /><br />* The total value of cashless transactions reached a peak of approximately Rs. 1.5 lakh billion in March, 2017.<br /><br />* The growth in total value of digital transactions (over previous month) became negative in the months of January, February and April. The growth rate in total value of digital transactions (over previous month) was 1.4 percent in May, 2017. Please see chart-1.<br /><br />* The RBI data on electronic payments reveal that there has been a spurt in both volume and value of total cashless transactions during March, 2017 as compared to the previous two months. <br /><br /><img src="https://im4change.in/siteadmin/tinymce/uploaded/Chart%202%20Percentage%20share%20of%20various%20modes%20in%20total%20volume%20of%20transactions.jpg" alt="Chart 2 Percentage share of various modes in total volume of transactions" width="329" height="245" /><br /><br /><em><strong>Source: </strong>Electronic Payment Systems – Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br /><br /><strong>Notes: <br /></strong><br />The percentage shares of various modes in total volume of electronic transactions (during different months) have been calculated by the Inclusive Media for Change team.<br /><br />The data provided by RBI is provisional.<br /> <br />The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br /><br />NACH figures are for approved transactions only <br /><br />The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br /><br />The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br /><br />Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br /><br />Mobile Banking figures are taken from 5 banks.<br /><br /></em>* During the month of May, 2017, the percentage share of the mode 'debit & credit cards at PoS' (i.e. 25.3 percent) in total volume of digital transactions has been the highest, followed by 'NACH' (21.1 percent), 'NEFT' (16.9 percent) and 'CTS' (10.5 percent). For the same month, the percentage share of the mode 'USSD' (i.e. zero percent) in total volume of digital transactions has been the lowest, followed by UPI (1.0 percent), 'RTGS' (1.1 percent) and 'mobile banking' (7.0 percent). Please consult chart-2.<br /><br />* The percentage share of the mode 'mobile banking' in total volume of cashless transactions reached a peak of 9.7 percent in November, 2016 but never reached such a high level later on. Kindly see chart-2. It indicates how the government’s demonetisation measure aided mobile banking initially. <br /><br /><strong>Table-1: Percentage share of different modes in total value of digital transactions during various months</strong><br /><br /></div><div align="justify"><img src="https://im4change.in/siteadmin/tinymce/uploaded/Table%201%20Percentage%20share%20of%20various%20modes%20in%20total%20value%20of%20digital%20transactions.jpg" alt="Table 1 Percentage share of various modes in total value of digital transactions" width="246" height="69" /> </div><div align="justify"> </div><div align="justify"><em><strong>Source: </strong>Electronic Payment Systems – Data Dissemination (Updated as on 11 June, 2017), Reserve Bank of India<br /><br /><strong>Notes: <br /></strong><br />The percentage shares of different modes in total value of electronic transactions (during various months) have been calculated by the Inclusive Media for Change team.<br /><br />The data provided by RBI is provisional.<br /> <br />The source of data for Cheque Truncation System (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), and Unified Payments Interface (UPI) is National Payments Corporation of India (NPCI). <br /><br />NACH figures are for approved transactions only <br /><br />The figures related to Unstructured Supplementary Service Data (USSD) is negligible. The source of data for USSD is NPCI. <br /><br />The figures related to 'debit and credit cards at Point-of-Sale (PoS)' have taken into account card transactions of only 4 banks. <br /><br />Prepaid Payments Instrument (PPI) issued by 8 non-bank issuers for goods and services transactions only have been taken into account in the data.<br /><br />Mobile Banking figures are taken from 5 banks.<br /><br /></em>* From the table-1, it could be observed that in the month of May, 2017, the percentage share of the mode 'RTGS' (i.e. 79.8 percent) in total value of digital transactions has been the highest, followed by 'NEFT' (11.0 percent), 'CTS' (6.0 percent) and 'mobile banking' (1.7 percent). For the same month, the percentage shares of the modes -- 'UPI', 'USSD' and ‘PPI’ (all zero percent) in total value of digital transactions have been the lowest, followed by 'debit & credit cards at PoS' (0.4 percent), 'IMPS' (0.5 percent) and 'NACH' (0.6 percent). <br /><br />* On comparing chart-2 against table-1, it could be said that although 'RTGS' has a meagre share in total volume of cashless transactions, which hovers around 1 percent, it occupies an overwhelmingly large share (around 80 percent) in the total value of electronic transactions <em>(from November, 2016 to May, 2017)</em>.<br /><br />* The percentage share of the mode 'mobile banking' in total value of cashless transactions has stayed below 2.0 percent during the last 7 months. <br /><br /><strong>Importance of going digital</strong><br /><br />Among other things, it has been argued by economists that a move towards a cashless economy would result in: a. Improvement in financial transparency and reduction in the generation of black money; b. Increase in tax base and thus tax collection; c. Financial inclusion; d. Reduction in incidence of corruption and tax evasion; and e. Reduction in the cost of printing hard currency. <br /><br />According to the official website <a href="http://cashlessindia.gov.in" title="http://cashlessindia.gov.in">http://cashlessindia.gov.in</a>, there are various modes of digital payments that are available before the citizens. They are as follows: <br /><br />1. Banking cards which include debit cards, credit cards, prepaid cards etc. Examples: RuPay, Visa, MasterCard etc.; <br />2. Unstructured Supplementary Service Data (USSD);<br />3. Aadhaar Enabled Payment System (AEPS);<br />4. Unified Payments Interface (UPI); <br />5. Mobile Wallets: Most banks have their e-wallets, and some of the private companies are also providing mobile wallets such as: Paytm, Freecharge, Mobikwik, Oxigen, mRuppee, Airtel Money, Jio Money, SBI Buddy, itz Cash, Citrus Pay, Vodafone M-Pesa, Axis Bank Lime, ICICI Pockets, SpeedPay etc.;<br />6. Point-of-Sale devices (PoS devices);<br />7. Internet Banking, which includes National Electronic Fund Transfer (NEFT), Real Time Gross Settlement (RTGS), Electronic Clearing System (ECS) & Immediate Payment Service (IMPS); <br />8. Mobile Banking;<br />9. Micro ATMs.<br /><br /><br /><strong><em>References: </em></strong><br /><br />Electronic Payment Systems – Data Dissemination (Updated as on June 11, 2017), Reserve Bank of India, please <a href="http://rbidocs.rbi.org.in/rdocs/content/docs/ELECT07022016_A.xls" title="http://rbidocs.rbi.org.in/rdocs/content/docs/ELECT07022016_A.xls">click here</a> to access<br /> <br />Promoting Digital Payments among People, please <a href="http://cashlessindia.gov.in/promoting_digital_payments_people.html" title="http://cashlessindia.gov.in/promoting_digital_payments_people.html">click here</a> to access<br /><br />Paytm founder Vijay Shekhar Sharma to buy Rs 82 crore worth real estate in Lutyens’ Delhi, The Indian Express, 7 June, 2017, please <a href="http://indianexpress.com/article/business/paytm-founder-vijay-shekhar-sharma-to-buy-rs-82-crore-worth-real-estate-in-lutyens-delhi-4692547/" title="http://indianexpress.com/article/business/paytm-founder-vijay-shekhar-sharma-to-buy-rs-82-crore-worth-real-estate-in-lutyens-delhi-4692547/">click here</a> to access <br /> <br />Mobile wallets see a soaring growth post-demonetisation -Sunny Sen, Hindustan Times, 1 January, 2017, please <a href="http://www.hindustantimes.com/business-news/mobile-wallets-see-a-soaring-growth-post-demonetisation/story-zwdBi3UGqG1qZD92AEF9GK.html" title="http://www.hindustantimes.com/business-news/mobile-wallets-see-a-soaring-growth-post-demonetisation/story-zwdBi3UGqG1qZD92AEF9GK.html">click here</a> to access <br /><br />Here are the advantages of cashless payments and the pitfalls you should beware of -Riju Dave, The Economic Times, 12 December, 2016, please <a href="http://economictimes.indiatimes.com/wealth/spend/going-cashless-is-it-good-for-you/articleshow/55908649.cms" title="http://economictimes.indiatimes.com/wealth/spend/going-cashless-is-it-good-for-you/articleshow/55908649.cms">click here</a> to access <br /><br />Demonetisation’s impact on mobile wallets, Livemint.com, 7 December, 2016, please <a href="http://www.livemint.com/Industry/qauzUZqgYFhwhPnt18CgIM/Demonetisation-and-the-digital-economy.html" title="http://www.livemint.com/Industry/qauzUZqgYFhwhPnt18CgIM/Demonetisation-and-the-digital-economy.html">click here</a> to access, <br /></div><div align="justify"> </div><div align="justify"> </div><div align="justify"><strong>Image Courtesy: Inclusive Media for Change/ Shambhu Ghatak</strong> <br /></div>

</div>

</td>

</tr>

</table>

</div>

</div>

</div>

<div class="clear"></div>

<div style="padding-top: 18px;">

<p class="post-tag">Tagged with:

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Digital Wallets"

title="Digital Wallets">

Digital Wallets </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Digital India"

title="Digital India">

Digital India </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Digital Payments"

title="Digital Payments">

Digital Payments </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Electronic Banking Transactions"

title="Electronic Banking Transactions">

Electronic Banking Transactions </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Electronic payment"

title="Electronic payment">

Electronic payment </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Electronic payments"

title="Electronic payments">

Electronic payments </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Cashless Economy"

title="Cashless Economy">

Cashless Economy </a>

<a class="tagcloud5"

href="https://im4change.in/search?qryStr=Mobile Banking"

title="Mobile Banking">

Mobile Banking </a>

</p>

</div>

<div class="clear"></div>

<br><br>

<div class="widget-top">

<h4>Related Articles</h4>

<div class="stripe-line"></div>

</div>

<div class="widget-container">

<ul id="recentcomments">

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/5-reasons-why-cash-is-back-in-the-economy-after-5-years-of-demonetisation-anand-adhikari.html"

title="5 reasons why cash is back in the economy after 5 years of demonetisation -Anand Adhikari">

5 reasons why cash is back in the economy after 5 years of demonetisation -Anand Adhikari </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/five-years-since-demonetisation-what-has-changed-roshan-kishore.html"

title="Five years since demonetisation: What has changed? -Roshan Kishore">

Five years since demonetisation: What has changed? -Roshan Kishore </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/one-for-the-record-books-rachna-khaira.html"

title="One for the Record Books -Rachna Khaira">

One for the Record Books -Rachna Khaira </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/they-made-it-to-college-despite-all-odds-but-pandemic-apathy-is-making-adivasi-students-drop-out-prashant-rathod.html"

title="They made it to college. Despite all odds. But pandemic apathy is making Adivasi students drop out -Prashant Rathod">

They made it to college. Despite all odds. But pandemic apathy is making Adivasi students drop out -Prashant Rathod </a>

</li>

<li class="recentcomments">

<a href="https://im4change.in/latest-news-updates/166k-students-in-delhi-fell-off-grid-as-schools-moved-online-fareeha-iftikhar.html"

title="166k students in Delhi fell off grid as schools moved online -Fareeha Iftikhar">

166k students in Delhi fell off grid as schools moved online -Fareeha Iftikhar </a>

</li>

</ul>

</div>

<div class="comment-respond" id="respond">

<a name="commentbox"> </a>

<h3 class="comment-reply-title" id="reply-title">Write Comments</h3>

<form method="post" accept-charset="utf-8" role="form" action="/news-alerts-57/no-clear-cut-trend-in-economy-going-cashless-4682083.html"><div style="display:none;"><input type="hidden" name="_method" value="POST"/></div> <form class="comment-form" id="commentform" method="post" action="#commentbox" onSubmit="return validate()"

name="cmtform">

<input type="hidden" name="cmttype" value="articlecmt"/>

<input type="hidden" name="article_id" value="33984"/>

<p class="comment-notes">Your email address will not be published. Required fields are marked <span

class="required">*</span></p>

<p class="comment-form-author">

<label for="commenterName">Name</label>

<span class="required">*</span>

<input type="text" aria-required="true" size="30"

value=""

name="commenterName" id="commenterName" required="true">

</p>

<p class="comment-form-email">

<label for="commenterEmail">Email</label> <span class="required">*</span>

<input aria-required="true" size="30" name="commenterEmail" id="commenterEmail" type="email"

value=""

required="true">

</p>

<p class="comment-form-contact">

<label for="commenterPh">Contact No.</label>

<input type="text" size="30"

value=""

name="commenterPh" id="commenterPh">

</p>

<p class="comment-form-comment">

<label for="comment">Comment</label>

<textarea aria-required="true" required="true" rows="8" cols="45" name="comment"

id="comment"></textarea>

</p>

<p class="comment-form-comment">

<label for="comment">Type the characters you see in the image below <span class="required">*</span><br><img

class="captchaImg"

src="https://im4change.in/securimage_show_art.php?tk=908309459" alt="captcha"/>

</label>

</p>

<input type="text" name="vrcode" required="true"/>

<p class="form-submit" style="width: 200px;">

<input type="submit" value="Post Comment" id="submit" name="submit">

</p></form>

</div>

<style>

.ui-widget-content {

height: auto !important;

}

</style>

<div id="share-modal"></div>

<style>

.middleContent a{

background-color: rgba(108,172,228,.2);

}

.middleContent a:hover{

background-color: #418fde;

border-color: #418fde;

color: #000;

}

</style>

<script>

function shareArticle(article_id) {

var options = {

modal: true,

height: 'auto',

width: 600 + 'px'

};

$('#share-modal').html("");

$('#share-modal').load('https://im4change.in/share_article?article_id=' + article_id).dialog(options).dialog('open');

}

function postShare() {

var param = 'article_id=' + $("#article_id").val();

param = param + '&y_name=' + $("#y_name").val();

param = param + '&y_email=' + $("#y_email").val();

param = param + '&f_name=' + $("#f_name").val();

param = param + '&f_email=' + $("#f_email").val();

param = param + '&y_msg=' + $("#y_msg").val();

$.ajax({

type: "POST",

url: 'https://im4change.in/post_share_article',

data: param,

success: function (response) {

$('#share-modal').html("Thank You, Your message posted to ");

}

});

return false;

}

</script> </div>

</div>

<!-- Right Side Section Start -->

<!-- MAP Section START -->

<aside class="sidebar indexMarg">

<div class="ad-cell">

<a href="https://im4change.in/statemap.php" title="">

<img src="https://im4change.in/images/map_new_version.png?1582080666" alt="India State Map" class="indiamap" width="232" height="252"/> </a>

<div class="rightmapbox">

<div id="sideOne" class="docltitle"><a href="https://im4change.in/state-report/india/36" target="_blank">DOCUMENTS/

REPORTS</a></div>

<div id="sideTwo" class="statetitle"><a href="https://im4change.in/states.php"target="_blank">STATE DATA/

HDRs.</a></div>

</div>

<div class="widget widgePadTop"></div>

</div>

</aside>

<!-- MAP Section END -->

<aside class="sidebar sidePadbottom">

<div class="rightsmlbox1" >

<a href="https://im4change.in/knowledge_gateway" target="_blank" style="color: #035588;

font-size: 17px;">

KNOWLEDGE GATEWAY

</a>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title">

<a href="https://im4change.in/newsletter" target="_blank">

NEWSLETTER

</a>

</p>

</div>

</div>

<div class="rightsmlbox1" style="height: 325px;">

<div>

<p class="rightsmlbox1_title">

Interview with Prof. Ravi Srivastava

</p>

<p class="rightsmlbox1_title">

<a href="https://im4change.in/video/interview-with-prof-ravi-srivastava-on-current-economic-crisis">

<img width="250" height="200" src="/images/interview_video_home.jpg" alt="Interview with Prof. Ravi Srivastava"/>

</a>

<!--

<iframe width="250" height="200" src="https://www.youtube.com/embed/MmaTlntk-wc" frameborder="0" allow="accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture" allowfullscreen=""></iframe>-->

</p>

<a href="https://im4change.in/videogallery" class="more-link CatArchalAnch1" target="_blank">

More videos

</a>

</div>

</div>

<div class="rightsmlbox1">

<div>

<!--div id="sstory" class="rightboxicons"></div--->

<p class="rightsmlbox1_title"><a href="https://im4change.in/list-success-stories" target="_blank">Success Stories</a></p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a

href="https://im4change.in/interviews" target="_blank">Interviews</a>

</p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a href="https://www.commoncause.in/page.php?id=10" >Donate</a></p>

</div>

</div>

<div class="rightsmlbox1">

<div>

<p class="rightsmlbox1_title"><a

href="https://im4change.in/marquee"

class="isf_link more-link" title="India Focus?" style="border: 4px solid #fdd922;width: 90%;background-color: #fdd922;text-align: center;color: #000000;font-size:18px" target="_blank">India Focus</a></p> </div>

</div>

<div class="rightsmlbox1" style="height: 104px !important;">

<a href="https://im4change.in/quarterly_reports.php" target="_blank">

Quarterly Reports on Effect of Economic Slowdown on Employment in India (2008 - 2015)

</a>

</div>

<!-- <div class="rightsmlbox1">

<a href="https://play.google.com/store/apps/details?id=com.im4.im4change" target="_blank">

</a></div> -->

<!-- <section class="cat-box recent-box secMarg">

<h2 class="cat-box-title">Most Visited</h2>

</section> -->

<!-- accordion Starts here -->

<!-- <div id="accordion" class="accordMarg">

</div> -->

<!-- accordion ends here -->

<!-- Widget Tag Cloud Starts here -->

<div id="tag_cloud-2" class="widget widget_tag_cloud">

<section class="cat-box recent-box secMarg">

<h2 class="cat-box-title">MOST VISITED TAGS</h2>

</section>

<div class="widget-top wiPdTp">

<div class="stripe-line"></div>

</div>

<div class="widget-container">

<div class="tagcloud">

<a href="https://im4change.in/search?qryStr=Agriculture"

target="_blank" class="tag-link-4 font4">Agriculture</a>

<a href="https://im4change.in/search?qryStr=Food Security"

target="_blank" class="tag-link-4 font4">Food Security</a>

<a href="https://im4change.in/search?qryStr=Law and Justice"

target="_blank" class="tag-link-4 font4">Law and Justice</a>

<a href="https://im4change.in/search?qryStr=Health"

target="_blank" class="tag-link-4 font4">Health</a>

<a href="https://im4change.in/search?qryStr=Right to Food"

target="_blank" class="tag-link-4 font4">Right to Food</a>

<a href="https://im4change.in/search?qryStr=Corruption"

target="_blank" class="tag-link-4 font4">Corruption</a>

<a href="https://im4change.in/search?qryStr=farming"

target="_blank" class="tag-link-4 font4">farming</a>

<a href="https://im4change.in/search?qryStr=Environment"

target="_blank" class="tag-link-4 font4">Environment</a>

<a href="https://im4change.in/search?qryStr=Right to Information"

target="_blank" class="tag-link-4 font4">Right to Information</a>

<a href="https://im4change.in/search?qryStr=NREGS"

target="_blank" class="tag-link-4 font4">NREGS</a>

<a href="https://im4change.in/search?qryStr=Human Rights"

target="_blank" class="tag-link-4 font4">Human Rights</a>

<a href="https://im4change.in/search?qryStr=Governance"

target="_blank" class="tag-link-4 font4">Governance</a>

<a href="https://im4change.in/search?qryStr=PDS"

target="_blank" class="tag-link-4 font4">PDS</a>

<a href="https://im4change.in/search?qryStr=COVID-19"

target="_blank" class="tag-link-4 font4">COVID-19</a>

<a href="https://im4change.in/search?qryStr=Land Acquisition"

target="_blank" class="tag-link-4 font4">Land Acquisition</a>

<a href="https://im4change.in/search?qryStr=mgnrega"

target="_blank" class="tag-link-4 font4">mgnrega</a>

<a href="https://im4change.in/search?qryStr=Farmers"

target="_blank" class="tag-link-4 font4">Farmers</a>

<a href="https://im4change.in/search?qryStr=transparency"

target="_blank" class="tag-link-4 font4">transparency</a>

<a href="https://im4change.in/search?qryStr=Gender"

target="_blank" class="tag-link-4 font4">Gender</a>

<a href="https://im4change.in/search?qryStr=Poverty"

target="_blank" class="tag-link-4 font4">Poverty</a>

<a href="https://im4change.in/search?qryStr=Farm Laws" target="_blank" class="tag-link-4 font4">Farm Laws

</a>

<a href="https://im4change.in/search?qryStr=Citizenship Amendment Act" target="_blank" class="tag-link-4 font4">Citizenship Amendment Act

</a>

<a href="https://im4change.in/search?qryStr=CAA NPR NRIC" target="_blank" class="tag-link-4 font4">CAA NPR NRIC

</a>

<a href="https://im4change.in/search?qryStr=Job Losses" target="_blank" class="tag-link-4 font4">Job Losses

</a>

<a href="https://im4change.in/search?qryStr=Migrant Workers" target="_blank" class="tag-link-4 font4">Migrant Workers

</a>

<a href="https://im4change.in/search?qryStr=Unemployment" target="_blank" class="tag-link-4 font4">Unemployment

</a>

<a href="https://im4change.in/search?qryStr=PMGKAY" target="_blank" class="tag-link-4 font4">PMGKAY

</a>

<a href="https://im4change.in/search?qryStr=PM-KISAN" target="_blank" class="tag-link-4 font4">PM-KISAN

</a>

<a href="https://im4change.in/search?qryStr=PM-CARES" target="_blank" class="tag-link-4 font4">PM-CARES

</a>

<a href="https://im4change.in/search?qryStr=LFPR" target="_blank" class="tag-link-4 font4">LFPR

</a>

</div>

</div>

</div>

<!-- Widget Tag Cloud Ends here -->

</aside>

<!-- Right Side Section End -->

</div>

<section class="cat-box cats-review-box footerSec">

<h2 class="cat-box-title vSec CatArcha">Video

Archives</h2>

<h2 class="cat-box-title CatArchaTitle">Archives</h2>

<div class="cat-box-content">

<div class="reviews-cat">

<div class="CatArchaDiv1">

<div class="CatArchaDiv2">

<ul>

<li>

<a href="https://im4change.in/news-alerts-57/moving-upstream-luni-fellowship.html" target="_blank">

Moving Upstream: Luni – Fellowship </a>

</li>

<li>

<a href="https://im4change.in/news-alerts-57/135-million-indians-exited-multidimensional-poverty-as-per-government-figures-is-that-the-same-as-poverty-reduction.html" target="_blank">

135 Million Indians Exited “Multidimensional" Poverty as per Government... </a>

</li>

<li>

<a href="https://im4change.in/news-alerts-57/explainer-why-are-tomato-prices-on-fire.html" target="_blank">

Explainer: Why are Tomato Prices on Fire? </a>

</li>

<li>

<a href="https://im4change.in/news-alerts-57/nsso-survey-only-39-1-of-all-households-have-drinking-water-within-dwelling-46-7-of-rural-households-use-firewood-for-cooking.html" target="_blank">

NSSO Survey: Only 39.1% of all Households have Drinking... </a>

</li>

<li class="CatArchalLi1">

<a href="https://im4change.in/news-alerts-57"

class="more-link CatArchalAnch1" target="_blank">

More...

</a>

</li>

</ul>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/I51LYnP8BOk/1.jpg"

alt=" Im4Change.org हिंदी वेबसाइट का परिचय. Short Video on im4change.org...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Short-Video-on-im4change-Hindi-website-Inclusive-Media-for-Change" target="_blank">

Im4Change.org हिंदी वेबसाइट का परिचय. Short Video on im4change.org... </a>

</p>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/kNqha-SwfIY/1.jpg"

alt=" "Session 1: Scope of IDEA and AgriStack" in Exploring...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Session-1- Scope-of-IDEA-and-AgriStack-in-Exploring-Digitalisation-in-Agriculture-29-April-2022" target="_blank">

"Session 1: Scope of IDEA and AgriStack" in Exploring... </a>

</p>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/6kIVjlgZItk/1.jpg"

alt=" "Session 2: Farmer Centric Digitalisation in Agriculture" in Exploring...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Session-2-Farmer-Centric-Digitalisation-in-Agriculture-in-Exploring-Digitalisation-in-Agriculture-29-April-2022" target="_blank">

"Session 2: Farmer Centric Digitalisation in Agriculture" in Exploring... </a>

</p>

</div>

<div class="CatArchaWidth">

<img class="CatArchaImg"

src="https://img.youtube.com/vi/2BeHTu0y7xc/1.jpg"

alt=" "Session 3: Future of Digitalisation in Agriculture" in Exploring...">

<p class="CatArchaPPad">

<a href="https://im4change.in/video/Session-3-Future-of-Digitalisation-in-Agriculture-in-Exploring-Digitalisation-in-Agriculture-29-April-2022" target="_blank">

"Session 3: Future of Digitalisation in Agriculture" in Exploring... </a>

</p>

</div>

<div class="divWidth">

<ul class="divWidthMarg">

<li>

<a href="https://im4change.in/video/Public-Spending-on-Agriculture-in-India-Source-Foundation-for-Agrarian-Studies"

title="Public Spending on Agriculture in India (Source: Foundation for Agrarian Studies)" target="_blank">

Public Spending on Agriculture in India (Source: Foundation for...</a>

</li>

<li>

<a href="https://im4change.in/video/Agrarian-Change-Seminar-Protests-against-the-New-Farm-Laws-in-India-by-Prof-Vikas-Rawal-JNU-Source-Journal-Of-Agrarian-Change"

title="Agrarian Change Seminar: 'Protests against the New Farm Laws in India' by Prof. Vikas Rawal, JNU (Source: Journal Of Agrarian Change) " target="_blank">

Agrarian Change Seminar: 'Protests against the New Farm Laws...</a>

</li>

<li>

<a href="https://im4change.in/video/Webinar-Ramrao-The-Story-of-India-Farm-Crisis-Source-Azim-Premji-University"

title="Webinar: Ramrao - The Story of India's Farm Crisis (Source: Azim Premji University)" target="_blank">

Webinar: Ramrao - The Story of India's Farm Crisis...</a>

</li>

<li>

<a href="https://im4change.in/video/water-and-agricultural-transformation-in-India"

title="Water and Agricultural Transformation in India: A Symbiotic Relationship (Source: IGIDR)" target="_blank">

Water and Agricultural Transformation in India: A Symbiotic Relationship...</a>

</li>

<li class="CatArchalLi1">

<a href="https://im4change.in/videogallery"

class="more-link CatArchalAnch1" target="_blank">

More...

</a>

</li>

</ul>

</div>

</div>

</div>

</div>

</section> </div>

<div class="clear"></div>

<!-- Footer option Starts here -->

<div class="footer-bottom fade-in animated4">

<div class="container">

<div class="social-icons icon_flat">

<p class="SocialMargTop"> Website Developed by <a target="_blank" title="Web Development"

class="wot right"

href="http://www.ravinderkhurana.com/" rel="nofollow">

RAVINDErkHURANA.com</a></p>

</div>

<div class="alignleft">

<a

target="_blank" href="https://im4change.in/objectives-8.html"

class="link"

title="Objectives">Objectives</a> | <a

target="_blank" href="https://im4change.in/about-us-9.html"

class="link" title="About Us">About Us</a> | <a

target="_blank" href="https://im4change.in/media-workshops.php"

class="ucwords">Workshops</a> | <a

target="_blank" href="https://im4change.in/disclaimer/disclaimer-149.html"

title="Disclaimer">Disclaimer</a> </div>

</div>

</div>

<!-- Footer option ends here -->

</div>

<div id="connect">

<a target="_blank"

href="http://www.facebook.com/sharer.php?u=https://im4change.in/news-alerts-57/no-clear-cut-trend-in-economy-going-cashless-4682083.html"

title="Share on Facebook">

<img src="https://im4change.in/images/Facebook.png?1582080640" alt="share on Facebook" class="ImgBorder"/>

</a><br/>

<a target="_blank"

href="http://twitter.com/share?text=Im4change&url=https://im4change.in/news-alerts-57/no-clear-cut-trend-in-economy-going-cashless-4682083.html"

title="Share on Twitter">

<img src="https://im4change.in/images/twitter.png?1582080632" alt="Twitter" class="ImgBorder"/> </a>

<br/>

<a href="/feeds" title="RSS Feed" target="_blank">

<img src="https://im4change.in/images/rss.png?1582080632" alt="RSS" class="ImgBorder"/>

</a>

<br/>

<a class="feedback-link" id="feedbackFormLink" href="#">

<img src="https://im4change.in/images/feedback.png?1582080630" alt="Feedback" class="ImgBorder"/>

</a> <br/>

<a href="javascript:function iprl5(){var d=document,z=d.createElement('scr'+'ipt'),b=d.body,l=d.location;try{if(!b)throw(0);d.title='(Saving...) '+d.title;z.setAttribute('src',l.protocol+'//www.instapaper.com/j/WKrH3R7ORD5p?u='+encodeURIComponent(l.href)+'&t='+(new Date().getTime()));b.appendChild(z);}catch(e){alert('Please wait until the page has loaded.');}}iprl5();void(0)"

class="bookmarklet" onclick="return explain_bookmarklet();">

<img src="https://im4change.in/images/read-it-later.png?1582080632" alt="Read Later" class="ImgBorder"/> </a>

</div>

<!-- Feedback form Starts here -->

<div id="feedbackForm" class="overlay_form" class="ImgBorder">

<h2>Contact Form</h2>

<div id="contactform1">

<div id="formleft">

<form id="submitform" action="/contactus.php" method="post">

<input type="hidden" name="submitform" value="submitform"/>

<input type="hidden" name="salt_key" value="a0e0f2c6a0644a70e57ad2c96829709a"/>

<input type="hidden" name="ref" value="feedback"/>

<fieldset>

<label>Name :</label>

<input type="text" name="name" class="tbox" required/>

</fieldset>

<fieldset>

<label>Email :</label>

<input type="text" name="email" class="tbox" required/>

</fieldset>

<fieldset>

<label>Message :</label>

<textarea rows="5" cols="20" name="message" required></textarea>

</fieldset>

<fieldset>

Please enter security code

<div class="clear"></div>

<input type="text" name="vrcode" class="tbox"/>

</fieldset>

<fieldset>

<input type="submit" class="button" value="Submit"/>

<a href="#" id="closefeedbakcformLink">Close</a>

</fieldset>

</form>

</div>

<div class="clearfix"></div>

</div>

</div>

<div id="donate_popup" class="modal" style="max-width: 800px;">

<table width="100%" border="1">

<tr>

<td colspan="2" align="center">

<b>Support im4change</b>

</td>

</tr>

<tr>

<td width="25%" valign="middle">

<img src="https://im4change.in/images/logo2.jpg?1582080632" alt="" width="100%"/> </td>

<td style="padding-left:10px;padding-top:10px;">

<form action="https://im4change.in/donate" method="get">

<table width="100%" cellpadding="2" cellspacing="2">

<tr>

<td width="33%" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

10

</td>

<td width="33%" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

100

</td>

<td width="33%" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

1000

</td>

</tr>

<tr>

<td colspan="3">

</td>

</tr>

<tr>

<td style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

50

</td>

<td style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

500

</td>

<td style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

<input type="text" name="price" placeholder="?" style="font-family: 'Script Font', cursive, Arial;font-size: 20px;font-weight: 700;">

</td>

</tr>

<tr>

<td colspan="3">

</td>

</tr>

<tr>

<td colspan="3" align="right">

<input type="button" name="Pay" value="Pay"

style="width: 200px;background-color: rgb(205, 35, 36);color: #ffffff;"/>

</td>

</tr>

</table>

</form>

</td>

</tr>

</table>

</div><script type='text/javascript'>

/* <![CDATA[ */

var tievar = {'go_to': 'Go to...'};

/* ]]> */

</script>

<script src="/js/tie-scripts.js?1575549704"></script><script src="/js/bootstrap.js?1575549704"></script><script src="/js/jquery.modal.min.js?1578284310"></script><script>

$(document).ready(function() {

// tell the autocomplete function to get its data from our php script

$('#s').autocomplete({

source: "/autocomplete"

});

});

</script>

<script src="/vj-main-sw-register.js" async></script>

<script>function init(){var imgDefer=document.getElementsByTagName('img');for(var i=0;i<imgDefer.length;i++){if(imgDefer[i].getAttribute('data-src')){imgDefer[i].setAttribute('src',imgDefer[i].getAttribute('data-src'))}}}

window.onload=init;</script>

</body>

</html>'

}

$maxBufferLength = (int) 8192

$file = '/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php'

$line = (int) 853

$message = 'Unable to emit headers. Headers sent in file=/home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php line=853'

Cake\Http\ResponseEmitter::emit() - CORE/src/Http/ResponseEmitter.php, line 48

Cake\Http\Server::emit() - CORE/src/Http/Server.php, line 141

[main] - ROOT/webroot/index.php, line 39

Warning (2): Cannot modify header information - headers already sent by (output started at /home/brlfuser/public_html/vendor/cakephp/cakephp/src/Error/Debugger.php:853) [CORE/src/Http/ResponseEmitter.php, line 148]

$response = object(Cake\Http\Response) {

'status' => (int) 200,

'contentType' => 'text/html',

'headers' => [

'Content-Type' => [

[maximum depth reached]

]

],

'file' => null,

'fileRange' => [],

'cookies' => object(Cake\Http\Cookie\CookieCollection) {},

'cacheDirectives' => [],

'body' => '<!DOCTYPE html>

<!--[if lt IE 7 ]>

<html class="ie ie6" lang='en'> <![endif]-->

<!--[if IE 7 ]>

<html class="ie ie7" lang='en'> <![endif]-->

<!--[if IE 8 ]>

<html class="ie ie8" lang='en'> <![endif]-->

<!--[if (gte IE 9)|!(IE)]><!-->

<html lang='en'>

<!--<![endif]-->

<head><meta http-equiv="Content-Type" content="text/html; charset=utf-8">

<title>

NEWS ALERTS | No clear-cut trend in economy going cashless </title>

<meta name="description" content="

Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens’ Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being..."/>

<meta name="keywords" content="Digital Wallets,Digital India,Digital Payments,Electronic Banking Transactions,Electronic payment,Electronic payments,Cashless Economy,Mobile Banking"/>

<meta name="news_keywords" content="Digital Wallets,Digital India,Digital Payments,Electronic Banking Transactions,Electronic payment,Electronic payments,Cashless Economy,Mobile Banking">

<link rel="alternate" type="application/rss+xml" title="ROR" href="/ror.xml"/>

<link rel="alternate" type="application/rss+xml" title="RSS 2.0" href="/feeds/"/>

<link rel="stylesheet" href="/css/bootstrap.min.css?1697864993"/> <link rel="stylesheet" href="/css/style.css?v=1.1.2"/> <link rel="stylesheet" href="/css/style-inner.css?1577045210"/> <link rel="stylesheet" id="Oswald-css"

href="https://fonts.googleapis.com/css?family=Oswald%3Aregular%2C700&ver=3.8.1" type="text/css"

media="all">

<link rel="stylesheet" href="/css/jquery.modal.min.css?1578285302"/> <script src="/js/jquery-1.10.2.js?1575549704"></script> <script src="/js/jquery-migrate.min.js?1575549704"></script> <link rel="shortcut icon" href="/favicon.ico" title="Favicon">

<link rel="stylesheet" href="/css/jquery-ui.css?1580720609"/> <script src="/js/jquery-ui.js?1575549704"></script> <link rel="preload" as="style" href="https://www.im4change.org/css/custom.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery.modal.min.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/jquery-ui.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel="preload" as="style" href="https://www.im4change.org/css/li-scroller.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<!-- <link rel="preload" as="style" href="https://www.im4change.org/css/style.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous"> -->

<link rel="preload" as="style" href="https://www.im4change.org/css/style-inner.css" onload="this.rel='stylesheet'" media="all" crossorigin="anonymous">

<link rel='dns-prefetch' href="//im4change.org/css/custom.css" crossorigin >

<link rel="preload" as="script" href="https://www.im4change.org/js/bootstrap.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.li-scroller.1.0.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.modal.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery.ui.totop.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-1.10.2.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-migrate.min.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/jquery-ui.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/setting.js">

<link rel="preload" as="script" href="https://www.im4change.org/js/tie-scripts.js">

<!--[if IE]>

<script type="text/javascript">jQuery(document).ready(function () {

jQuery(".menu-item").has("ul").children("a").attr("aria-haspopup", "true");

});</script>

<![endif]-->

<!--[if lt IE 9]>

<script src="/js/html5.js"></script>

<script src="/js/selectivizr-min.js"></script>

<![endif]-->

<!--[if IE 8]>

<link rel="stylesheet" type="text/css" media="all" href="/css/ie8.css"/>

<![endif]-->

<meta property="og:title" content="NEWS ALERTS | No clear-cut trend in economy going cashless" />

<meta property="og:url" content="https://im4change.in/news-alerts-57/no-clear-cut-trend-in-economy-going-cashless-4682083.html" />

<meta property="og:type" content="article" />

<meta property="og:description" content="

Paytm's founder Vijay Shekhar Sharma was in the news recently for signing a deal to purchase a Rs. 82 crore worth property in Lutyens’ Delhi. He is credited with the growth of Paytm's mobile wallet services, which is currently being..." />

<meta property="og:image" content="" />

<meta property="fb:app_id" content="0" />

<meta name="viewport" content="width=device-width, initial-scale=1, maximum-scale=1, user-scalable=no">

<link rel="apple-touch-icon-precomposed" sizes="144x144" href="https://im4change.in/images/apple1.png">

<link rel="apple-touch-icon-precomposed" sizes="120x120" href="https://im4change.in/images/apple2.png">

<link rel="apple-touch-icon-precomposed" sizes="72x72" href="https://im4change.in/images/apple3.png">

<link rel="apple-touch-icon-precomposed" href="https://im4change.in/images/apple4.png">

<style>

.gsc-results-wrapper-overlay{

top: 38% !important;

height: 50% !important;

}

.gsc-search-button-v2{

border-color: #035588 !important;

background-color: #035588 !important;

}

.gsib_a{

height: 30px !important;

padding: 2px 8px 1px 6px !important;

}

.gsc-search-button-v2{

height: 41px !important;

}

input.gsc-input{

background: none !important;

}

@media only screen and (max-width: 600px) {

.gsc-results-wrapper-overlay{

top: 11% !important;

width: 87% !important;

left: 9% !important;

height: 43% !important;

}

.gsc-search-button-v2{

padding: 10px 10px !important;

}

.gsc-input-box{

height: 28px !important;

}

/* .gsib_a {

padding: 0px 9px 4px 9px !important;

}*/

}

@media only screen and (min-width: 1200px) and (max-width: 1920px) {

table.gsc-search-box{

width: 15% !important;

float: right !important;

margin-top: -118px !important;

}

.gsc-search-button-v2 {

padding: 6px !important;

}

}

</style>

<script>

$(function () {

$("#accordion").accordion({

event: "click hoverintent"

});

});

/*

* hoverIntent | Copyright 2011 Brian Cherne

* http://cherne.net/brian/resources/jquery.hoverIntent.html

* modified by the jQuery UI team

*/

$.event.special.hoverintent = {

setup: function () {

$(this).bind("mouseover", jQuery.event.special.hoverintent.handler);

},

teardown: function () {

$(this).unbind("mouseover", jQuery.event.special.hoverintent.handler);

},

handler: function (event) {

var currentX, currentY, timeout,

args = arguments,

target = $(event.target),

previousX = event.pageX,

previousY = event.pageY;

function track(event) {

currentX = event.pageX;

currentY = event.pageY;

}

;

function clear() {

target

.unbind("mousemove", track)

.unbind("mouseout", clear);

clearTimeout(timeout);

}

function handler() {

var prop,

orig = event;

if ((Math.abs(previousX - currentX) +

Math.abs(previousY - currentY)) < 7) {

clear();

event = $.Event("hoverintent");

for (prop in orig) {

if (!(prop in event)) {

event[prop] = orig[prop];

}

}

// Prevent accessing the original event since the new event

// is fired asynchronously and the old event is no longer

// usable (#6028)

delete event.originalEvent;

target.trigger(event);

} else {

previousX = currentX;

previousY = currentY;

timeout = setTimeout(handler, 100);

}

}

timeout = setTimeout(handler, 100);

target.bind({

mousemove: track,

mouseout: clear

});

}

};

</script>

<script type="text/javascript">

var _gaq = _gaq || [];

_gaq.push(['_setAccount', 'UA-472075-3']);

_gaq.push(['_trackPageview']);

(function () {

var ga = document.createElement('script');

ga.type = 'text/javascript';

ga.async = true;

ga.src = ('https:' == document.location.protocol ? 'https://ssl' : 'http://www') + '.google-analytics.com/ga.js';

var s = document.getElementsByTagName('script')[0];

s.parentNode.insertBefore(ga, s);

})();

</script>

<link rel="stylesheet" href="/css/custom.css?v=1.16"/> <script src="/js/jquery.ui.totop.js?1575549704"></script> <script src="/js/setting.js?1575549704"></script> <link rel="manifest" href="/manifest.json">

<meta name="theme-color" content="#616163" />

<meta name="apple-mobile-web-app-capable" content="yes">

<meta name="apple-mobile-web-app-status-bar-style" content="black">

<meta name="apple-mobile-web-app-title" content="im4change">

<link rel="apple-touch-icon" href="/icons/logo-192x192.png">

</head>

<body id="top" class="home inner blog">

<div class="background-cover"></div>

<div class="wrapper animated">

<header id="theme-header" class="header_inner" style="position: relative;">

<div class="logo inner_logo" style="left:20px !important">

<a title="Home" href="https://im4change.in/">

<img src="https://im4change.in/images/logo2.jpg?1582080632" class="logo_image" alt="im4change"/> </a>

</div>

<div class="langhindi" style="color: #000;display:none;"

href="https://im4change.in/">

<a class="more-link" href="https://im4change.in/">Home</a>

<a href="https://im4change.in/hindi/" class="langbutton ">हिन्दी</a>

</div>

<nav class="fade-in animated2" id="main-nav">

<div class="container">

<div class="main-menu">

<ul class="menu" id="menu-main">

<li class="menu-item menu-item-type-custom menu-item-object-custom menu-item-has-children"

style="left: -40px;"><a

target="_blank" href="https://im4change.in/">Home</a>

</li>

<li class="menu-item mega-menu menu-item-type-taxonomy mega-menu menu-item-object-category mega-menu menu-item-has-children parent-list"

style=" margin-left: -40px;"><a href="#">KNOWLEDGE GATEWAY <span class="sub-indicator"></span>

</a>

<div class="mega-menu-block background_menu" style="padding-top:25px;">

<div class="container">

<div class="mega-menu-content">

<div class="mega-menu-item">

<h3><b>Farm Crisis</b></h3>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/farmers039-suicides-14.html"

class="left postionrel">Farm Suicides </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/unemployment-30.html"

class="left postionrel">Unemployment </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/rural-distress-70.html"

class="left postionrel">Rural distress </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/migration-34.html"

class="left postionrel">Migration </a>

</p>

<p style="padding-left:5px;">

<a target="_blank" href="https://im4change.in/farm-crisis/key-facts-72.html"

class="left postionrel">Key Facts </a>

</p>

<p style="padding-left:5px;">